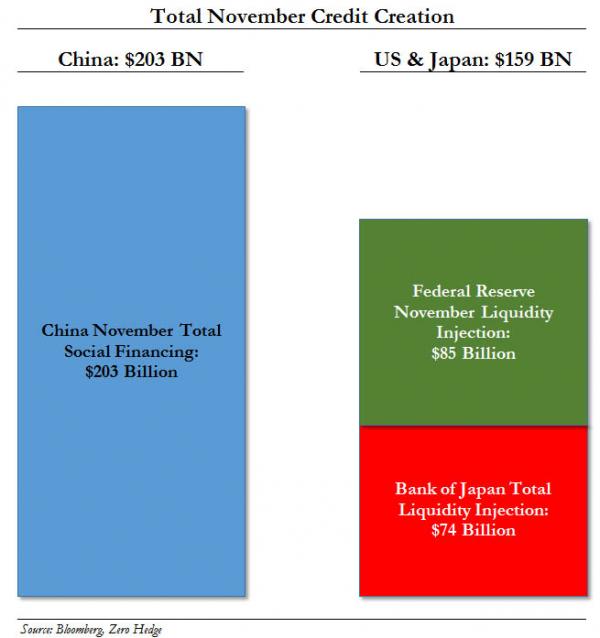

With private sector loan creation in the US and Japan virtually unchanged since Lehman levels (and the US in danger of posting a negative comp in a very months) and Europe loan creation contracting at a record pace, it falls upon the Fed and Bank of Japan (and possibly the ECB soon) to inject the much needed credit-money liquidity into the system. And, as everyone knows, month after month the Fed and the BOJ diligently create $85 billion and $75 billion in new outside money out of thin air (that this “credit” ends up in the stock market is a different topic).

So to help readers get a sense of perspective how the US and Japan compare when matched to China, below we present a chart showing the fixed monthly “money” creation by the Fed and the BOJ compared to the most comprehensive money supply aggregate available in China – the Total Social Financing – for the month of November. The chart speaks for itself.

Basically, while everyone focuses on the breakneck money creation by the Fed and the BOJ, what happened in the past month is that China quietly created some 20% more money. Perhaps most impotantly, between these three entities, nearly $400 billion in liquidity was created de novo in one month! Because when the entire world is a credit-fueled ponzi scheme, these are the kind of numbers that matter.

For those curious, here is a more detailed breakdown of the Chinese numbers from Bank of America.

New bank loans and TSF rebounded notably in November

Despite higher and volatile interbank rates and rising bond yields, credit growth remained quite robust towards year-end. Two most watched data points, new bank loans and Total Social Financing (TSF), rebounded notably to RMB625bn and RMB1230bn respectively in November from RMB506bn and RMB856bn in October. YoY bank loan growth remained unchanged at 14.2%, while yoy outstanding TSF growth moderated to 19.5% from 19.7%. Today’s money & credit data should be positive for markets which have been worried that the PBoC could tighten credit supply to reduce leverage by citing rising bond yields and interbank rates.

{kind=link}