We start with some observations on the latest developments in the global credit and rate markets (from Merrill Lynch, Citi, CS, Morgan Stanley and others).

Bank Credit

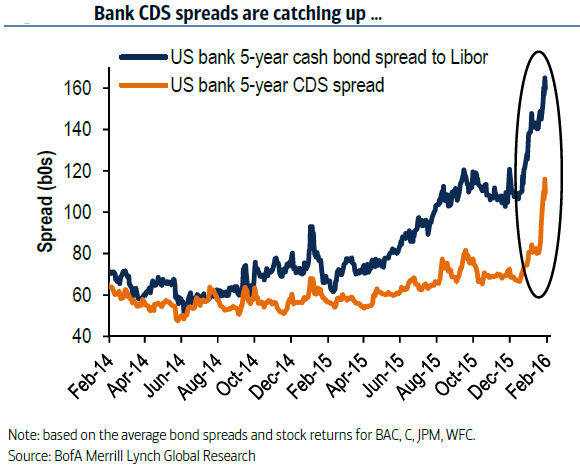

1. Bank CDS spreads are catching up with bank bond spreads which have been widening since last summer. This feels overdone – the US banking system is the healthiest it’s been in years (even as returns on equity soften).

Source: BAML

2. Related to the above, here is the share price to book ratio over time for the major US banks. The current environment is NOT 2008 or even 2011.

Source: @ForbesInvestor, h/t Jake

3. Deutsche Bank’s newest bondholders are unhappy with DB buying back its bonds at market. Apparently the latest issuance came out before the weak earnings results were made public. The bondholders are complaining that they have been misled – and now they would take a loss selling the paper back to DB.

Source: Bloomberg.com

4. European bank CDS trading volumes have surged.

Source:  â€@acemaxx, @business

5. Will the pressure on European bank shares reverse the recent improvements in Eurozone’s credit growth?Â

Source: â€@enlundmÂ

Corporate Credit

1. US investment grade bonds have outperformed high yield on a relative basis.

2. Related to the above, here we have the year-to-date fund flows for select asset classes.

Source: BAML

3. The spread between energy and non-energy corporate credits continues to rise.

Source:  â€Credit Suisse

4. US investment grade credit spreads have been highly correlated to the equity markets recently.Â

Source: Â BAML

Credit Dislocations

We’ve had a number of market dislocations recently. Spreads between corporate bonds and CDS, swaps and treasuries, CDX (index) and single-name CDS – are all sharply lower. A decade ago these dislocations would get arbitraged out, but not today.

Regulatory pressures make the arb difficult as banks conserve balance sheet usage by charging higher rates on repo financing. Moreover, single name CDS trading has become very expensive in terms of margin requirements.

Source: Â Citi Research

Citi also attributes the differences in swap spreads and bond-CDS spreads across currencies to the recent central bank activities.Â

Source: â€Citi

Rate Hike/Cut ExpectationsÂ

1. As discussed on Friday, the last few weeks saw the most dramatic shift in market expectations of the Fed policy trajectory in years (possibly the fastest on record). This chart is just spectacular.