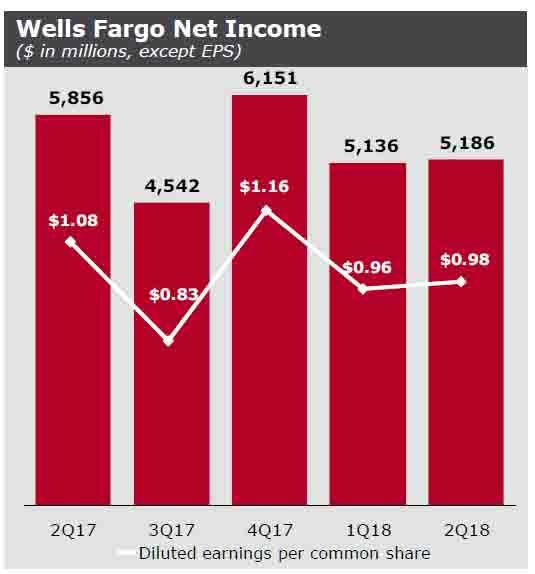

Unlike JPM, which started off Q2 solidly, if with some weakness in loan creation, rapidly rising deposit costs, and a missing outlook page, Wells Fargo had an ugly second quarter, in which it missed on the top and bottom line, reporting revenue of $21.6BN down 3% Y/Y and down 2% Q/Q, missing expectations of $21.71BN, and EPS of $0.98, also below the $1.12 expected.

To be sure, there was some good news in the report: first Well said that its Net Interest Margin rose 9bps from 2.84% to 2.93%, the highest in over a year, and translating in Net Interest Income of $12.54BN, up from $12.471BN a year ago, even though the entire gain vs last year was solely due to one extra day in the quarter generating $80 million in revenue.

Additionally, the net charge-offs of $602 million, were down $139 million LQ: the $150 million reserve release reflected strong credit portfolio performance, as well as lower loan balances. Meanwhile, non-performing assets decreased $305 million Q/Q to $7.99BN as nonaccrual loans decreased $233 million as a $282 million decline in consumer real estate non-accruals was partially offset by a $46 million increase in commercial nonaccruals. Also good news: Foreclosed assets declined $72 million.

Alas, everything else in the report was ugly, starting with non-interest income which tumbled from $9.8BN to $9.0BN, largely as a result of trading gains which were down $52 million and included lower customer trading activity in equity products.

But far more concerning was the ongoing shrinkage in the company’s balance sheet, as period-end loans declined from $947.3BN to $944.3BN, the lowest in years, and down $13.1 billion YoY driven by “declines in auto and legacy consumer real estate portfolios including Pick-a-Pay and junior lien mortgages, as well as lower commercial real estate loans.”

There was a decline in period-end loan balances across the board with:

- Commercial loans down $291MM

- Commercial real estate loans down $2.5BN

- Commercial and industrial up $1.9BN

- Lease financing up $321MM