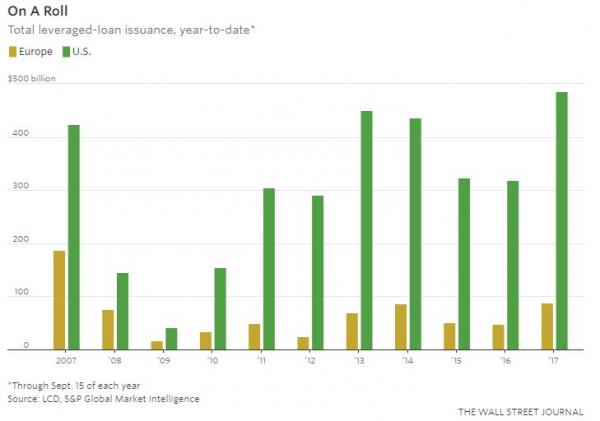

If a surge in covenant-lite levered loans is any indication that debt and equity markets are nearing the final stages of their bubbly ascent, then perhaps now is a good time for investors to take their profits and run. As the Wall Street Journal points out this morning, levered loans volumes in the U.S. are once again surging, eclipsing even 2007 levels, despite the complete implosion of bricks-and-mortar retailers and continued warnings that “the market is getting frothy.”

Volume for these leveraged loans is up 53% this year in the U.S., putting it on pace to surpass the 2007 record of $534 billion, according to S&P Global Market Intelligence’s LCD unit.

In Europe, recent loans offer fewer investor safeguards than in the past. This year, 70% of the region’s new leveraged loans are known as covenant-lite, according to LCD, more than triple the number four years ago. Covenants are the terms in a loan’s contract that offer investor protections, such as provisions on borrowers’ ability to take on more debt or invest in projects.

“If feels like the market is getting frothy,†said Henrik Johnsson, co-head of global debt-capital markets at Deutsche Bank AG . “We’re overdue a correction.â€

Meanwhile, volumes are surging even as traditional lender protections have become basically nonexistent.As S&P LCD points out, over 70% of levered loans issued so far in 2017 are considered “covenant-lite” versus only 30% of those issued in 2007.

Before the financial crisis, the boom in leveraged loans was one of the signs of markets overheating. As the crisis intensified in 2008, investors in U.S. leveraged loans lost nearly 30%, according to the S&P/LSTA Leveraged Loan Index.

Regulators are taking note. In its last quarterly report, the Bank for International Settlements noted the growth of covenant-lite loans and pointed out that U.S. companies are more leveraged than at any time since the beginning of the millennium. That could harm the economy in the event of a downturn or a rise in interest rates, said the BIS consortium of central banks.

The leveraged loan market has long been favored by private-equity firms raising cash to fund company takeovers. Investment banks arrange the loans and typically parcel them out to other lenders and investors.

Loan terms are now “more aggressive here in Europe,†said Christopher Kandel, a partner at law firm Latham & Watkins LLP, citing provisions giving borrowers greater flexibility to pay out dividends or incur additional debt.

Cov-lite loans barely existed in Europe before the financial crisis. “That will be the test for investors,†said Taron Wade, a director at S&P Global. “How they perform through the cycle.â€