A year ago the Bitcoin was the buzz.  An analyst from a major bank urged central banks to buy some for reserve purposes, completely ignoring the fact that there were not Bitcoin bonds, the market lacked transparency and was far too small. Another analyst tried to calculate intrinsic value of Bitcoins and came up with something well north of prevailing prices.  Â

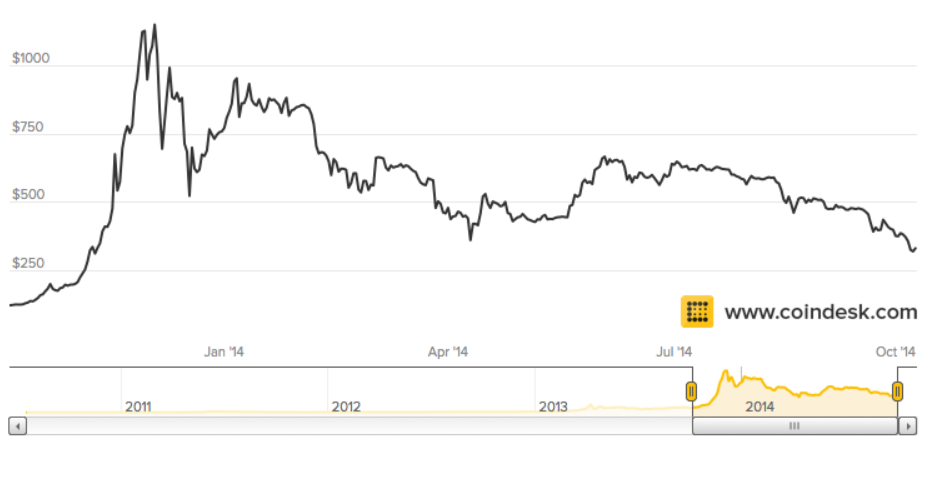

This Great Graphic was tweeted by Yahoo’s Jeff Macke, and he got it from coindesk.com. It shows the large downtrend in the Bitcoin’s value this year. In fact, the Bitcoin is making a new low for the year today (though the dollar is also somewhat softer on the day).

Yes, there is still a Bitcoin eco-system, but it has lost the buzz. It seems more like a quaint niche artifact. Yes there some shops and electronic vendors who will accept it in lieu of payment, but it seems this is more a a marketing ploy than an secession from sovereign money. The payment system technology may have some merit and this may be its real legacy. Â

At the end of September, the IMF published its latest reserve figures (COFER) for Q2. Global reserves rose $134 bln after adjusting for exchange rate movement. This is down from $166 bln in Q1 14. The euro’s share of reserves slipped to 24.2% from 25.0%. This was the sharpest drop in euro allocation since 2011. Speculators in the futures market had swung to a net short euro position in mid-May, arguably responding to the same fundamental considerations as the central banks. Â

The US dollar’s share rose to 60.7% from 60.3% of reserves. The Australian and Canadian dollar’s share of reserves edged higher, as did the “other “category (which likely includes the Scandis, the New Zealand dollar, the Singapore dollar, Korean won and Danish krone). While many observers still talk about the diminished role for the dollar, we suspect the risk is in the opposite direction.

The role of the dollar may be enhanced in the coming years as the main alternative, the euro, is again hobbled and depreciation a 2-3 year time frame looks more likely.  What are central banks interested in : liquidity, safety and then returns. US yields may rise on a medium and long-term view, but this may be more than offset by currency appreciation. Although the long term demise of the dollar is the widely held view, medium and long-term investors should consider the opposite scenario.Â