The BoJ is On Deck

The big item on the calendar over the next 24 hours is the Bank of Japan’s first-rate decision of the year. The BoJ was looked at and watched as one of the more passive Central Banks last year, with the Japanese Yen as one of the few currencies keeping track with the U.S. Dollar’s weakness in the last nine months of 2017 as price action in the pair remained in a range-bound state.

USD/JPYÂ Daily: Range-Bounce Since March 2017

Chart prepared by James Stanley

Are Hints of Tighter Policy on the Horizon?

Shortly after we opened the door into 2018, worries began to grow that the BoJ might embark on a ‘stealth taper.’ Given the bank’s open-ended bond-buying program, the fact that they bought fewer long-dated bonds earlier this year triggered thoughts that they may be slowly drawing down QE purchases before making any formal announcements of as such, and this equated to about three trading days of aggressive Yen strength.

EUR/JPY Four-Hour: Bearish Reversal on Fears of ‘Stealth Taper’

Chart prepared by James Stanley

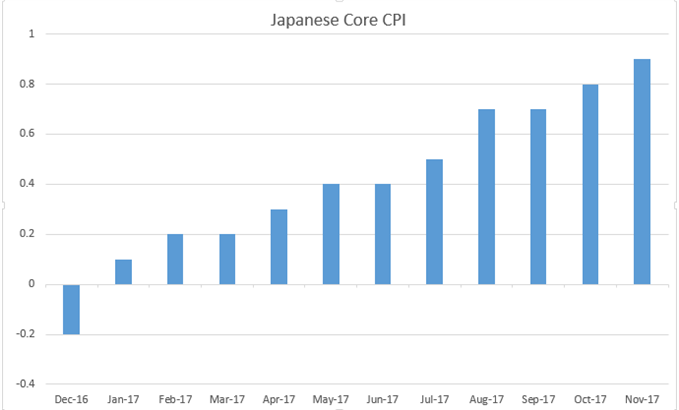

The thesis is somewhat supported by the encouraging trend that’s been seen with core inflation in Japan. After coming in at -.2% last December, core inflation went on a steady track higher throughout 2017, coming in at .9% for November. This is still far below the bank’s 2% inflation target, but the trend is encouraging nonetheless.

Japan’s Core Inflation with a Steady Stream of Growth in 2017

Chart prepared by James Stanley

The Bank of Japan has previously said that they’re confident that the economy will be able to hit their 2% inflation target inside of the next two years, but this is something the bank has been saying for a while (much longer than just the past two years) without it actually coming to fruition. Also of concern is the fact that the BoJ may still be gun shy after their move to negative rates two years ago seemed to really blow up; bringing on months of Yen strength, diametrically opposed to their initial goal of more weakness.