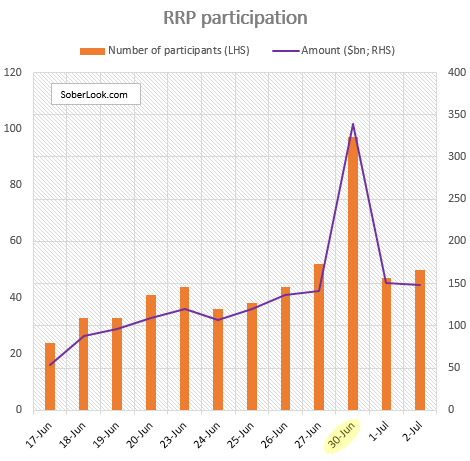

If you are a bank or even a money market fund, you probably want your financials to show the maximum amount of your overnight liquidity placed with the Fed’s RRP rather than with other banks. Your balance sheet looks less “risky” this way. And since most financial reporting is done at quarter end (with mid-year and year-end being the most important dates), you want to place your cash with the Fed on the last day of the quarter for one night and then take it out. And that’s exactly what’s taking place currently.

Â

Why not leave your liquidity with the Fed for a longer period? Because the Fed’s current RRP rate pays 5 basis points, while the private repo market is paying about double that. Of course as cash is pulled out of the repo markets for quarter-end and moved to the Fed or elsewhere, rates in the private markets rise. Once the liquidity comes back to the private markets at the start of the new quarter, the repo rates return to normal.

|

| Source: DTCC |

The larger the RRP program becomes, the stronger this quarter-end effect will be. Welcome to the wonderful world of window dressing.