Overnight bulletin summary

- Global equities trade higher amid easing geopolitical tensions

- Pound tumbles on weaker than expected inflation data

- Today’s calendar includes US retail sales, Empire Fed, import prices, NAHB, and API crude oil inventories

Global stocks and US futures are up for a second day, with the VIX sliding 0.65 vols to 11.68 (-5.2%) and haven assets dropping, after a KCNA report report suggested North Korea had pulled back its threat to attack Guam after days of increasingly bellicose “fire and fury” rhetoric with President Trump, and hours after China took its toughest steps to support U.N. sanctions against Pyongyang, while the possibility of a Sino-American trade war was played down. The report, from KCNA on Tuesday, said Kim praised the military for drawing up a “careful plan†to fire missiles toward Guam. Kim was cited by KCNA saying he would watch the U.S.’s conduct “a little more.â€

“There is a more relaxed attitude being taken towards the Korean situation in markets. With the report North Korea has put its plans on hold, there is a sense of stepping back from the brink,” Rabobank analyst Lyn Graham-Taylor said.

Notably, risk aversion has not totally gone away, as Defence secretary Mattis also warned earlier that if NK fired missiles at Guam, it would be “game on†and “could escalate into war quicklyâ€. That said, he was vague about what would happen if missiles splashed into the sea near Guam.

The result was a continuation of yesterday’s “risk-on” sentiment: the USD bounced, the USDJPY spiked as hugh as 110.45, while the pound tumbled on poor UK inflation data, while the EUR was dragged lower on what is a holiday across continental Europe. However, as some trading desks warn, this return of risk appetite may be temporary as the US and South Korea have joint military exercises scheduled for next week, which could spark things off again. For now however, traditional haven assets including gold and core bonds across Europe and TSYs slumped.

Global stocks were roughly unchanged, with the MSCI All-Country World Index declined less than 0.05 percent, while Europe was broadly if modestly higher with the Stoxx Europe 600 Index up 0.1%. Germany’s DAX Index jumped 0.3 percent, as did the U.K.’s FTSE 100 Index. S&P Futures are up 0.2%.

In Asia, Japan’s Topix index finished the day 1.1% higher driven by the sharp drop in the Yen, and Australia’s S&P/ASX 200 Index gained 0.5% at the close. Hong Kong’s Hang Seng index dropped 0.3% following a bout of last hour selling, even as the Shanghai Composite Index rose 0.4%. Markets in South Korea and India are closed Tuesday for holidays. The yen fell 0.7% to 110.41 per dollar, the biggest drop in three weeks.

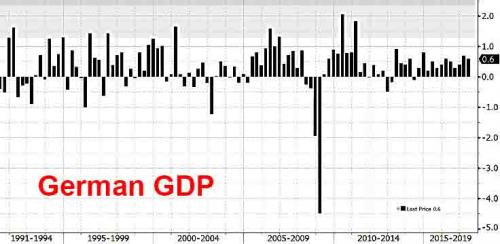

While the overnight session was generally quiet, aside from the previously noted UK inflation miss which sent sterling tumbling, another indication that Europe may be rolling over was German Q2 GDP data, which missed at 0.6%, below the 0.7% expected, as imports outpaced exports following the recent surge in the Euro.

After hawkish comments from Dudley and UST yields doing well, there is a broad USD bid, even though South Korean markets was closed for national holiday. As noted above, the yen dropped on easing of N.Korean tensions, while the pound weakened after U.K. inflation data missed estimates, and Sweden’s krona gained as headline inflation reached the highest level since 2011.

“We have North Korea saying they will wait, and Trump not saying anything at all, compared to his past promise of ‘fire and fury,'” said Mitsuo Imaizumi, chief FX strategist at Daiwa Securities.”That added up to good news for the dollar, bad news for the yen,” he said.

Also overnight, China’s credit growth came in higher than expected even as broad M2 plunged to a new all time low of 9.2% (exp. 9.4%): new yuan loans printed 825bn vs 800bn expected while aggregate financing came in at 1220bn vs 1000bn. However both measures of credit growth decreased sharply from June, where aggregate financing was 1776bn and new yuan loans increasing 1540bn.

In rates, the yield on 10-year Treasuries advanced three basis points to 2.25 percent.Germany’s 10-year yield gained two basis points to 0.43 percent.Britain’s 10-year yield climbed three basis points to 1.01 percent.

Gold fell 0.6 percent to $1,274 an ounce. Oil prices steadied somewhat after falling more than 2.5 percent on Monday to its lowest in about three weeks on the strength of the dollar and reduced refining in China. Brent was last down 2 cents at $50.71 a barrel.

Market Snapshot

- S&P 500 futures up 0.2% to 2,467.25

- U.S. 10Y Treasury yield: +3bps to 2.25%

- EUR/USD: -0.2% to 1.1758

- USD/JPY: +0.7% at 110.40

- GBP/USD: -0.5% at 1.2901

- STOXX Europe 600 up 0.07% to 376.41

- MSCI Asia up 0.2% to 158.72

- MSCI Asia ex Japan up 0.07% to 520.98

- Nikkei up 1.1% to 19,753.31

- Topix up 1.1% to 1,616.21

- Hang Seng Index down 0.3% to 27,174.96

- Shanghai Composite up 0.4% to 3,251.26

- Sensex up 0.8% to 31,449.03

- Australia S&P/ASX 200 up 0.5% to 5,757.48

- Kospi up 0.6% to 2,334.22

- German 10Y yield rose 1.5 bps to 0.421%

- Euro down 0.2% to $1.1752

- Italian 10Y yield fell 0.9 bps to 1.73%

- Spanish 10Y yield rose 0.2 bps to 1.44%

- Brent futures down 0.1% to $50.68/bbl

- Gold spot down 0.6% to $1,274.68

- U.S. Dollar Index up 0.3% to 93.68