Ok, so we’ve written volumes this year about the extent to which inflows into EM assets have remained remarkably resilient in the face of myriad headwinds, including, but by no means limited to:

- the prospect that DM central banks are on the verge of a coordinated normalization push

- swings in commodity prices and rampant uncertainty about crude

- idiosyncratic risk (think Turkey, Brazil, and South Korea)

- worries about whether China’s efforts to rein in speculation will choke off growth and/or stymie the flow of credit to the real economy

Some of EM’s resiliency can be attributed to dollar weakness and to be sure, no one is convinced that DM policy makers are actually prepared to make good on “threats†to meaningfully scale back accommodation.

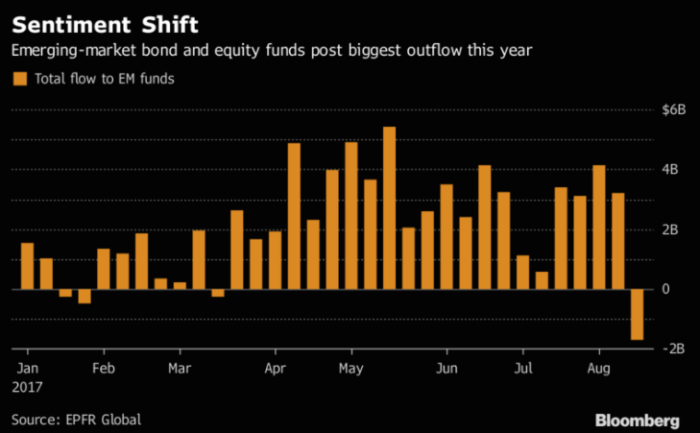

Well, with that as the context, do consider the following chart from Bloomberg which shows that for the first time in 22 weeks, EM assets as a whole experienced a net outflow:

Here’s a bit of color from Citi:

- US$1.6bn of outflow from EM funds — This is the first outflow from EM funds in 22 weeks. GEM funds saw US$251mn of redemption. Asia funds lost US$1.2bn, where US$761mn came from China funds. LatAm and EMEA funds both had close to US$70mn of outflows.

Is this the proverbial tipping point?