Nasdaq Takes a Hit, Rotation Into ‘Safe’ Sectors Continues

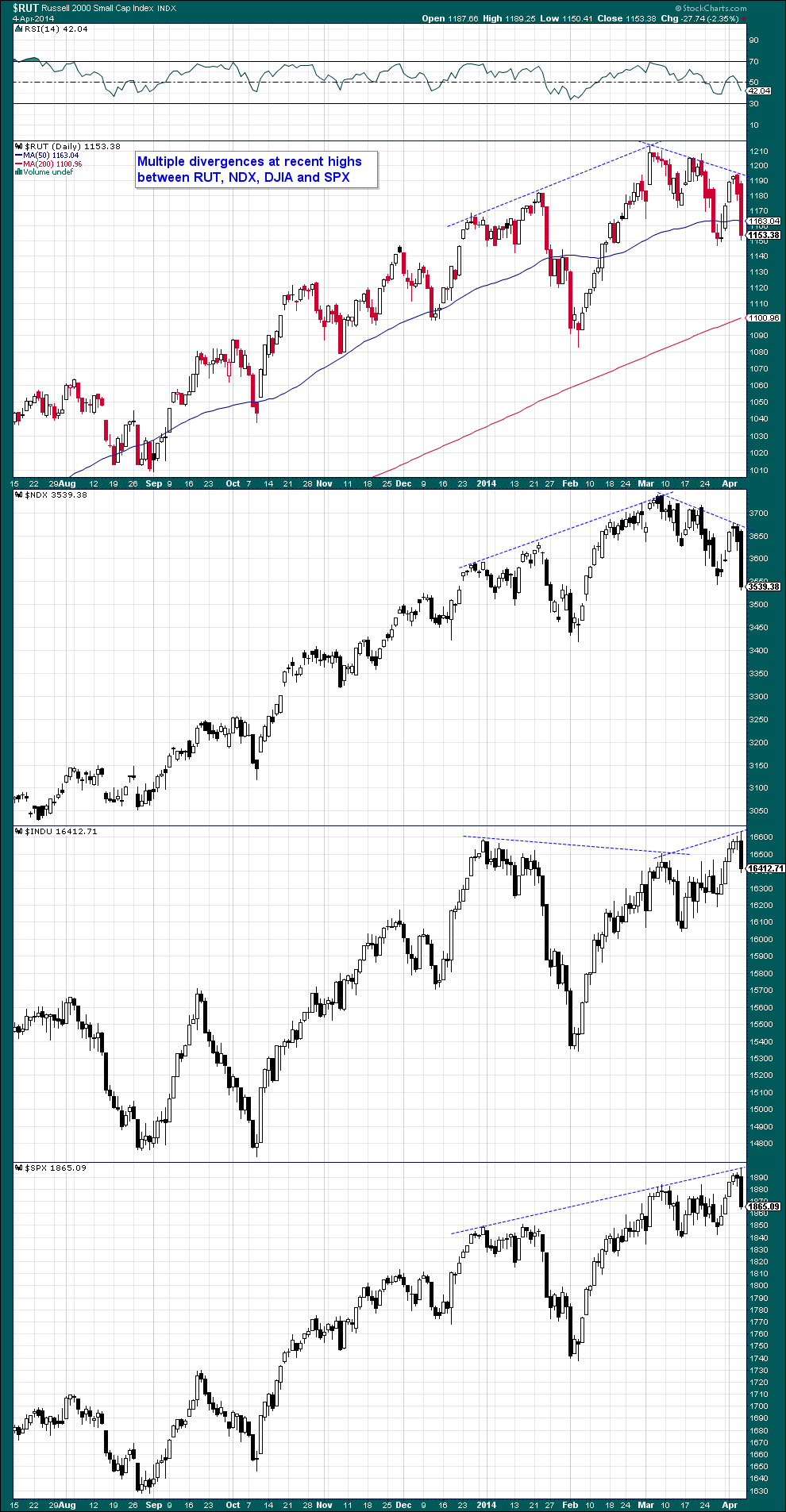

On Friday momentum stocks sold off with some verve again after the release of the payrolls data. Since the latter were actually quite close to the expected number, they cannot really have been the trigger of the sell-off (in other words, it would probably have happened regardless of the data). A few weeks ago, Charles Biederman of TrimTabs warned that the upcoming tax season could lead to some selling, but there is also the presidential cycle to consider. If the market continues to follow this particular cycle model (it has actually done so year-to-date), it should decline from an April high into an October low. What makes the recent market action interesting is that there continue to be multiple divergences in evidence between different indexes:

Russell 2000 Index, NDX, DJIA and SPX – the former two have been in sync, but have diverged from the other indexes. There are many more intra-market divergences between different sub-sectors that have been put in place over recent months.

Two examples illustrating the weakness in momentum names are PNQI (internet power shares) and BBH (a cap-weighted biotechnology ETF). These two were previously among the strongest sectors.

PNQI is closing in on its 200 dma – click to enlarge.

BBH is likewise about to meet with its 200 dma – click to enlarge.

There has been rotation from stocks perceived as risky into stocks perceived as ‘safe’, such as utilities and tobacco stocks. The ratio of XLU to QQQ has been rising strongly since making a low in mid January. In other words, there have been signs of intra-market deterioration since January already, but since early March they have become a lot more pronounced. This happens to coincide with the beginning of the Fed’s ‘tapering’ of QE3, which may or may not be coincidence.

Utilities rise strongly vs. QQQ (an ETF replicating the performance of the NDX) – click to enlarge.

There is some empirical evidence that supports the idea that there may be a connection between this change in market character and the decrease in monetary pumping (small as it is). Previous pauses in the Fed’s extraordinary policy measures have been followed by fairly sizable corrections on both occasions, and the market only regained its poise once new measures were either announced or implemented (QE2 was preceded by an ‘announcement effect’).