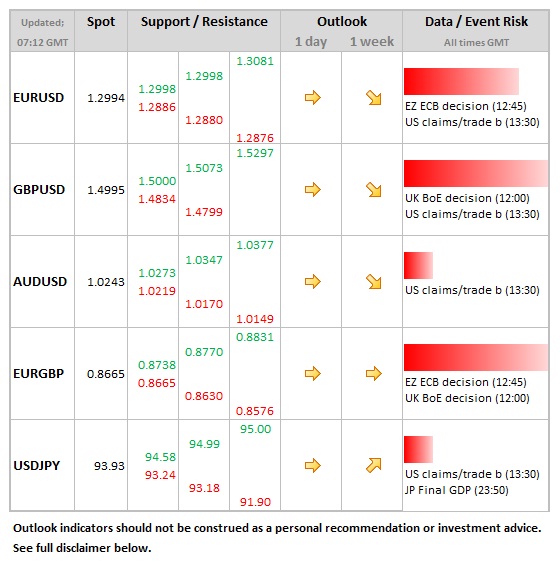

Data/Event Risks

Data/Event Risks

- EUR: The ECB meeting brings lower risk of a surprise vs. that of the Bank of England. However, the last two occasions have seen big moves after the press conference given by Draghi. The euro is weaker (2% on broad measure, 4% vs. USD), so in some ways the pressure is off the ECB to ease policy. More: The key to an ECB rate cut is the unwinding of the LTRO

- USD: The claims and trade data are of low risk. The bigger focus is on the change in FX dynamics, given the stronger dollar coming at the same time as equities are rallying. This is where the bigger risk lies.

- GBP: Sterling will be decidedly nervous at the BoE decision. Around a quarter of institutions surveyed are looking for more quantitative easing (mostly GBP 25bln more), but other surveys suggest ‘the street’ could be more strongly positioned for a policy move. No change could see cable rally up to ½ big figure.

Idea of the Day

We’ve said it often, but the first rule of forex is “nothing lasts foreverâ€. As such, the fact that both equities and equities were rallying yesterday is one of the talking points as we head into the key risk events of today (interest rate decisions in UK and Eurozone) and tomorrow (US employment report). The dollar index was up 0.45% yesterday and on only 30% of occasions over the past two years when we’ve seen a rise of this magnitude or more have we see equities move in the same direction. It highlights one of the themes we have been talking about for some time now, namely the change in the risk dynamics, with a move away from better data being dollar negative because investors seek risk assets elsewhere. Tomorrow’s employment report will be the real test of this new dynamic.

Latest FX News

- EUR:  The single currency put up one of the better fights against the stronger dollar tone seen late in the European session and overnight and currently trying to claw back to the 1.30 level. Italy is still struggling to form a government, but Italian bond yields have fallen from the highs near to 4.90%,

- JPY: There was 8:1 vote to keep policy steady at the BoJ meeting, with one member dissenting in favour of starting open-ended asset purchases now (vs. next year). This was last meeting with out-going governor Shirakawa, so expectations were low for any big announcements. The yen is steady after Wednesday’s late dollar surge.

- GBP: Â Sterling was one of the bigger losers in the dollar surge, nudging cable back below the 1.50 level. There are clearly nerves ahead of the BoE meeting today, where expansion of asset purchases remains the risk.

- AUD: The trade balance was worse than expected at AUD 1.1bln, but this followed on from a sharp improvement in December. The market was little moved, the AUD regaining some lost ground from yesterday to 1.0250.