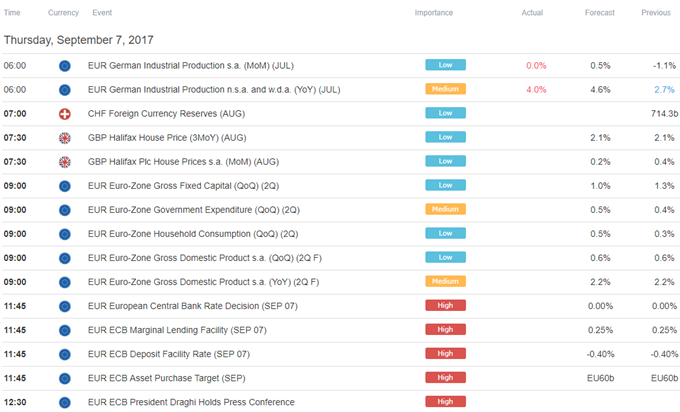

All eyes are on an ECB monetary policy announcement in European trading hours. Expectant traders are keen to see if the President Mario Draghi and company will use the occasion to begin the process of “tapering†QE asset purchases or at least set the stage for doing so in the months ahead. The absence of such guidance may be seen as disappointing, driving the Euro broadly lower.

Such a scenario seems compelling. To justify QE withdrawal, the ECB will need to make the case for upgraded inflation expectations. That will be difficult. The single currency has added nearly 7 percent since forecast were last updated in June and headline CPI has dutifully trended lower. Meanwhile, slowing composite PMI readings suggest brisk economic performance will not emerge as a potent offset.

Later in the day, speeches from Cleveland Fed President Loretta Mester and her New York counterpart Bill Dudley will enter the spotlight. Mester is a dependable hawk and seems unlikely to surprise the markets with more of the same. Dudley represents the FOMC’s centrist majority however. If he seems warm to the idea of another rate hike in 2017, the US Dollar may advance.

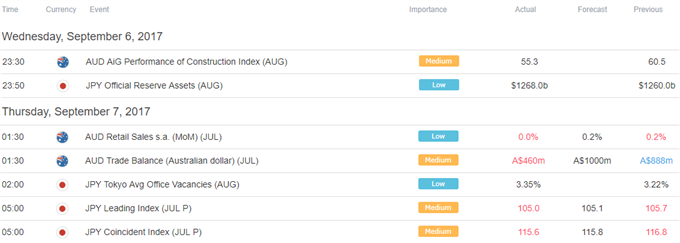

The Australian Dollar underperformed in mostly quiet Asia Pacific trade, sent lower by round of disappointing economic data releases. The New Zealand Dollar fared markedly better, correcting higher after suffering the largest drawdown in a week in the prior session. The Yen edged up as Japanese stocks drifted lower to close a gap higher at the opening bell, offering a familiar boost to the standby anti-risk currency.

Asia Session

European Session

** All times listed in GMT. See the full DailyFX economic calendar here.