Â

Our June 2014 Economic Forecast continues to show a strengthening economy – this general strengthening cycle began 12 months ago with one small dip at the beginning of 2014. All portions of the economy outside our economic model – except housing – are showing expansion. Â

- Since the end of the 2007 Great Recession, our economic index has been on a roller coaster of highs and lows. Why is the economy pulsing when it did not prior to the Great Recession? – May be caused by the extraordinary monetary policy.

- The consumer portion of the economy is lagging the growth of the business sector.

- The personal income year-over-year percentage growth rate (first derivative of monetary value) compared with personal expenditures has closed – but in monetary terms there remains a gap which is still growing. Econintersect considers that this will sideline the consumer’s contribution to economic growth. Note that the quantitative analysis which builds our model does not include personal income or expenditures.

- Another data point – the correlation between retail sales and employment remains weak. This by itself is not a recession flag, but a warning that the economy is not healthy. Note that neither employment nor personal income are part of our economic model.

- Also real estate continues to soften – and sales are contracting year-over-year. Real estate can not be used as an economic forecasting tool as it has a mixed record in predicting the economy or modeling economic growth. However, this begs several questions including the dynamics which are causing real estate contraction.Â

- And another data point – our Joe Sixpack index – is saying poor Joe is no longer better off than he was in the previous period.

- Econintersect checks its forecast using several alternate monetary based methods – and all the check forecasts are similar to our forecast.

- Note that all the graphics in this post auto-update. The words are fixed on the day of publishing, and therefore you might note a conflict between the words and the graphs due to backward data revisions and/or new data which occurs during the month.

This post will summarize the:

- special indicators,

- leading indicators,

- predictive portions of coincident indicators,

- review of the technical recession indicators, and

- interpretation of our own index – Econintersect Economic Index (EEI) – which is built of mostly non-monetary “things†that have been shown to be indicative of direction of the Main Street economy at least 30 days in advance.

Special Indicators:

The consumer is still consuming. The USA remains in only the fourth period in history where the ratio of spending to income has exceeded 0.92 (April 1987, the months surrounding the 2001 recession, from September 2004 to the beginning of the 2007 Great Recession, and now). This high ratio of spending to income will act as a constraint to any major gain in consumer spending .

Seasonally Adjusted Spending’s Ratio to Income (a increasing ratio means Consumer is spending more of Income)

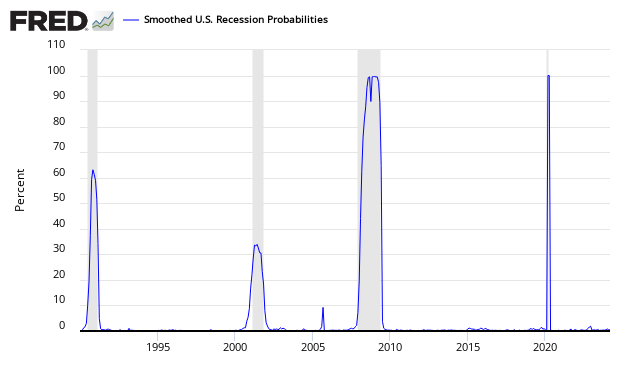

The St. Louis Fed produces a Smoothed U.S. Recession Probabilities Chart which is currently giving no indication of a recession.

Smoothed recession probabilities for the United States are obtained from a dynamic-factor markov-switching model applied to four monthly coincident variables: non-farm payroll employment, the index of industrial production, real personal income excluding transfer payments, and real manufacturing and trade sales. This model was originally developed in Chauvet, M., “An Economic Characterization of Business Cycle Dynamics with Factor Structure and Regime Switching,†International Economic Review, 1998, 39, 969-996. (http://faculty.ucr.edu/~chauvet/ier.pdf)

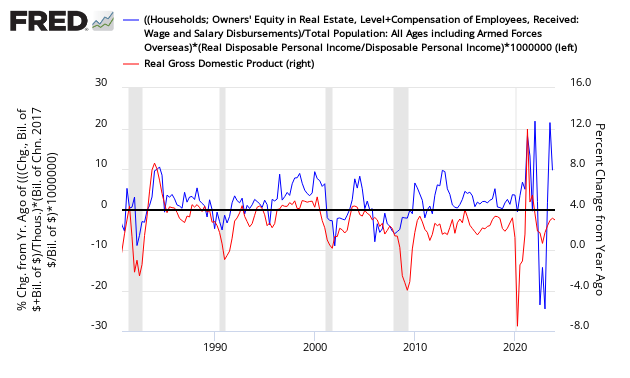

Joe Sixpack’s economic position is no longer strengthening (blue line in graph below). The Econintersect index’s underlying principle is to estimate how well off Joe feels. The index was documented at a bottom in the July 2012 forecast. Joe and his richer friends are the economic drivers. Joe is close to the levels associated with past recessions. However, note that this index has falsely warned of recessions that never occurred. This index is updated every quarter.

Joe Sixpack Index (blue line, left axis)

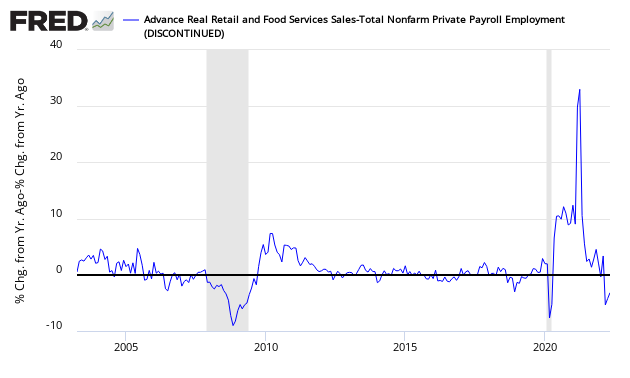

Econintersect reviews the relationship between the year-over-year growth rate of non-farm private employment and the year-over-year real growth rate of retail sales. This index is barely positive. As long as retail sales grow faster than the rate of employment gains (above zero on the below graph) – a recession is not imminent.

Growth Relationship Between Retail Sales and Non-Farm Private Employment – Above zero suggests economic expansion

- Most economic releases are based on seasonally adjusted data which is revised for months after issuance so an actual contraction in a particular release may not be obvious for many months due to seasonality methodology which smooths the data. No special indicator is particularly strong – and continues to show an economy not running on all cylinders.