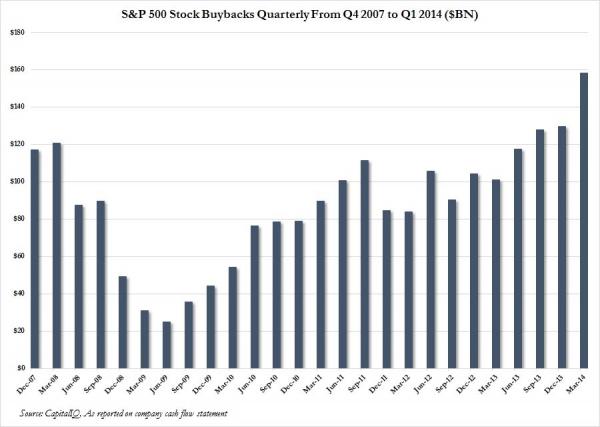

It was a month ago when Zero Hedge first revealed that as QE was “tapering”, a just as powerful and even more indiscriminate force had stepped in to make up for the loss of Fed buying of last resort: corporations themselves, almost exclusively on a levered basis (issuing debt whose use of proceeds are stock buybacks). Specifically, we showed that the total amount of stock bought back by corporations in Q1 was the highest since the bursting of the last credit bubble. In fact it was the highest ever.

This was promptly noticed by both the WSJ and the FT. What the two financial media outlets likely have not grasped is that based on trading desk commentary, according to which the bulk of “flow” now originates almost exclusively at C-suites ordering banks to continue the buyback activity, the Q2 stock repurchase totals will be even greater than Q1, and likely surpass $200 billion. This means that every month this quarter companies are buying back about $70 billion of their own stock: an amount which at this runrate will surpass the Fed’s original QE(3) amount of $85 billion within a quarter!

But while the “Zero Hedge first revealed ” buyer of US stocks has been fully unmasked now, what most likely do not know is that just this is happening at a comparable record pace nowhere else but the place which is mirroring and repeating every single Fed mistake tit for tit.

Japan.

According to Bloomberg, companies in the Topix index are acquiring their own stock at the fastest pace ever, led by NTT Docomo Inc. and Toyota Motor Corp., with $25 billion of announced purchases so far this year, data compiled by Bloomberg show. The buybacks are limiting losses in the world’s worst-performing developed equity market: Companies using the strategy have gained even as the Topix slid.

Only $25 billion you say? Why that is less than a fifth of what their US peers are doing. Well, yes. But remember that on a relative basis, the BOJ’s $75 billion or so in QE is orders of magnitude greater than the Fed’s own QE when one factors in the relative sizes of the US and Japanese stock markets.

Additionally, keep in mind that the net annual bond issuance in Japan is already well below half of the amount monetized every year by the BOJ (which means if you think US bonds are illiquid, just try to buy, or sell a JGB – good luck). This means that vastly more of the BOJ’s intervention ends up in the stock market: either Japan’s or that of the US, courtesy of immediately fungible global fund transfers.