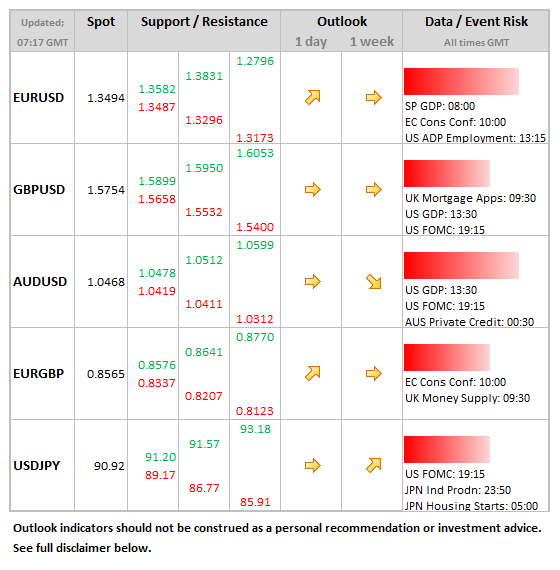

Data/Event Risks

Data/Event Risks

- EUR: Bit and pieces today in terms of releases, with SP GDP at 8:00, IT business confidence at 09:00, and EC consumer confidence at 10:00, to be followed by a myriad of US releases later on. Data not the main driver for the euro right now, but rather flow, or to be more precise, inflow, with 1.35 broken on EURUSD in early European trade.

- USD: Event risk ramps up today with ADP Employment at 13:15, followed by a first stab at Q4 GDP (market expects +1.1%) and then FOMC at 19:15. ADP will provide an important cue for Friday’s payrolls – if above 200K (last 215K), then this should assist the dollar. Likewise GDP – if above 1.5%, especially if consumer demand is decent, then dollar should get a boost. FOMC likely a non-event – Minutes though will be more interesting. See how to trade the US GDP with USD/JPY.

- GBP: Not a lot to get excited about today with credit and mortgage approvals out at 09:30.

- JPY: Â A busy agenda tonight with industrial production for December at 23:50, followed by vehicle production at 04:00 and housing starts at 05:00. Â

Idea of the Day

We are coming to the end of what has been a pretty dramatic month in FX. Volatility was at multi-year lows towards the end of last year in currency markets as a whole, but what was happening was that correlations were declining, between certain currency pairs and against other asset markets. This has continued this month with a vengeance, but markets have also become a lot more trended (sterling, yen, Swiss franc weakness, euro strength). This could make for a fairly choppy and unpredictable month end as institutional investors look to re-weight cross-currency investments, or reduce exposure to what have been profitable trades. This could make the yen and sterling at risk of some short-covering activity. But in the bigger picture, it’s shown an FX market a lot more sensitive to varying domestic conditions, something which should continue for the coming months.

Latest FX News

- USD: Gave back some of the gains of the previous day, for no good reason other than JPY and GBP short-covering and continued euro-repatriation. That said, if the economic news over coming days is on the stronger side of expectations, then we expect the dollar to make some forward progress.

- JPY: Trading the yen from the short side seems less simple in recent days, as those pre-disposed to take some money off the table jostle with those late to the game. Looking at the price action this week, there appears to be a greater equilibrium between buyers and sellers right now. That said, still plenty of potential for the yen to slide further next month, with the G20 meeting mid-month sure to stimulate discussion of currency wars.

- EUR: Breaking above the 1.35 level in early European trade and seems unstoppable right now, boosted by euro-repatriation, month-end flows, and the fact that the ECB’s balance sheet is shrinking (at least for now). Higher levels appear in prospect against most major currencies in the short term.

- GBP: January has been a shocker for sterling, but yesterday there was some short-covering and month-end flow that steadied things. Right now, it is hard to see where the good news is going to come from, given uncertainty over the UK’s relationship with Europe whilst fiscal policy is not achieving its objectives quickly enough.

Further reading: Higher US yields – Not only QE related – Could endanger Japan