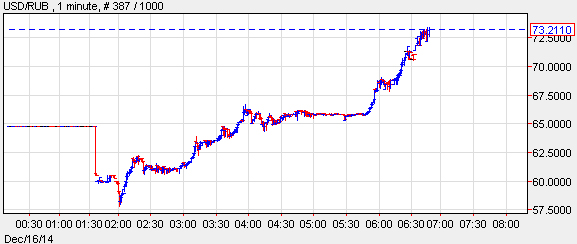

For those wondering if the CBR’s intervention in the Russian FX market with its shocking emergency rate hike to 17% overnight calmed things, the answer is yes… for about two minutes. The USDRUB indeed tumbled nearly 10% to 59 and then promptly blew right back out, the Ruble crashing in panic selling and seemingly without any CBR market interventions, and at last check was freefalling through 72 74 76, and sending the Russian stock market plummeting by over 15%.

It is so bad, US equity futures which had jumped earlier on hopes of more Chinese intervention following the latest disastrous Chinese PMI print, as well as a French manufacturing PMI beat (don’t laugh), are back to unchanged.

The latest rout continues to be driven by the relentless plunge in Brent which also continued crashing overnight to fresh 5 year lows, sliding decidedly under $60 as WTI dropped well under $55 as well. And as we previewed over a month ago, it is not just Russia, but every single petroleum exporting country that is suddenly seeing a currency crisis, and spreading to all EMs with the Indian Rupee weakening the most since 2013, Indonesia lowering the Rupiah’s reference rate by the most on record, and so on. Ironically, this happens as the USDJPY is also crashing and dropping moments ago to 116.25, the lowest level since mid-November. At this rate the Fed will have no choice but to intervene, however in the opposite direction, and admit that despite all its best intentions, the US can not decouple from the rest of the world and a rate hike – so very priced in by everyone – is just no going to happen in the coming years (which sadly means that the latest subprime debt driven “recovery” is about to be called off).

A quick look at the oil market where Brent drops for 5th day, falls below $60 for 1st time since July 7, 2009 as the market continues to look for signs that falling prices is crimping production. WTI breaks below $55, drops to lowest since May 6, 2009. “The race to the bottom continues, we are still not seeing any signs of supply disruption,†says Saxo Bank head of commodity strategy Ole Hansen. “There is very big negative momentum in the mkt and the fact people are starting to talk about breakeven levels of $35-$40 has put up a new red flag for mkts to aim at.… Jan. WTI options expire today and there is quite a lot of open interest ~$55 put strikes, that is probably the key level of potential support today.â€

Not helping things was Russia’s announcement that it too like the Saudis will not cut production: Russia agrees with OPEC that market will determine crude price, Energy Minister Alexander Novak tells reporters at meeting of Gas Exporting Countries Forum in Doha, Qatar. Novak says that he met with OPEC energy ministers in Vienna; “The participants of that meeting concurred that the situation will be fixed by the market itself in terms of supple and demand balance. Russia is not a country that changes its supply. We will maintain our production unchanged.â€

Looking at the Markets, first in Asia, the Nikkei 225 tumbled -2% fell for a 2nd day to breach the key psychological 17,000 level for the first time since the 17th Nov. as the JPY continued to strengthen. In China bad news was good, and the Shanghai Comp surged higher som +2.3% on renewed easing calls following disappointing Chinese data. December HSBC flash Manufacturing PMI printed a contractionary reading for the first time in 7 months (49.5 vs. Exp. 49.8 (Prev. 50.0), with both output and new orders components slipping, the latter contracting for the first time since April. Hang Seng traded down 1.55% weighed on by weakness across energy stocks.

Despite opening higher, European stocks took a turn lower in early trade, with the move to the downside led by energy names after Brent crude futures broke below USD 60/bbl pre-market and WTI broke below USD 54/bbl. Furthermore, the softness in stocks lifted European fixed income products with the Bund tripping stops through 154.73, leading the German 10yr yield to once again print record lows and slip below 0.6%. Overall global sentiment remains relatively negative with Saudi Arabian (-5.5%) and Dubai (-8%) stock indexes also placed under further pressure as the fall in oil prices continue to dent domestic profits. Furthermore, concerns were also placed on Russia as despite the Russian central bank hiking their rate by 650bps, the RUB hit record lows vs the USD and the MICEX was down as much as 7%. This then triggered fears over the ramifications for the Eurozone economy, given the close trade ties to Russia, particularly for Germany.

Nonetheless, European equities then reversed earlier losses, with the move higher led by utility and consumer discretionary names, while Russian asset classes began to stabilise. Additionally, from a data perspective, Eurozone PMIs also painted a less dreary than expected picture with the headline manufacturing and services Eurozone PMIs exceeding expectations. This was then later exacerbated by a particularly strong German ZEW survey (Expectations 34.9 vs. Exp. 20.0), which also subsequently saw Bunds pull away from their best levels.