One of the most common expressions in the investment world is that “one day does not a trend make.†Indeed, it would be foolhardy to over-analyze the stock and bond market reaction to the initial estimate of 4% economic growth in the 2nd quarter. What is more instructive in determining the attractiveness of asset classes in your portfolio are their current prices in relation to longer-term moving averages (a.k.a. trendlines).

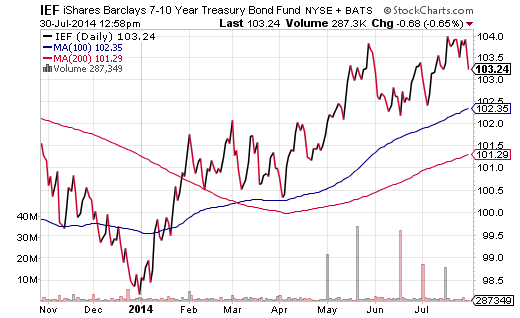

For example, the 10-year yield rocketed higher on the upbeat economic news, smashing bond exchange-traded funds like iShares 7-10 Year U.S. Treasury Bond Fund (IEF). The fear? A rapidly expanding economy implies that the Federal Reserve will have to raise interest rates sooner rather than later. However, an elongated perspective on the viability of government bonds in your portfolio tells a different story. The iShares 7-10 Year U.S. Treasury Bond Fund (IEF) remains above its intermediate (100-day) and long-term (200-day) trendlines. Unrealized year-to-date gains of 5.1% provided ample reward for far less risk than owning stock assets alone.

Â

Â

Nearly every economist and analyst at the start of the year believed that the 10-year yield would climb from roughly 3.0% to 3.4%. While it may transpire before the year is out, you would have struggled to find a solitary soul who would have predicted that the 10-year would fall from 3.0% to 2.45% beforehand. That’s why visualizing the progress of a fund like IEF – as it pierced its 100-day in mid-January and its 200-day in late January – benefits an asset allocator who is looking to put cash to work.

Paying attention to moving averages will not help you “call†stock or bond market bottoms, let alone give you divinely inspired foresight into market tops. However, they will help you sharpen your investing decisions as well as ignore day-to-day noise.

Consider a second example – small company U.S. stocks in the Russell 2000. The iShares Russell 2000 (IWM) responded more favorably to the strong economic data today than large company stocks in the S&P 500. Yet a “big picture†view sees that IWM has experienced three pullbacks of 7% or more since the start of the year. The current price of IWM is below its 100-day, while the slope of the trendline itself has turned negative. Excluding dividends, the S&P 500 lays claim to 6.5% unrealized gains in 2014 whereas the the Russell 2000 is flat in 2014.