There is nothing fancy about these three solutions.

I have covered rising income/wealth inequality for many years in dozens of entries. Since Thomas Piketty’s new book has catapulted the topic into the media spotlight, it’s a good time to list solutions that go deeper than Piketty’s proposed global wealth tax–a proposal he characterizes as utopian.

Every solution is utopian, because the Financial Aristocracy and their central bank cronies have democracy by the throat. There is no legislative way to change the Status Quo when political power is for sale to the highest bidder, and central banks are issuing nearly-free money to the financial oligarchy that owns the political machinery.

But listing solutions is still important, because it reveals just how far from democracy, rule of law and free-market capitalism we have fallen. I have been describing various aspects of widening inequality in recent entries:

America’s Nine Classes: The New Class Hierarchy

A Critique of Piketty’s Solution to Widening Wealth Inequality

Are You an Elitist? Class Warfare and the New Nobility

I propose three straightforward solutions that will systemically rectify wealth and income inequality.

1. Rather than add taxes to fund more social welfare–in effect, placing a Band-Aid over the tumor–let’s start by removing the source of rising inequality: the Federal Reserve. I laid out in detail how the Fed’s policies have enriched the top .1% at the expense of everyone else in Want to Reduce Income/Wealth Inequality? Abolish the Engine of Inequality, the Federal Reserve (January 28, 2014)

This boils down to the Cantillion Effect: new money is injected into the economy at specific points, creating winners and losers. Those with access to the new money (in the Federal Reserve’s policies, those with financial power) gain immensely and everyone far from the free-money spigot loses purchasing power.

There’s no mystery here: if trillions of dollars are available at near-zero interest rates to those at the top of the pyramid, they will benefit accordingly.

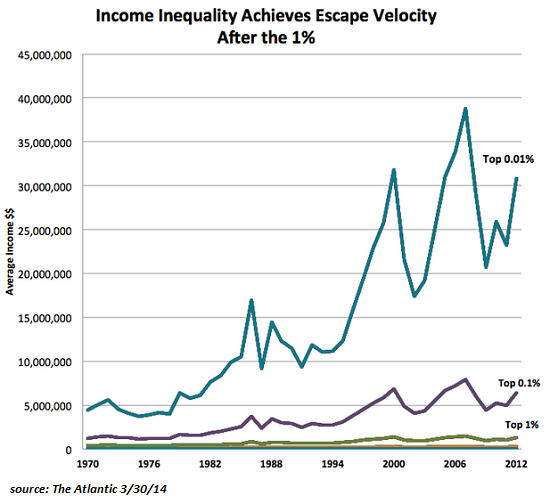

This chart shows how access to the Fed’s free-money spigot causes the very top layer of owners of capital to outpace their less-wealthy peers: while the top 10% has outpaced the bottom 90% and the top 1% has outpaced the top 10%, the real action is at the very pinnacle of wealth holders: the top .1% has outpaced the 1%, and the top .01% has outpaced the .1%.

Were the Fed abolished, the top holders of financial wealth would no longer have access to unlimited sums of free money, and the asset bubbles that are the essential engines of wealth inequality would all collapse, along with the vast majority of the top holders’ phantom wealth.

The collapse of asset valuations would impact middle-class holders of IRAs, 401Ks and pension funds invested in asset bubbles, but the real losers would be those at the top who own most of the phantom financial wealth.

2. Eliminate the 6.2% Social Security payroll tax paid by employees and employers, and print the money to pay Social Security benefits in the Treasury. I described this solution in How About Ending Social Security and Paying Retirees with Cash? (November 15, 2013).

The basic idea is this:Â rather than borrow money into existence via the Federal Reserve, abolish the Fed and print the new money directly. There is no interest to be paid on this new money, and so the financial parasites have nothing to gain from its creation.

This would wipe out the most regressive tax on the working poor, and benefit all employers. Each currently pay 6.2% of wages, so eliminating Social Security taxes would give every worker an immediate 6.2% raise and every employer a 6.2% reduction in labor overhead. (The 1.45% Medicare tax each pays would remain in place.)

The newly issued $800 billion a year would flow directly into tens of millions of individuals’ accounts, where the the majority of it will be spent in the real economy.

As for those who claim creating $800 billion a year would spark runaway inflation: the Fed has printed over $3 trillion in the past five years, and inflation is mostly a result of asset bubbles and cartel pricing (sickcare, college tuition, F-35 aircraft, etc.), not new money.

Abolishing the Fed would trigger a deflationary collapse of asset bubbles. Printing $800 billion and distributing it to tens of millions of households would only counter some of this deflationary wave. The $800 billion annual distribution is simply too small to create inflation in a $16 trillion economy that is undergoing a cleansing of trillions of dollars in phantom wealth at the top of the wealth pyramid.

3. Tax unearned income at much higher rates than earned income. The vast majority of the New Nobility’s income is unearned income from rents, interest, dividends and capital gains. Taxing unearned income is in effect a wealth tax because only those who own income-producing assets have unearned income.

It would be easy to set up a simple tiered tax structure that reduces income taxes for households with less than $250,000 annual earned income and offsets that reduction by raising the tax on unearned income above some level that enables small entrepreneurs and middle-class households to accumulate capital–for example, unearned income such as interest, dividends and capital gains would be taxed at the same rate as earned income up to $100,000 and then rises to much higher rates above that level.

There is nothing fancy about these three solutions. They shift the incentives away from speculation to earned income/productive work, they lower regressive taxes on the middle class and working poor and they do not restrain legitimate enterprise and wealth accumulation. They eliminate complex systems (the Federal Reserve and the tax code) and put money in the hands of tens of millions of households rather then the top .1%.

Yes, they are utopian, but only because we keep electing the same bought-and-paid-for Demopublican lapdogs of the super-wealthy and vested interests.

Â