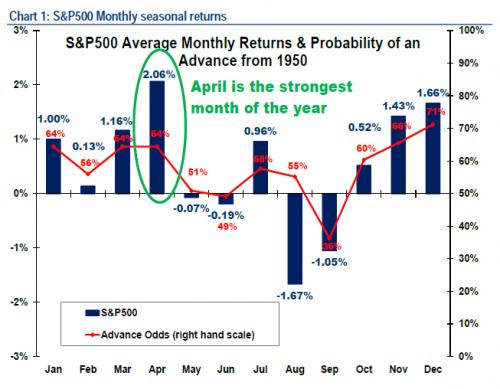

Both the entire month of March, and its last full week, particularly for biotech investors and especially hedge funds, is a time that many would rather forget and continue pretending that the saying “as January goes, so goes the year” is no longer applicable. Luckily, for all those bulls who have forgotten that in a normal market there is both return and risk, at least in pre-New Normal times, there may be some good news. As Bank of America’s chief technician MacNeil Curry reminds us, April is the least cruel month for stocks, posting the highest monthly average return since 1950, returning just over 2.0%.

From Curry, whose latest track record in market calls has hardly been successful:

We believe NOW ITS TIME TO DO AN ABOUT FACE and turn bullish risk assets for the next several weeks. From both a price and seasonal perspective, evidence says that the consolidation in the S&P500 is nearing completion and the larger bull trend is about to resume. Treasury yields should also participate as the week long consolidation in 5yr yields is drawing to a close.

That said, even the BofA analysts is starting to hedge quite aggressively: “Bigger picture, we are growing concerned that this equity rally is VERY mature and that US Treasury Vol is setting up for a significant breakout. But, to be clear, those are bigger picture concerns and NOT FOR THE HERE AND NOW.“

Maybe. Maybe not. Either way, here is what the historical data says.

April is the strongest month of the year for the S&P500. Since 1950 it has averaged OVER 2.00% for the month with the 3rd highest monthly probability of an advance at 64%

Of course, such Old Normal historical patterns are, as the name implies, not part of the NewNormal. Because nowhere in the past 64 years of chart data did the market have to deal with an unprecedented increase in the reduction (yes, second derivatives) of the growth of the Fed’s balance sheet. And never before has the entire global economy’s massive carry trade driven purely by several trillion in central bank liquidity injections been on the verge of unwinding, which as we have seen on two occasions already, had very adverse and dramatic consequences for the world’s emerging markets.