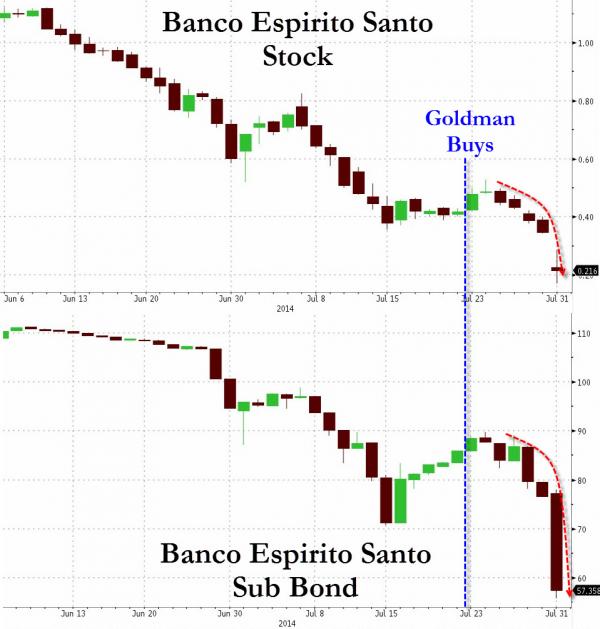

A week ago, investors were exuberantly buying Banco Espirito Santo (BES) stocks and bonds on the back of disclosures from Goldman Sachs that they have bought stakes in the bank “by virtue of its client transactions.” This morning, Goldman along with its muppeted clients (and hedge funds D.E.Shaw and Baupost) are licking their falling-knife-catching wounds as the stock of BES is down over 50% to new record lows and its bonds have cratered nearly 20 points to 57, after announcing a stunning $5 billion loss. Exuberance has turned to fear over ‘burden-sharing’ and bail-ins across the capital structure.

As Bloomberg reports,

Concerns persist over possible burden-sharing for subordinated debt, and even senior debt, after BES loss, CreditSights analysts John Raymond and Puja Poojara write in client note.

1H loss was as bad as anticipated, and lack of firm details on how CET1 will be returned to levels consistent with AQR, and surprise losses related to repackaged bonds and special purpose entities suggest situation is worse

Absence of concrete information on any capital support that may be in works, and on whether reported backing continues: CreditSights

With CET1 capital ratio at 5%, and 8% likely the requirement for both local regulator and baseline in ECB stress test, calculates needs of EU4b to boost capital to ~EU7b and transitional ratio to >11.5% before stress test

*Â *Â *

The bottom line – this is not going to get any better anytime soon as once again the European ‘rules’ are set to be changed and the ‘template’ from Cyprus maybe applied.