The US economy continued to churn out strong economic fundamentals but not enough to sustain dollar attractiveness amid rising tax concern. Retail sales rose 0.2 percent in October, indicating consumer spending remains healthy even with less desirable wage growth.

In the U.K, the economy has started showing signs of weakness following Prime Minister Theresa May failure to reach an agreement with the European Union. Retail sales dropped 0.3 percent year-on-year in October, while wage growth edge higher slightly to 2.2 percent in the third quarter. Still, this is below the 3 percent inflation rate that is eroding buying power.

In the Euro-area, the economy grew at 0.6 percent with consumer prices remaining steady at 1.4 percent, same as previous numbers.

This week, we will be reviewing six currency pairs as listed below;

AUD/USD

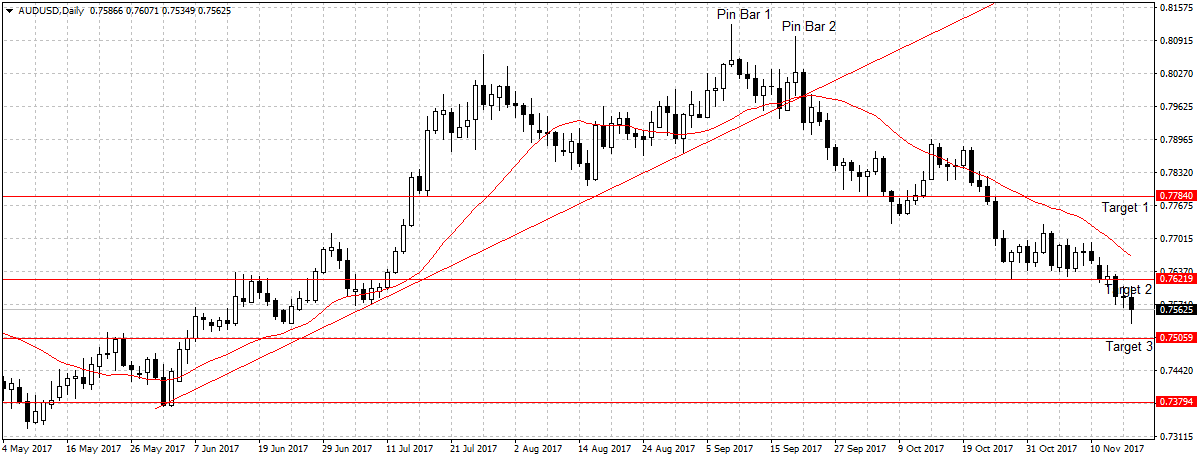

Australia created fewer jobs than expected in October but unemployment rate improved to 5.4 percent. Meaning, drop in the participation rate was what plunged unemployment rate to more than 4-year low and not state of the economy.

As previously stated, the Australian economy is struggling with weak wage growth and low inflation rate, this we expect to continue into 2018. Especially, with retailers cutting prices to boost demand and housing debt rising.

Â

Therefore, this week we remain bearish on AUD/USD and expect the success of House Republicans on tax reform to further aid AUD/USDÂ towards our third target at 0.7505.

NZD/USD

Last week, data shows New Zealand’s producer price index, both input and output, rose less than expected in the third quarter. Suggesting that price pressures are still low and likely to impede the Reserve Bank of New Zealand from raising rates in 2018.

Even though inflation rate was better than expected in the third quarter, 1.9 percent year-on-year. It was just above the mid of 1-3 percent projected by the apex bank. This is partly due to the decline in global dairy prices and weak exports.