I have been suggesting for several years that the U.S. Dollar would confound those anticipating its demise by starting a long secular uptrend.

In early September I made the case for a rising U.S. dollar, based on the basic supply and demand for dollars stemming from four dynamics:

- Demand for dollars as reserves

- Other nations devaluing their own currencies to increase exports

- “Flight to safety†from periphery currencies to the reserve currencies

- Reduced issuance of dollars due to declining U.S. fiscal deficits and the end of QE (quantitative easing)

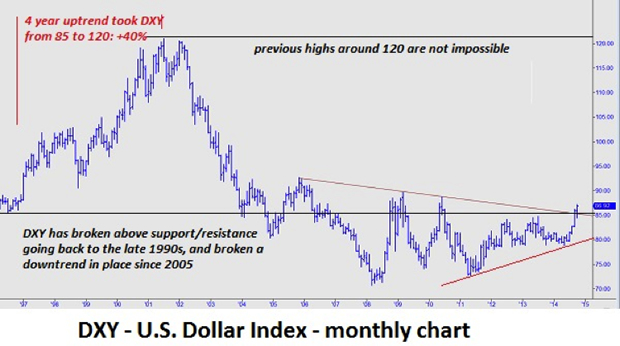

Since then the dollar has continued its advance, and is now breaking out of a downtrend stretching back to 2005—and by some accounts, to 1985:

Â

(Source)

Â

Technically, the Dollar Index has broken out of a multi-year wedge:

Â

Â

So what does this mean for the global economy?

Â

Â

Since currencies are intertwined with virtually every aspect of the global economy—trade, credit, inflation/deflation, commodities and capital flows, even political and soft power—there is no one consequence, but a multitude of interactive consequences.

Â

For U.S. households, the rising dollar will have gradual, generally marginal effects: our dollars will buy more euros and yen when we visit Europe and Japan as tourists, imports from countries with weakening currencies will be slightly cheaper (if the importers don’t palm the difference as extra profit) and we may be competing with more foreigners for dollar-based assets such as American homes, oil wells and Treasury bonds.

Â

In sum, a rising dollar will only affect households on the margins. Since roughly 85% of the U.S. economy is domestic, imports and exports have relatively limited influence on the entire economy.

Â

In other words, the direct consequences of a stronger dollar on U.S. households are generally positive, with the exception of those working in price-sensitive export industries, where the rising dollar will make goods sold in countries with weakening currencies more costly.

Â

But the secondary effects could end up being far more consequential for Americans and everyone else on the planet, for this reason: the centrality of the dollar in the global economy means that the effects of a stronger dollar can create potentially destabilizing dynamics.Â

Â

Simply put, the dollar’s rise could destabilize the entire global financial system. To understand why this is so, we have to start with the source of the risk: the world’s central banks.

Â

Central Banks Are Responsible for the Heightened Risk

Â

One primary reason for this expansion of risk is the unprecedented actions of the world’s central banks since the 2008 Global Financial Meltdown. In effect, the central banks doubled down on debt and leverage as the politically expedient “solution†to the implosion of credit and leverage (what we call de-leveraging) as the collateral underlying highly leveraged loans (think subprime mortgages on overpriced McMansions) evaporated like mist in Death Valley.

Â