For tactical momentum positions within the major sectors, we currently favor Technology (XLK or VGT) and Health Care (XLV or VHT) for overweight versus diversified core. Based on various combinations of focus factors, the data suggests these sectors:

- High growth of earnings and interest rates now: XLY, XLI, XLB, XLF

- Reduced growth of earnings and rising interest rates in 2019: maybe XLV, XLE and XLC

- Blended Cyclical and Defensive suitability: XLK, XLE, XLC

- Minimal to positive correlation to rising interest rates: XLF, XLE, XLI, XLB, XLY

- Lower earnings growth at lower cost of growth: XLF, maybe XLB

- Higher earnings growth and lower cost of growth: XLC, XLE, XLY

- Higher 3-5-year earnings growth: XLY, XLC, XLE

- Higher growth in 2019 than 2018: None

- Higher 3-5-year earnings growth than 2018: XLRE, XLY

- Higher 3-5-year earnings growth than 2019: All excluding XLE

- Currently positive 1-year trend momentum: XLY, XLK

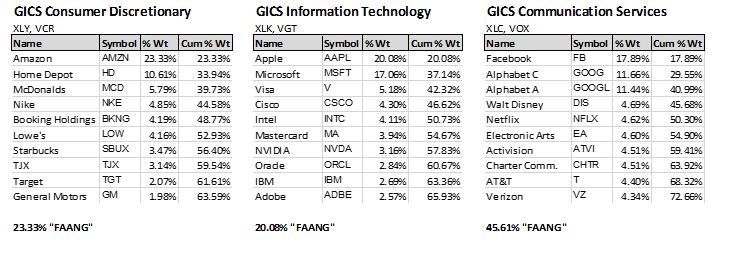

The three sectors newly constituted as of September 28 are shown here represented by their top 10 holdings. The movements out of Consumer Discretionary and Technology into Communications Services, create difficult challenges in effectively comparing current data to historical averages.

Backtest data provided by State Street Global Advisors shows these historical differences between the old and new sector definitions. We are at somewhat of disadvantage attempting to compare current to historical valuation and other data due to the reconfiguration.

For those of you focused on “FAANG†(FaceBook, Apple, Amazon, Netflix and Google), whether to overweight or underweight, the percentage of FAANG exposure in each of the new sector funds is listed below their top 10 holdings in the tables above.

Within long-term strategic holdings, you can maximize FAANG exposure by owning a short list of mega-cap stocks in a fund such as XLG (Russell top 50) with 25.44% FAANG, minimize with VTI (total US market) with 10.51% FAANG; or marginalize FAANG with RSP (S&P 500 equal weight) with 1%.

2-Yr Correlation to Treasury Yields vs 10-Yr Beta To S&P 500Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â