Our HSBCÂ research report released September of 2016 has proven to be 110% correct. This is the first sentence of our report:

HSBC Common Equity Returns: Notwithstanding a possible boost from significant depreciation of the pound and their beating (already lowered) analysts’ expectations, it looks as if the market has not sufficiently discounted HSBC’s price given it’s extremely negative fundamental, credit and macro outlook.Â

This morning the company reports an 82% drop in year over year earnings. Bloomberg reports HSBC Plunges After Missing Profit Estimates on Revenue Drop

HSBCÂ Holdings Plc dropped the most in 18 months in London trading after reporting fourth-quarter profit that missed estimates on a surprise drop in revenue, which it warned could fall again this…

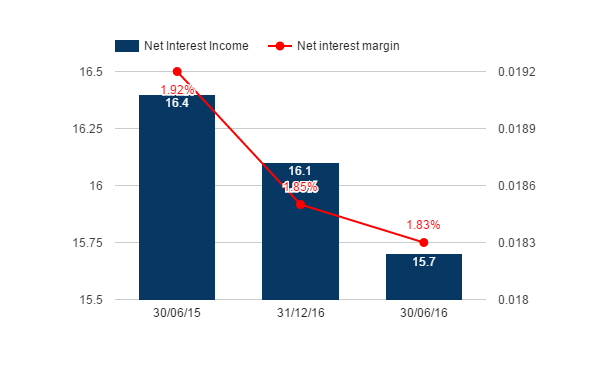

Net Interest income (US$ billion)

The bank had no less than 6 “one off” expenses and $6 billion worth of of write-downs where analysts were only expecting $1 billion. Of course, we clearly anticipated such, as you can see below.Â

“Pretax profit is a large miss versus consensus†with “weakness in revenues across all major line items,†Citigroup Inc.’s Ronit Ghose said in a note titled “Weak Revenues, Messy Quarter.†Ghose also noted “an unusually large amount of one-offs†in the period, including a multibillion-dollar writedown on the value of its scandal-hit European private bank.

HSBC Holding PLC

|

Date |

1 M |

3M |

6M |

YTD |

1Y |

|

06/08/16 |

15.27% |

10.34% |

4.41% |

-12.37% |

-22.8% |

Notably, GBP has depreciated against dollar by ~15% in the last month. This might have contributed to appreciation of HSBC stock price since July 7, 2016 till Aug 6, 2016.

Financial Results – 2Q2016:

-

HSBC Holdings PLC reported a decline of ~29% in their reported profit before tax. Reported PBT was totaled at USD9.7 billion in 2Q2016 Â versus US$13.6 billion in 2Q2015

-

Similarly the bank’s revenue also fell down 11% to US$29.5 billion in 2Q2016 compared to US$32.9 billion in 2Q2015

-

HSBC reported an increase of 64% in total loan impairment and other credit risk provisions to US$2.4 billion in 2Q2016 from US$1.4 billion in 2Q2015

-

As per the bank’s Group Chief Executive Stuart Gulliver HSBC is going to buy back up to $2.5bn of its shares this year and hopes for another buyback in 2017. This is an absolutely silly use of capital given the decline in fundamentals, worsening credit metrics and deteriorating macro environment! A move whose only possible justification is to place investor perception of per share metrics.

-

The bank also stepped back from its dividend policy which implied a payout ratio of 8%

-

Risk-weighted assets (RWA) reduced by $21bn or 2% to US$1,082 billion as of June 30, 2016 mainly because of targeted RWA initiatives and the effects of currency translation in 1H2016. RWA initiatives resulted in a reduction of $48bn and included asset sales in the GB&M legacy and US CML run-off portfolios, reduced exposures, refined calculations and process improvements