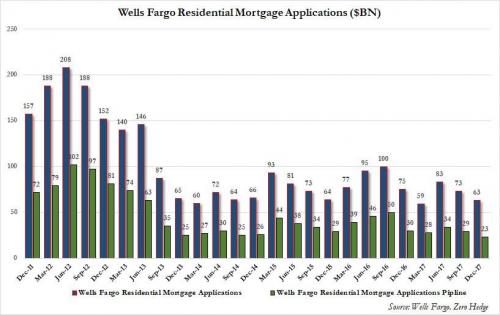

When we reported Wells Fargo’s Q3 earnings back in October, we drew readers’ attention to one specific line of business, the one we dubbed the bank’s “bread and butter“, namely mortgage lending, and which as we then reported was “the biggest alarm” because “as a result of rising rates, Wells’ residential mortgage applications and pipelines both tumbled, specifically in Q3 Wells’ mortgage applications plunged by $10 billion from the prior quarter to $73 billion, while the mortgage origination pipeline plunged to just $29 billion,” and just shy of the post-crisis lows recorded in late 2013.

Fast forward one quarter when what was already a grim situation for Warren Buffett’s favorite bank, just got as bad as it has been since the financial crisis for America’s largest mortgage lender, because buried deep in its presentation accompanying otherwise unremarkable Q1 results (EPS small beat, revenue small miss), Wells just reported that its ‘bread and butter’ is virtually gone, and in Q1 the amount in the all-important Wells Fargo Mortgage Application pipeline plunged by a whopping 23% to just $23 billion, and at the lowest level since the financial crisis.

And while Wells’ mortgage applications, a less forward looking indicator, was not quite as dire, it too was just shy of fresh post crisis lows at only $63 billion, just barely above the post-crisis low hit one year ago.Â

The lagging mortgage originations number, which usually trails the pipeline by 3-4 quarters, was nearly as bad, plunging 39% sequentially from $72 billion to only $44 billion, “due to higher rates and seasonality.” Since this number lags the mortgage applications, we expect it to post fresh post-crisis lows in the coming quarter.

Adding insult to injury, as one would expect with the yield curve flattening to 10 year lows recently, Wells’ Net Interest Margin – the source of its interest income – declined to a one year low, missing expectations once again. This is what Wells said: “NIM of 2.84%, down 2 bps LQ as the negative adjustment related to leveraged leases, and growth in average deposits, were partially offset by lower average long-term debt and a modest net benefit from all other growth, repricing and variable item.” And visually: