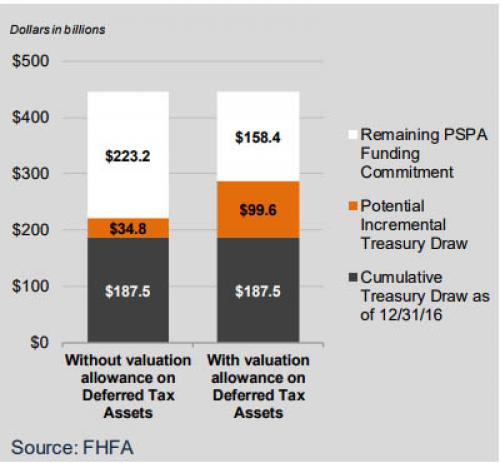

While the latest Fed stress test found that all US commercial banks have enough capital to survive even an “adverse” stress scenario, a severe recession in which the VIX hypothetically soars to 70, the two US mortgage giants would not be quite so lucky: according to the results from the annual stress test of Fannie Mae and Freddie Mac released by their regulator, the Federal Housing Finance Agency, the “GSEs” which were nationalized a decade ago in the early days of the crisis, would need as much as $100 billion in bailout funding in the form of a potential incremental Treasury draw, in the event of a new economic crisis.

Under the “severely adverse” scenario, i.e., a “severe global recession” U.S. real GDP begins to decline immediately and reaches a trough in the second quarter of 2018 after a decline of 6.50% from the pre-recession peak. The rate of unemployment increases from 4.7% to a peak of 10.0% in the third quarter of 2018. CPI declines to about 1.25% by the second quarter of 2017 (so not that much further from here) and then rises to approximately 1.75% by the middle of 2018. Outright deflation is not even considered.

In addition, equity prices fall by approximately 50% from the start of the planning horizon through the end of 2017, and equity volatility soars, approaching levels last seen in 2008. Home prices decline by approximately 25% , and commercial real estate prices fall by 35% through the first quarter of 2019.The Severely Adverse scenario also includes a global market shock component that impacts the Enterprises’ retained portfolios. The global market shock involves large and immediate changes in asset prices, interest rates, and spreads caused by general market dislocation, uncertainty in the global economy, and significant market illiquidity. Option-adjusted spreads on mortgage-backed securities widen significantly in this scenario.

Most interesting is the following provision in the “severly adverse” scenario: the global market shock also includes a counterparty default component that assumes the failure of each Enterprise’s largest counterparty. Which, of course, is ironic because the Fed’s own stress test of commercial banks did not anticipate any bank failing. The global market shock is treated as an instantaneous loss and reduction of capital in the first quarter of the planning horizon, and the scenario assumes no recovery of these losses by the Enterprises in future quarters.