Data/Event Risks

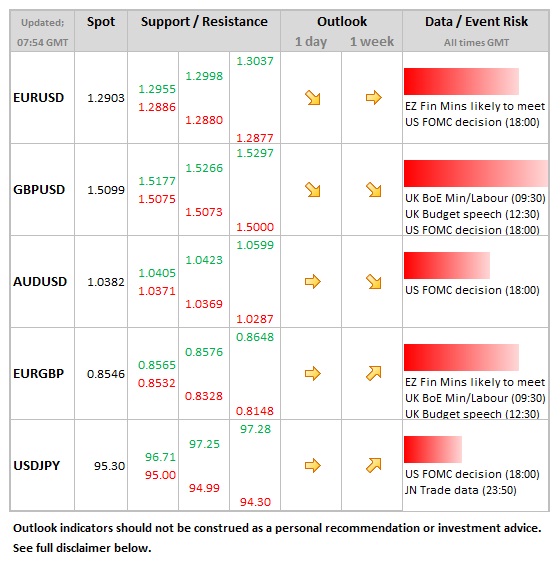

- EUR:  Eurozone finance ministers are likely to meet today to discuss the options for Cyprus after yesterday’s rejection of the deposit tax levy. The ECB meeting also meets and headlines from here will be key to watch with respect of emergency liquidity assistance (ELA) to Cypriot banks. Opinion: EUR/USD: Any upwards move could be an opportunity to go short

- GBP: Key data, with Bank of England minutes early on (Feb saw 3 votes for more QE), together with labour market figures.  The budget statement normally re-affirms the Bank of England’s inflation target, but there are risks that the Bank’s remit is either adjusted more radically, or the intention to do so is announced. This would almost certainly be sterling negative. Pound has performed well vs. euro this week, but this will be tested today.

- USD: The FOMC rate decision due at 18:00 GMT, but brings low risk. Greatest risk comes from change in wording of statement. Even though data has been better of late, the budgetary stand-off prevents the US central bank from becoming more confident in signalling a possible end to the current QE regime.

Idea of the Day

After yesterday’s resounding rejection of the bank levy by the Cypriot parliament, the focus today is the search for a plan B. Although the situation is very fluid, the suggestion is that Eurozone finance ministers will meet to discuss the options. At the same time, the Cypriot finance minister is in talks with Russia. The single currency is off the lows seen just after the announcement of the vote late yesterday, starting the European session back above the 1.29 level.

The way other currencies have been behaving has been instructive. The yen has outperformed, but perhaps not as much as would normally be expected in the risk-on/risk-off days of old. Sterling has held up as well and the other interesting dynamic has been the dollar-bloc currencies (AUD, CAD, NZD) which have all held up relatively well and avoided the risk-off dynamic that would have pressured them last year. But this should not surprise, as we’ve highlighted before (see Proving the new FX Regime). The key for market today probably lies with the ECB. Late yesterday, the ECB pledged to maintain emergency liquidity assistance to Cypriot banks “within existing rulesâ€.

Latest FX News

- EUR: Naturally Cyprus remains in the frame. The focus from here is on any emerging Plan B and the stance of the ECB. Key level is 1.2877, which is 50% Fibonacci level and also 200d moving average.

- GBP:  Rallying into European close and there’s no denying that the troubles in Europe are allowing sterling to benefit, but there are many hurdles for today. Upside resistance is seen at 1.5177 vs. USD, whilst the 1.50 level is natural support to the downside.

- JPY:  Firmer over the past 24 hours, but only modestly so and it’s difficult to say it’s behaving as the safe haven it once was. Today first day of new BoJ Governor Kuroda and expectations are strong for policy action in the coming weeks.

- AUD: The performance of the Aussie (together with CAD and NZD) were further proof that we have moved on from risk-on/risk-off dynamic, performing comparatively well in what would normally be described a “risk-off†environment. Better tone would be secured by close above 1.0413 (61.8% retracement of year’s range).

Further reading:Â Forex Analysis: EUR/USD Bearish Trend Drops to 50% of Prior Bullish Trend