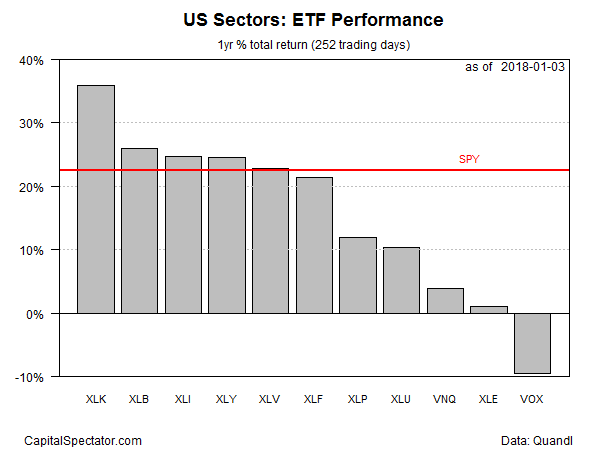

Technology shares continue to post the strongest trend performance for US equity sectors, based on a set of ETFs ranked by one-year return. Although most sectors are posting year-over-year gains, the annual pace for tech remains notable for its outsized advance vs. the rest of the field.

Technology Select Sector SPDR (XLK) is up a strong 35.8% for the year through yesterday (Jan. 3). The current gain is close to the ETF’s highest one-year total return since the recession ended in 2009. (At one point in last year’s fourth quarter, XLK’s rolling one-year change briefly accelerated to just under 40%, a cyclical peak for the post-recession period.)

XLK’s current upside momentum for the one-year gain is well above the number-two performer: stocks in the materials sector. The Materials Select Sector SPDR (XLB) is up 25.9% on a total return basis over the past 12 months – a solid increase, but no match for tech’s surge.

Although all but one of the 11 sectors are posting one-year gains, only five are beating the broad market, based on the SPDR S&P 500 (SPY), which is currently posting a 22.4% total return for the trailing one-year period.

The lone sector with a negative one-year trend at the moment: telecom. The Vanguard Telecommunication Services (VOX) was down 9.5% at yesterday’s close vs. the year-earlier level. In fact, VOX’s rolling one-year total return has been consistently negative every day since Dec. 5.

Â

The performance chart below presents a visual summary of tech’s dominance in recent history. Although most sector trends are positive, XLK’s run (black line at top of graph) stands apart as unusually bullish.

Â

Ranking the sector ETFs by current price relative to 200-day moving average reveals a more egalitarian profile. Although XLK’s latest price has the biggest premium over its 200-day average (12.8%), five other sectors are in close pursuit on that score. Note, too, that energy (XLE) is the current leader for the biggest premium over the 50-day average — is that a sign that the sector’s modest one-year gain (a thin 1.1%) is poised to rise in the months ahead?