The United States

Investors around the world continue to focus on the US elections, with the latest Clinton/FBI news injecting a fresh dose of risk appetite into the global markets. Here is what the betting markets are telling us as of the late evening on Monday.

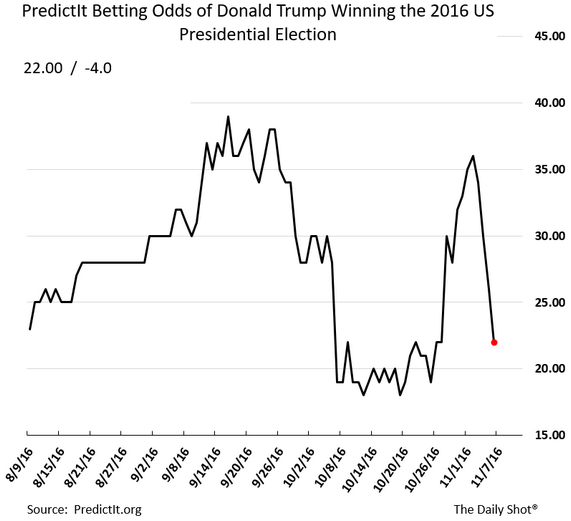

•Donald Trump victory odds over time (from PredictIt).

•PredictIt betting odds electoral map.

Source: @PredictIt;Â Further reading

•Electoral map based on Betfair betting odds.

Source:Â Maxim Lott and John Stossel (Fox News)

With risk appetite returning in response to reduced political uncertainty, the S&P500 had the best day since March.

The yen, which usually weakens against the dollar when risk appetite improves, dropped 1.3%.

The declining chances of a Trump victory sent the probability of a December rate hike to 82% – the highest in almost a year.

Historically, here is how US elections impacted uncertainty, the stock market, and credit risk in the past.

Source: @JoshZumbrun, @NickTimiraos, @Tmp_Research;Â Read full article

Next, let’s take a look at other economic developments in the United States.

1. Consumer debt (excluding mortgages) rose more than expected – shown as a percentage of the GDP below.

A good portion of this increase was from student loans. The chart below shows student debt directly owned by the federal government, which has now exceeded $1 trillion. Note that the total student debt outstanding (including debt that is guaranteed by the government) is about $1.4 trillion.

Another significant contributor is auto debt (shown adjusted for the population growth below). This trend is how the near-record auto sales in the US have been financed.

2. The latest data from Moody’s suggests that the US apartment market tightness is easing. Hopefully, this will result in the leveling off in the shelter CPI.

Source: Moody’s Investors Service, @joshdigga

3. As discussed yesterday, wage acceleration is likely to be concentrated in the skilled/managerial component of the labor market. Credit Suisse points out that this is the case in manufacturing.

Source: Credit Suisse, @NickatFP, @joshdigga

4. The Fed’s labor market conditions index has stabilized but remains below the post-recession average.Â