One of the closed-end funds that seems to be a recurrent favorite on our watch list is the DoubleLine Opportunistic Credit Fund (DBL), run by Jeffrey Gundlach of DoubleLine Capital.This unique actively managed portfolio was the first of its kind to debut from DoubleLine back in 2012 and has developed a cult following among CEF investors.

DBL primarily invests in a mixed basket of mortgage backed securities, collateralized loan obligations and other asset backed securities. The fund has just over $325 million in total assets with a relatively tame 16% leverage ratio to boost its net exposure.It currently yields over 8% annually and income is paid monthly to shareholders.Â

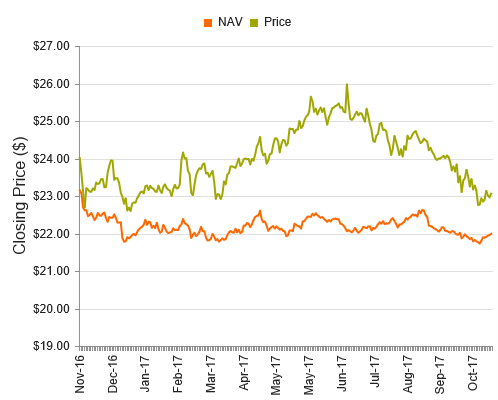

We don’t currently own any exposure to DBL for clients of our firm and have been wary of its fundamental analytics for some time now. This stems primarily from the above-average premium over the last 52-weeks in addition to the underperformance of its underlying portfolio relative to the category this year.

(Source: CEFconnect.com)

Although we have seen the premium in DBL recently collapse to some of the narrowest levels in the last nine months, there are other concerning factors that are beginning to crop up on our radar as well. The squeeze in credit spreads, alongside the relatively low interest rate environment, has created an inability of the fund to meet its existing distribution rate.Furthermore, without a firm buffer of undistributed net investment income (UNII), it’s relying on return of capital (ROC) in the short-term to meet its distribution policies.

According to Morningstar, DBL has identified a portion of its dividend as return of capital in the last four consecutive months. All income prior to August had been driven entirely by the bonds in the underlying portfolio. Situations like these are often a precursor to a dividend cut to re-align the income stream with realistic expectations and create a healthier long-term sustainability plan.