“It’s dangerous to be short still, but we might be building toward a moment where the market becomes quite vulnerable,” warns Bill Fleckenstein who is finishing up the documentation on a new short fund he is about to start marketing. With the slowing growth of the Fed balance sheet, over 70% of the S&P’s gains since 2011 from hope-driven multiple-expansion alone, bond and equity market sentiment at extremes, and (as Goldman warned) valuations anything cheap, it is hardly surprising that, as Reuters reports, after years of hiding under their desks, short sellers are re-emerging – slowly.

Whether outright short or long/short funds, the market-share of this corner of the business bottomed at approximately 25% in 2013, but in the last weeks, several S&P 500 companies have seen large increases in shares borrowed for short bets; and the “tide might be turning.”

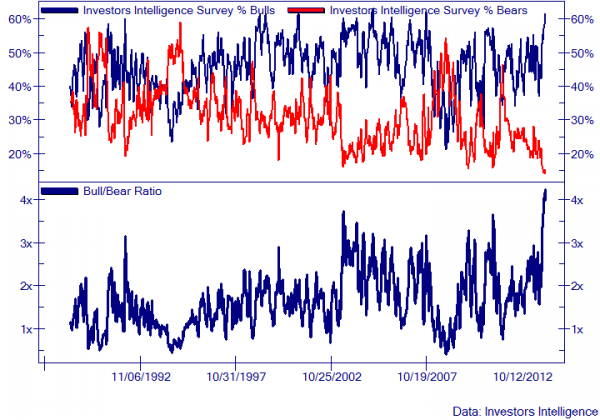

Sentiment equity market sentiment at extremes…

and bond…

Â

Â

Fed balance sheet growth slowing and dislocated from the equity exuberance…

Â

Multiple-expansion the only hope left…

Â

And (as Goldman warned) valuations anything cheap…

S&P 500 valuation is lofty by almost any measure, both for the aggregate market (15.9x) as well as the median stock (16.8x). We believe S&P 500 trades close to fair value and the forward path will depend on profit growth rather than P/E expansion. However, many clients argue that the P/E multiple will continue to rise in 2014 with 17x or 18x often cited, with some investors arguing for 20x. We explore valuation using various approaches. We conclude that further P/E expansion will be difficult to achieve. Of course, it is possible. It is just not probable based on history.

The current valuation of the S&P 500 is lofty by almost any measure, both for the aggregate market as well as the median stock: (1) The P/E ratio; (2) the current P/E expansion cycle; (3) EV/Sales; (4) EV/EBITDA; (5) Free Cash Flow yield; (6) Price/Book as well as the ROE and P/B relationship; and compared with the levels of (6) inflation; (7)

nominal 10-year Treasury yields; and (8) real interest rates. Furthermore, the cyclically-adjusted P/E ratio suggests the S&P 500 is currently 30% overvalued in terms of (9) Operating EPS and (10) about 45% overvalued using As Reported earnings