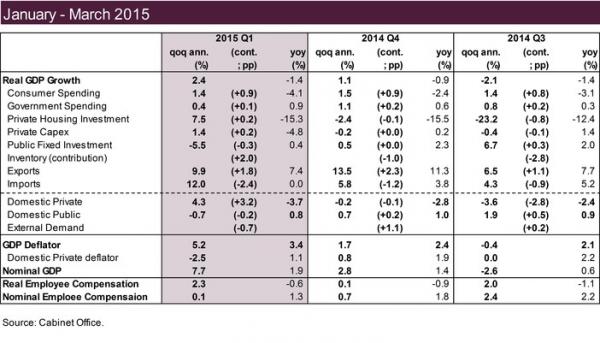

The only remarkable macroeconomic news overnight was out of Japan where we got the Q1 GDP print of 2.4% coming in well above consensus of 1.6%, and higher than the 1.1% in Q4. Did it not snow in Japan this winter? Does Japan already used double, and maybe triple, “seasonally-adjusted” data? We don’t know, but we do know that both Japan and Europe have grown far faster than the US in the first quarter.

And yet after briefly sliding on this “better than expected” news, the USDJPY ramped up to a multi-month high as the algos seemingly smelled a rat. And indeed, even a cursory look behind the numbers revealed that just like in the US, well over 80% of the “growth” was as a result of a massive inventory restocking, which contributed to 2.0% of the final 2.4% print, suggesting that Q2 GDP may once again be negative if imports continue to be a substantial detractor to growth.

Â

Aside from Japan, it has been a quiet session, with an odd plunge in the EURUSD right around the time the ECB released its delayed press release from the Coeure private meeting with hedge funds the day before. One wonders what the ECB may have leaked to asset managers this time. We will never know, of course, until the “people’s” central bank decides to advise its non-hedge fund clients.

Volumes remain depressingly low which as even the dumbest algo by now know is a green light to resume levitation, and sure enough, after treading water overnight, the ES is now starting its gradual, daily climb higher.

On the key news front, we finally got the terms of the latest and greatest UBS as a “recidivist” settlement with the US government, over Libor, Gold, FX rigging, this time paying $545 million, getting slapped with a 3 year probation this time – one which the bank will promptly flaunt – and not getting criminal charged. In other words, business as usual.

The main other newsflow continues to revolve around Greece, which again reiterated it will not make its June 5 payment to the IMF without more aid (from the IMF) and where the ECB’s Governing Council is set to meet today to debate whether to tighten rules on Greek access to Emergency Liquidity Assistance as the country veers toward default. As Bloomberg reports, the ECB may “imminently†raise discount it applies to collateral Greek banks pledge in exchange for Emergency Liquidity Assistance, Kathimerini newspaper reports, without citing anyone; ECB will, at the same time, expand pool of assets it accepts as collateral.

According to an MNI leak, which lately have been 100% wrong as they serve merely some conflicted hedge fund “source” to exit positions, the Bank of Greece has been said to accept an extra €6 billion in ELA, with the ECB somehow agreeing to accept government-guaranteed bank bonds as collateral. Somehow we very much doubt this.

Far more notable was a note by Moodys, which offloaded on Greek banks and said there is a high likelihood of a deposit freeze for Greek banks. Now even the rating agencies are desperate to accelerate the Greek bank run in hopes of overthrowing the government.

The key event looking ahead will be the FOMC Minutes for the April 28-29 meeting. Look for any instance of “double seasonal adjustment” which will be codeword that the Fed will raise rates oblivious of what the actual data represents.

Asian equities traded mixed following a lacklustre Wall Street close (S&P: -0.06%), as investors squared positions ahead of the FOMC minutes release. Shanghai Comp (+0.65%) continued to outperform, as participants eye the April 28th highs (4,572.39), this time lifted by IT, while the Hang Seng (-0.39%) was dragged lower by energy stocks. Nikkei 225 (+0.85%) touched a fresh 15yr high underpinned by Japanese Q1 Prelim GDP data, which showed the fastest quarterly growth in a year (0.6% vs. Exp. 0.4%, Prev. 0.4%). The ASX 200 (-0.09%) briefly broke below its 200 DMA in volatile trade, after a technical break below long-term support at 5,600.

Ahead of tomorrow’s Eurogroup two-day showdown on Greece, reports this morning in Greek press suggested raising haircuts and widening the asset pool accepted by the ECB are to be discussed at today’s ECB non-monetary policy meeting. This, as well as comments from the Greek Parliamentary Speaker that if a deal is not reached, Greece will not pay its June 5th debt obligation to the IMF weighed on equities, while bolstering Bunds.

Major European equity indices all now trade in the red (Euro Stoxx: -0.35%) after opening in mixed territory as news surrounding Greece guides sentiment, with the European calendar fairly light with the exception of this news and BoE minutes. US earnings today include Target and Lowe’s premarket and Salesforce.com aftermarket.

In fixed income markets, Bunds (+16 ticks) continue to outperform their US equivalent with USTs (-3 ticks) remaining weighed on by the large corporate issuance this month. Any source comments regarding Greece throughout the session could prove significant as the ECB are not expected to make any official statement, with any potential decisions to make their way to the market via source comments.