The Federal Reserve’s tapering is underway. The central bank’s quantitative easing (QE) program that generated record levels of monetary liquidity in recent years is on track to fade into history by the end of the year. The approaching demise of QE lays the groundwork for what’s widely expected to be the first interest rate hike sometime next year, probably around mid-2015, based on the consensus projection. The details and timing still depend on the incoming economic data, of course, as Fed Chair Janet Yellen reminded last week. But barring a run of weak numbers, which looks unlikely at this point, it appears that the tapering will roll on.

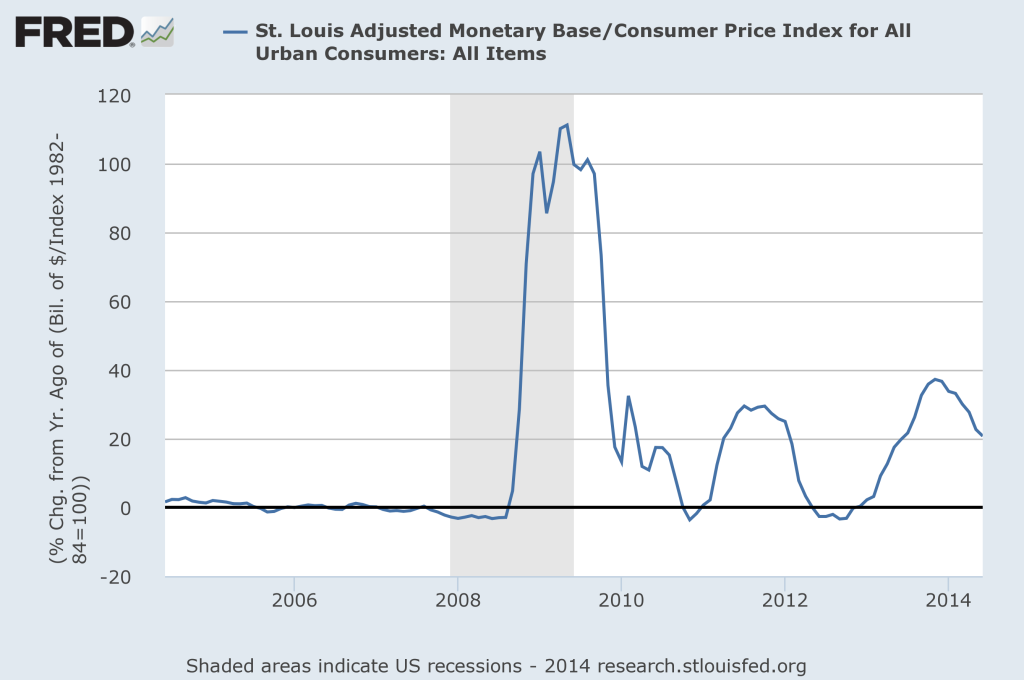

We can see this process unfolding in the ongoing deceleration in the year-over-year growth of real (inflation-adjusted) base money supply, a critical variable for assessing business cycle risk (see the chart here, for instance). As of last month, the real monetary base increased 20.7% vs a year ago. By historical standards that’s high, but in the post-2008 world of QE it’s middling. More importantly, the ongoing deceleration is telling us that the Fed really is tapering and has been for months. As recently as last November, real money supply was rising at roughly 37.5% a year, or nearly twice as high as the current increase.

The great mystery here is how the economy fares amid a sharp deceleration in the growth rate of the monetary base. The Fed has engineered such a slowdown before in the post-2008 era with less-than-encouraging results on the macro front. Will this time be any different? So far, the results look encouraging. Economic growth is holding up despite the falling pace of real money growth. But the outcome of this grand experiment is a work in progress and so the final verdict has yet to be written.

For now, at least, it seems that the central bank is successfully navigating the tricky waters of winding down monetary stimulus without materially impairing economic growth. It’s anyone’s guess if the Fed can continue to occupy this sweet spot, but so far, so good, at least through last month.