Reminding us of what McKinsey reported over a year ago, namely that the world never deleveraged after the financial crisis, Citi’s Hans Lorenzen released a fascinating presentation today discussing the “invincible” stock rally, and pointing out its Achilles heel, which happens to be the thing that made it possible in the first place:Â central banks.

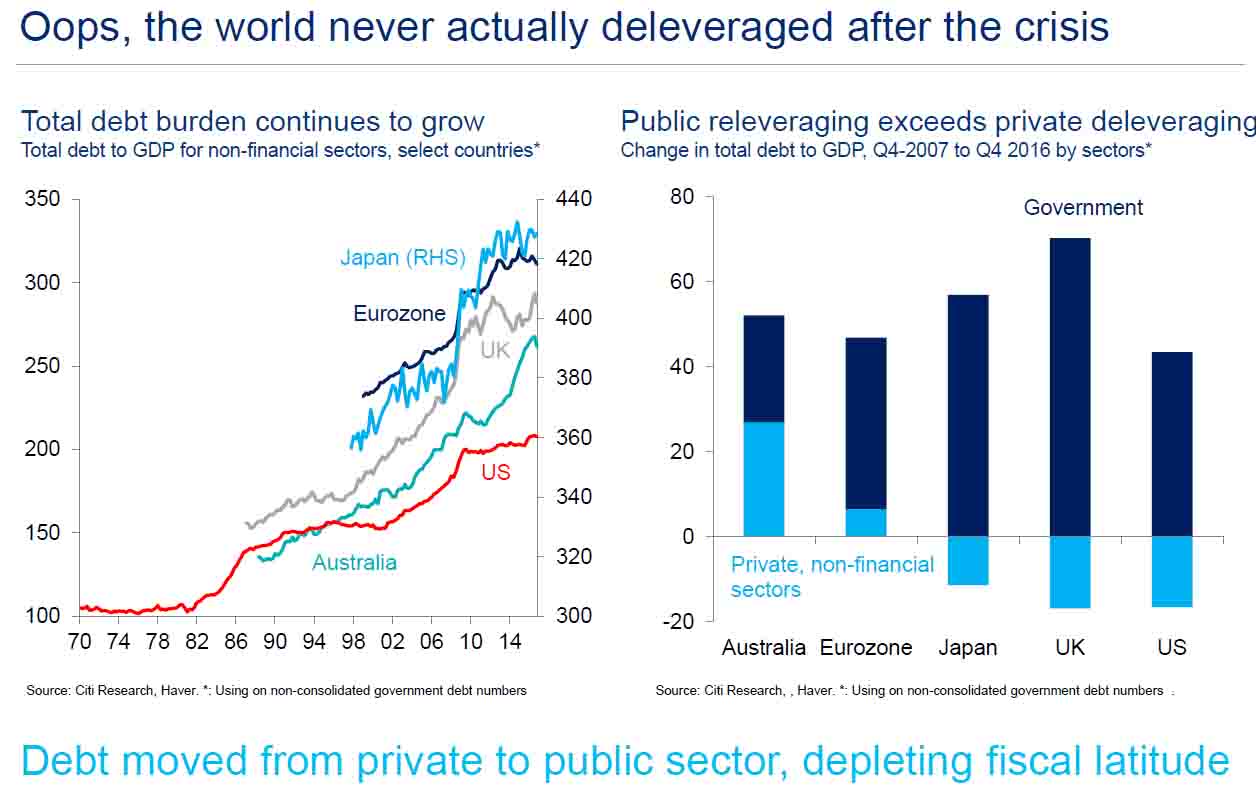

As the first charts below show, the permissive factor that allowed the world to “emerge” from the financial crisis and the global recession, was a surge in debt, which on a consolidated basis is above 360% of GDP in all five select developed regions. The chart on the right shows that while private sector releveraging has been slow, it has been drowned out by a historic surge in public sector debt.

(Click on image to enlarge)

What made this coordinated global releveraging possible? Central banks of course, who have bought over $10 trillion in public (and recently private) sector debt in the past decade, and between the world’s six largest central banks they now collectively own securities amounting to 40% of the world’s GDP.

However, it is this same unprecedented central bank balance sheet expansion that is now the biggest threat to not only the global recovery and ongoing attempts to stimulate the much-needed reflation (if only to inflate away the world’s debt load), but also to capital markets around the globe.

Which bring us to what may be the scariest chart for central bankers: Citi’s forecast of what happens to the global central bank “impulse”, or annual change, over the next two years and – as Lorenzen shows – its correlation to inflation expectations via real 5Y5Y forwards. The chart clearly shows the recent contraction in global central bank assets (including Chinese FX reserves) which took place as deflation fears swept the globe and as global stocks tumbled in late 2015 and early 2016. More importantly, the chart projects when the next such contraction is expected to take place…