Image Source:

Image Source:

It’s the first UK budget for the new Labour government and Britain’s first female Chancellor, Rachel Reeves. Big tax rises look inevitable, given the growing demands on the public purse. More investment is coming, too, but will that come with even more borrowing? That’s the key question for markets, and Reeves will seek to tread carefully.

The new Chancellor has inherited some challengesTo say that Chancellor Rachel Reeves is unhappy with her public finance inheritance would be an understatement. She has characterized the economic backdrop as the worst since World War II.That’s hard to square against the decent growth numbers we’ve had so far this year. The UK has been among the fastest growing in Europe, following a small technical recession in late 2023.But some of Reeves’ frustration is understandable. Treasury rules dictate that debt must be projected to fall as a share of GDP within five years. As of the March budget, that rule was met by the finest of margins, and only by making some challenging and often unrealistic assumptions about future public spending.Departmental budgets, set in 2021, have not been properly adjusted for higher inflation or the rising population. Real-terms per capita departmental spending is down 7% from three years ago. And without further action, further real-term cuts are coming in many areas. It’s hard to see how those can be implemented, with public service standards already under severe pressure.Public investment projections have suffered, too. That’s set to fall from 2.5% of GDP last year to 1.7% by the end of the Office for Budget responsibility’s forecast.Labor may find it has little choice but to raise both day-to-day and capital spending. But raising the required revenue has been made considerably harder by Labour’s election pledges, which ruled out tax rises for working people. In doing so, it has effectively ruled out changes to taxes that account for up to 70% of the public revenue it can actively control.Labor’s tax raising options* VAT on private schools unlikely to materially move the needle for overall VAT revenue Source: OBR, ING

Source: OBR, ING

Does the UK’s strong economic performance reduce the need for tax hikes?When pressed during the election campaign, Labour’s answer to finding more money was to grow the economy. And the key to unlocking that money in the shorter term is to convince the OBR to upgrade its growth forecasts.The Treasury will be hoping that the UK’s surprisingly strong growth this year will convince it to do just that. Even small changes to those GDP forecasts can make big changes to the amount of “headroom” it has available against its fiscal rules.Unfortunately, we think that’s wishful thinking. The OBR, like most economists, is likely to conclude that this year’s growth spurt is unlikely to last. If anything, the OBR’s forecasts already sit towards the more optimistic end of the spectrum on growth.There are no obvious tailwinds from financial markets, either. Higher inflation and, latterly, lower debt interest projections granted the previous Conservative government the headroom to make significant personal tax cuts. There’s no such luck this time; if anything, market rates are slightly higher than when the OBR last ran the numbers in March.In short, the amount of headroom available under the current fiscal rules is unlikely to have drastically changed since March.

What fiscal rules are the Treasury likely to choose?If the rules dictate that money is tight, why not just move the goalposts?That’s exactly what the government is expected to do in the budget. A new rule will require the Treasury to balance the current budget (day-to-day spending vs revenues) within five years.Interestingly, that doesn’t actually buy the Treasury much additional breathing room. Fiscal “headroom” would increase from £9bn to £14bn, if this rule were to become the binding constraint on the public finances.But here’s the crucial part: the current budget purposefully excludes government investment. And changes to the government’s other main fiscal rule could unlock tens of billions of pounds a year to spend on new projects.Recall the existing rule, which says that debt needs to fall as a share of GDP within five years. That rule is based on a debt measure that’s being artificially inflated as the BoE sells off its bond holdings. Switching back to the standard measure of public net debt would increase the headroom available by £16bn, according to the OBR’s March numbers.The government may go further still. There’s been a lot of discussion about basing the fiscal rules on public sector net worth. There are a few versions of this, but the idea is that it would capture the impact of investment not only on debt but also on the asset value it creates.The major appeal is that this would, on paper, unlock more than £50bn/year in additional funds for capital spending.

Will we see a dramatic increase in public investment?That all sounds great, but the fiscal rules are ultimately a self-imposed constraint. The simple reality is that any extra spending needs to be funded either by tax or borrowing. And this is ultimately what financial markets care about.The Treasury is going to be naturally cautious. The 2022 mini-budget debacle, which saw a mass sell-off in UK government debt markets, is still fresh in Westminster’s institutional memory. We suspect Reeves won’t ramp up investment anywhere near as far as some people have been led to think.The fact is that the metrics of public sector net worth are far from perfect. Valuing government assets isn’t at all straightforward. We think the Treasury will stick to a debt-based fiscal rule, and perhaps open a consultation into using the net worth measures in future.But even if the government does change the fiscal rules dramatically, it’s hard to see it spending all, or even most, of the extra cash afforded to it.History shows that chancellors tend to want to keep a safety buffer, not just to signal prudence, but also to protect themselves against adverse changes in economic conditions at future budgets. Previous chancellors have generally kept much more left over than the £9bn headroom in March. Then there are the practicalities. Deploying government investment often isn’t easy. The UK’s notorious planning delays, combined with the Civil Service capacity to deploy investment, means that lifting net investment much above 2.5% of GDP may not be easily achievable.That would still imply an extra £30bn/year on investment after five years, which would mark a significant increase in borrowing. Concerns about the market impact suggest that what gets announced is likely to be a fair bit lower.Public sector net investment set to fall as a share of GDP Source: ONS, OBR

Source: ONS, OBR

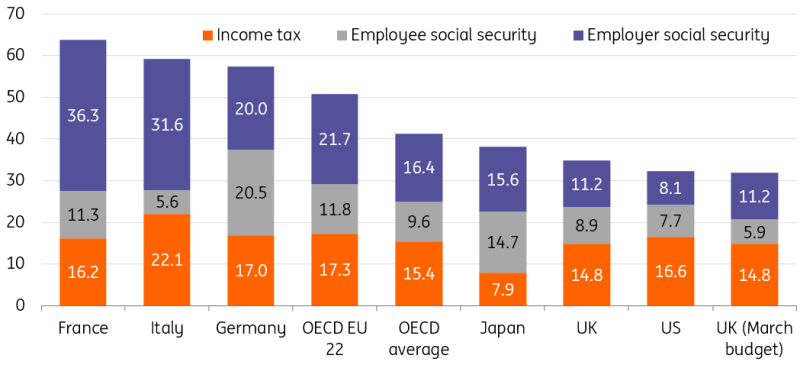

How significantly will taxes rise to meet day-to-day spending needs?Day-to-day spending is set to rise. The only question is by how much.Ending those planned real-terms cuts to departmental budgets mentioned earlier carries a price tag of roughly £20bn/year. The recently announced public-sector pay deal, at a cost of roughly £10bn, goes some way towards that.But simply allowing spending to rise with inflation may not be sufficient, something Reeves seems to agree with. From ageing to worker shortages, the public sector faces a growing list of long-term challenges.Whatever happens, it means that the government is going to raise more money than it said it would back at the general election. Possible changes to capital gains or inheritance tax, though controversial, would not be major revenue raisers. That’s why recent reports have instead centred on employer’s national insurance or social security. Increasing the rate paid by employers, and/or expanding NI to pension contributions, has the potential to raise more than £20bn/year.Putting the debate on whether that’s a good idea or not to one side, it’s worth remembering that social security contributions by UK employers are considerably lower than the EU average. Employer NI accounts for 11% of the average UK worker salary, versus comparable taxes worth 22% across the OECD’s EU average.It’s a reminder that while the UK’s tax burden (tax as a share of GDP) is the highest since the Second World War, it’s low by European standards. Income and social security as a percentage of an average single-person’s income (2023 data)Note: National Insurance was cut by four percentage points for employees across the November 2023 and March 2024 budgets Source: OECD, ING calculations

Source: OECD, ING calculations

Are markets getting nervous?The short answer is no. While markets will be eagerly awaiting news on any extra borrowing, there’s little sign of nervousness so far. Our FX team’s models show that there’s currently no risk premium in the pound, compared to 3% at the time of the mini-budget turmoil in 2022.Similarly, while 10-year gilt yields have risen over recent weeks, that’s down to shifting monetary policy expectations. The spread between gilts and swaps, which gives a sense of the additional risk investors see in holding UK bonds over a risk-free swap rate, has also been relatively stable. That’s been more heavily influenced by the Bank of England’s quantitative tightening.We doubt this picture will change much after the budget, either. Reeves’ rule requiring a balanced current budget limits the government’s ability to ramp up day-to-day spending without lifting taxes. That was what sparked the sell-off back in 2022. Within reason, investors are likely to be more tolerant of borrowing where it is targeted at growth-enhancing capital spending.There’s currently no risk premium in the pound Source: ING, Refinitiv

Source: ING, Refinitiv

How does this all affect the Bank of England?The bottom line is that the budget is likely to see higher day-to-day spending, largely matched by tax rises, with some debt-funded investment. While that’s potentially a net stimulus for the economy in the longer term, the impact over the next couple of years is less clear cut. And that means it shouldn’t massively change the course of BoE interest rate cuts.We expect a cut in November to be followed by another in December, with Bank Rate settling at 3.25% by the end of next summer.More By This Author:FX Daily: Dollar Rally Can Pause, But Should Not Correct Rates Spark: US Election Risk May Limit EUR Rates Upside The Commodities Feed: Chinese Oil Import Quota Increased

What The Markets Are Expecting From The UK’s Crucial Budget