Image Source:

Image Source:

The results of the US presidential election indicate that Trump will emerge victorious and the Republican Party will maintain control of the Senate. The New York Times’ closely-watched ‘swingometer’ projected a 93% chance of Trump winning, while Treasury yields rose to four-month highs as some betting sites significantly favoured him. However, the House of Representatives is still too close to call. Four years after departing the White House, Trump has advanced to the brink of a remarkable political revival by defeating Democrat Kamala Harris in the battleground states of North Carolina, Georgia & Pennsylvania. The euro, yen, and antipodean currencies have experienced declines as a result of the 1.5% increase in the US dollar index, which is the largest increase since March 2020. The dollar’s sharp increase against the offshore yuan prompted reports that Chinese banks were selling dollars to slow the yuan’s decline. China is perceived as being at the forefront of tariff risk, and its currency is currently trading at a high level of uncertainty, with implied volatility against the dollar circling record highs. As investors anticipate a meeting of top policymakers in Beijing this week to sanction local government debt refinancing and spending, Chinese markets have declined from an almost one-month high.European stock futures were less ebullient due to the potential for a global trade war and the threat to EU exports if Trump’s tariff policies are implemented. Additionally, there was a possibility that Trump could disengage from NATO, which would necessitate an increase in defence expenditures in Europe and would also serve to strengthen Russia’s territorial ambitions. Aside from US political developments, macro events that could potentially impact markets on Wednesday include: Services within the Eurozone Producer prices for September and PMIs for October. September industrial orders in Germany. Services provided by the United States PMI for October.

Overnight Newswire Updates of Note

Trump Wins The Critical Battleground State Of Pennsylvania

PBoC Affirms Supportive Monetary Policy

Japan PM Ishiba Preps Meeting With Biden, China’s XI

Japan PMI, Confidence Shrinks On Softer Sales

UBS Pushes Back RBA First Rate Cut Forecast To May 2025

NZ Unemployment Rate Rises Less Than Forecast

Hong Kong Stocks Slide, Traders Pare Risky Bets

US Stock, Yields Rise As Markets Await Election Outcome

Nvidia Rides AI Wave Past Apple As World largest Company

Crypto Surge To Record Levels On Early Trump Lead

Spike In UK Borrowing Cost Wipes Out Fiscal Headroom

(Sourced from reliable financial news outlets)

FX Options Expiries For 10am New York Cut (1BLN+ represents larger expiries, more magnetic when trading within daily ATR)

EUR/USD: 1.0650 (3.9BLN), 1.0700 (686M), 1.0725 (1.5BLN)

1.0750 (900M) 1.0800 (2.4BLN)

USD/CHF: 0.8675 (241M), 0.8700 (1.4BLN), 0.8800 (289M)

EUR/GBP: 0.8390-0.8400 (621M)

GBP/USD: 1.3000 (331M)

AUD/USD: 0.6475 (689M), 0.6510 (728M), 0.6525 (817M)

AUD/NZD: 1.1010 (397M), 1.1100 (300M)

USD/CAD: 1.3800 (555M), 1.3875 (420M), 1.4025 (267M), 1.4050 (442M)

USD/JPY: 153.50 (728M), 155.65 (350M)

CFTC Data As Of 1/11/24

Net USD G10 long +$8.88bn to +$18.7bn in Oct 23-29 IMM period; $IDX +0.13%

EUR +0.17%: speculative positions decreased by 21.8k contracts, now at -50.3k, lower ECB view weighs on EUR

JPY +1.55%; speculative positions decreased by 37.6k contracts, now at +25k, on hawkish Fed, less dovish BoJ

GBP +0.27%; speculative positions decreased by 8.2k contracts, now at +66.4k; less-dovish BoE lends support. Note large sterling dip post-budget not accounted for in this report

CAD +0.62%; speculative positions decreased by 26.9k contracts, now at -168k; shorts eyes July ATH -196k

AUD -1.78%; speculative positions decreased by 163 contracts, now at +27.5k; for now RBA least dovish c.bank

Equity fund managers cut S&P 500 CME net long position by 20,435 contracts to 1,045,389

Equity fund speculators trim S&P 500 CME net short position by 12,576 contracts to 292,035

Speculators increase CBOT US 10-year Treasury futures net short position by 52,992 contracts to 901,183

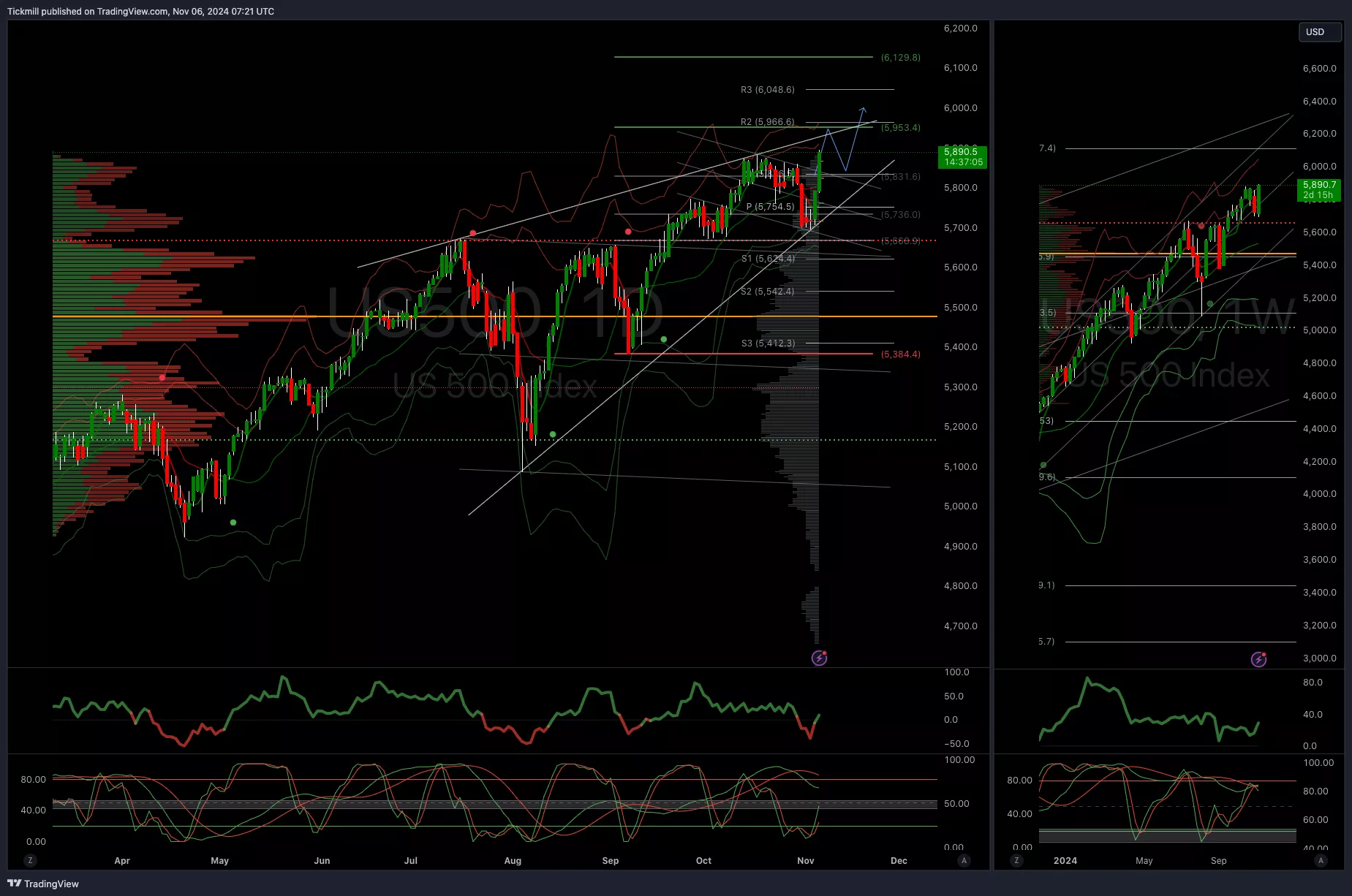

Technical & Trade ViewsSP500 Bullish Above Bearish Below 5745

Daily VWAP bearish

Weekly VWAP bearish

Below 5720 opens 5660

Primary support 5660

Primary objective 5950

(Click on image to enlarge) EURUSD Bullish Above Bearish Below 1.09

EURUSD Bullish Above Bearish Below 1.09

Daily VWAP bEARISH

Weekly VWAP bearish

Above 1.09 opens 1.0980

Primary support 1.0750

Primary objective 1.0750 – TARGET HIT NEW PATTERN EMERGING

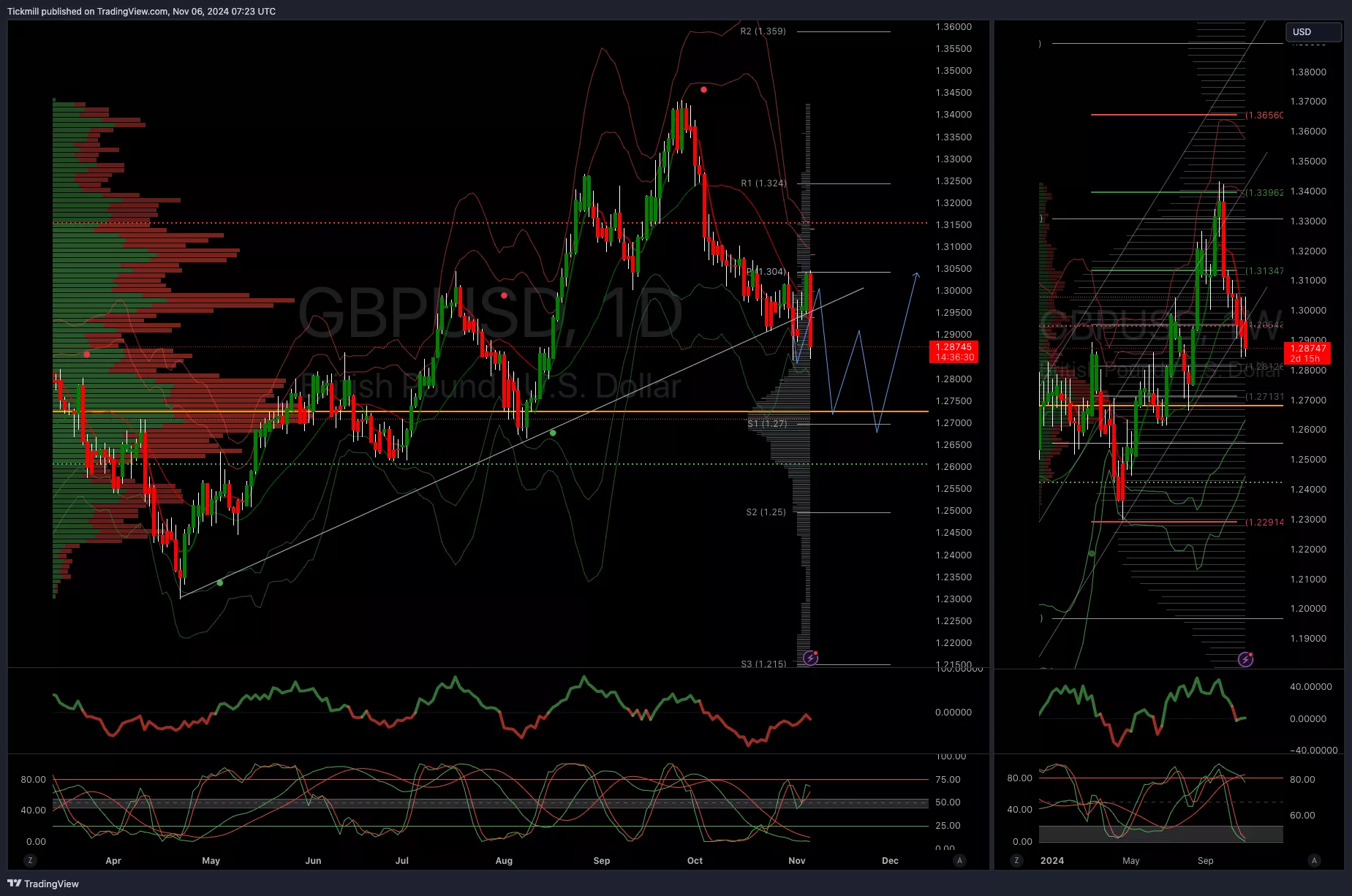

(Click on image to enlarge) GBPUSD Bullish Above Bearish Below 1.3050

GBPUSD Bullish Above Bearish Below 1.3050

Daily VWAP bEARISH

Weekly VWAP bearish

Below 1.29 opens 1.27

Primary support is 1.29

Primary objective 1.31

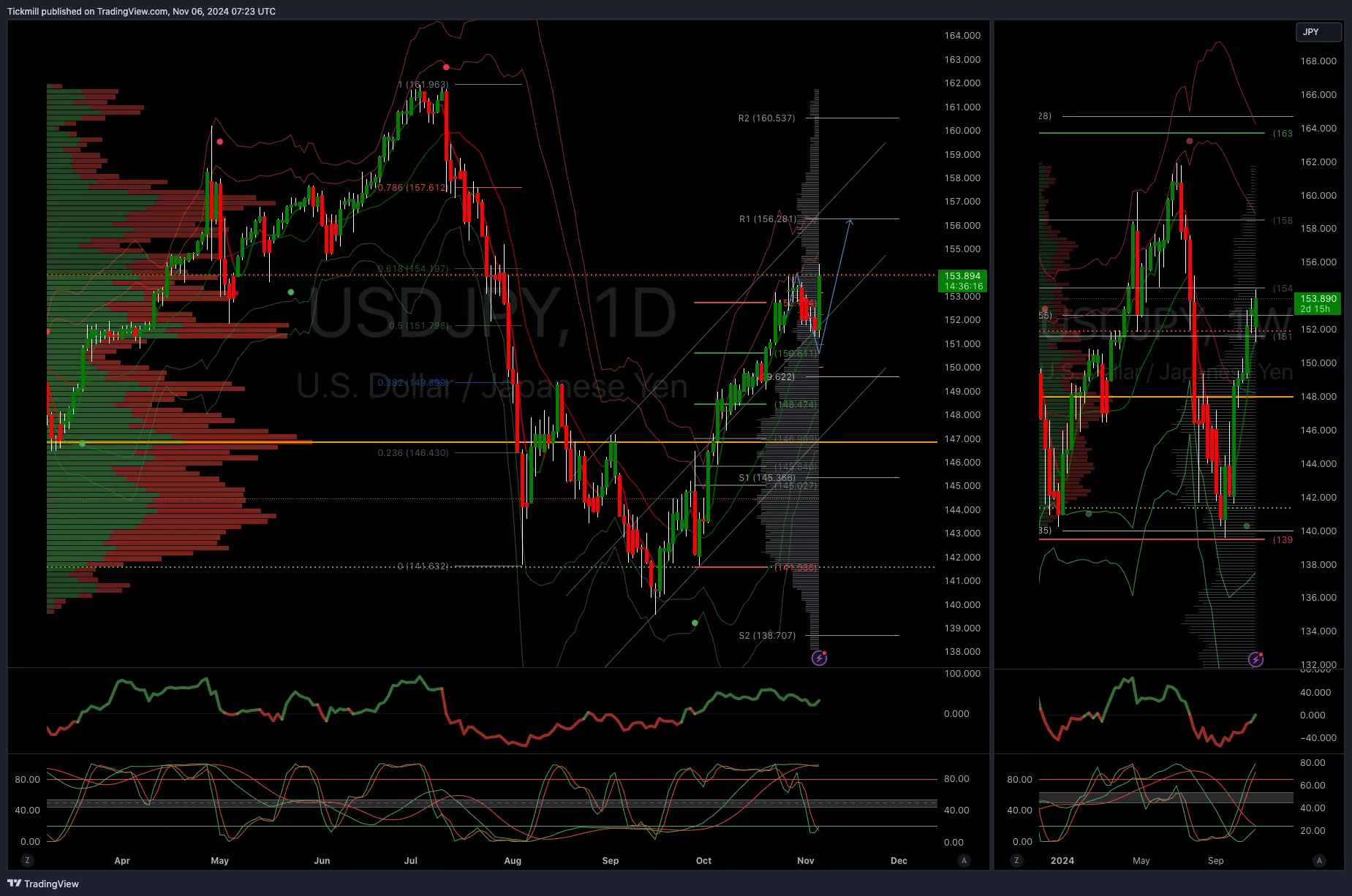

(Click on image to enlarge) USDJPY Bullish Above Bearish Below 148

USDJPY Bullish Above Bearish Below 148

Daily VWAP bullish

Weekly VWAP bullish

Below 148 opens 144

Primary support 148

Primary objective is 156

(Click on image to enlarge) XAUUSD Bullish Above Bearish Below 2680

XAUUSD Bullish Above Bearish Below 2680

Daily VWAP bearish

Weekly VWAP bullish

Below 2670 opens 2600

Primary support 2550

Primary objective is 2800

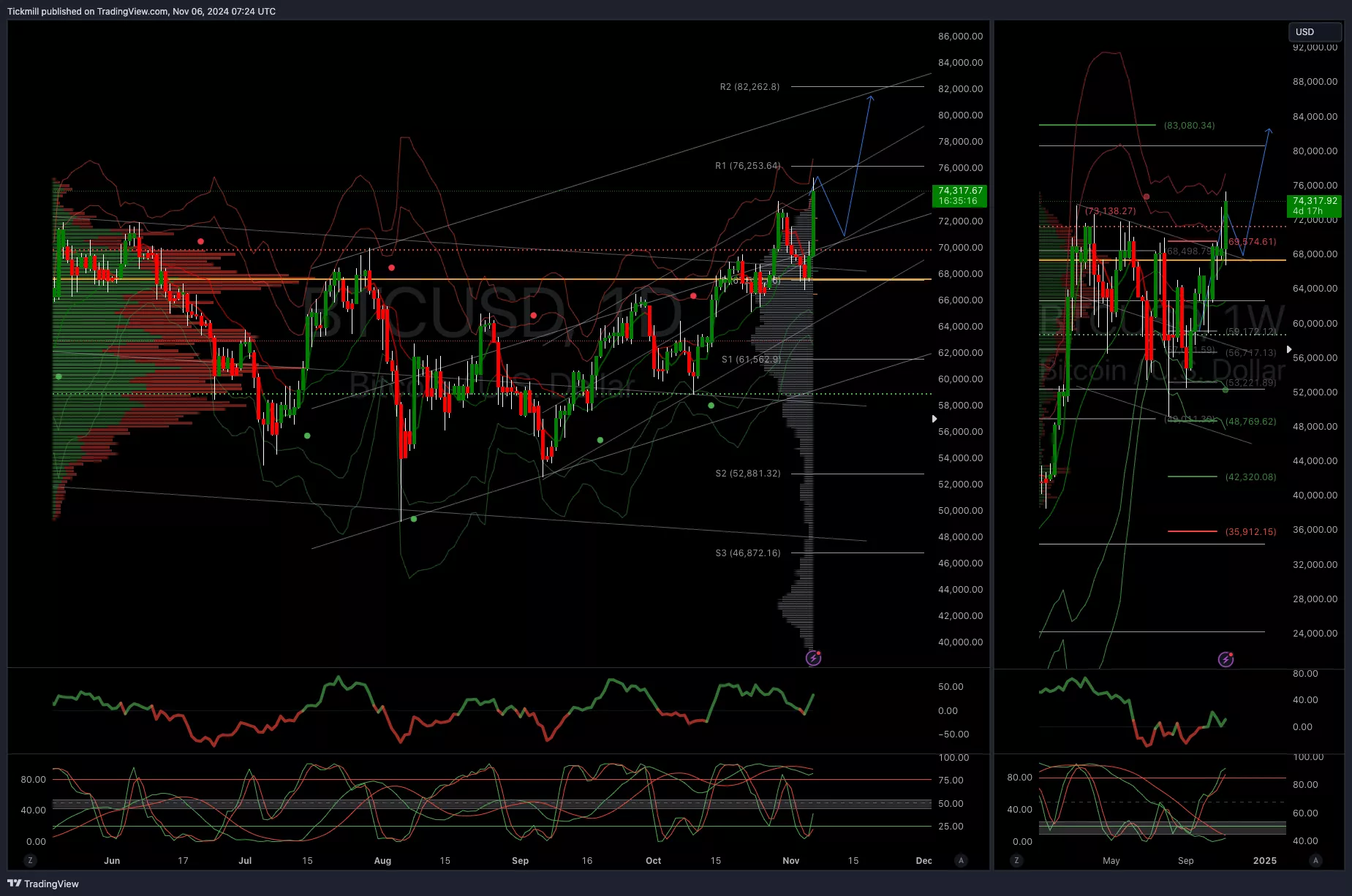

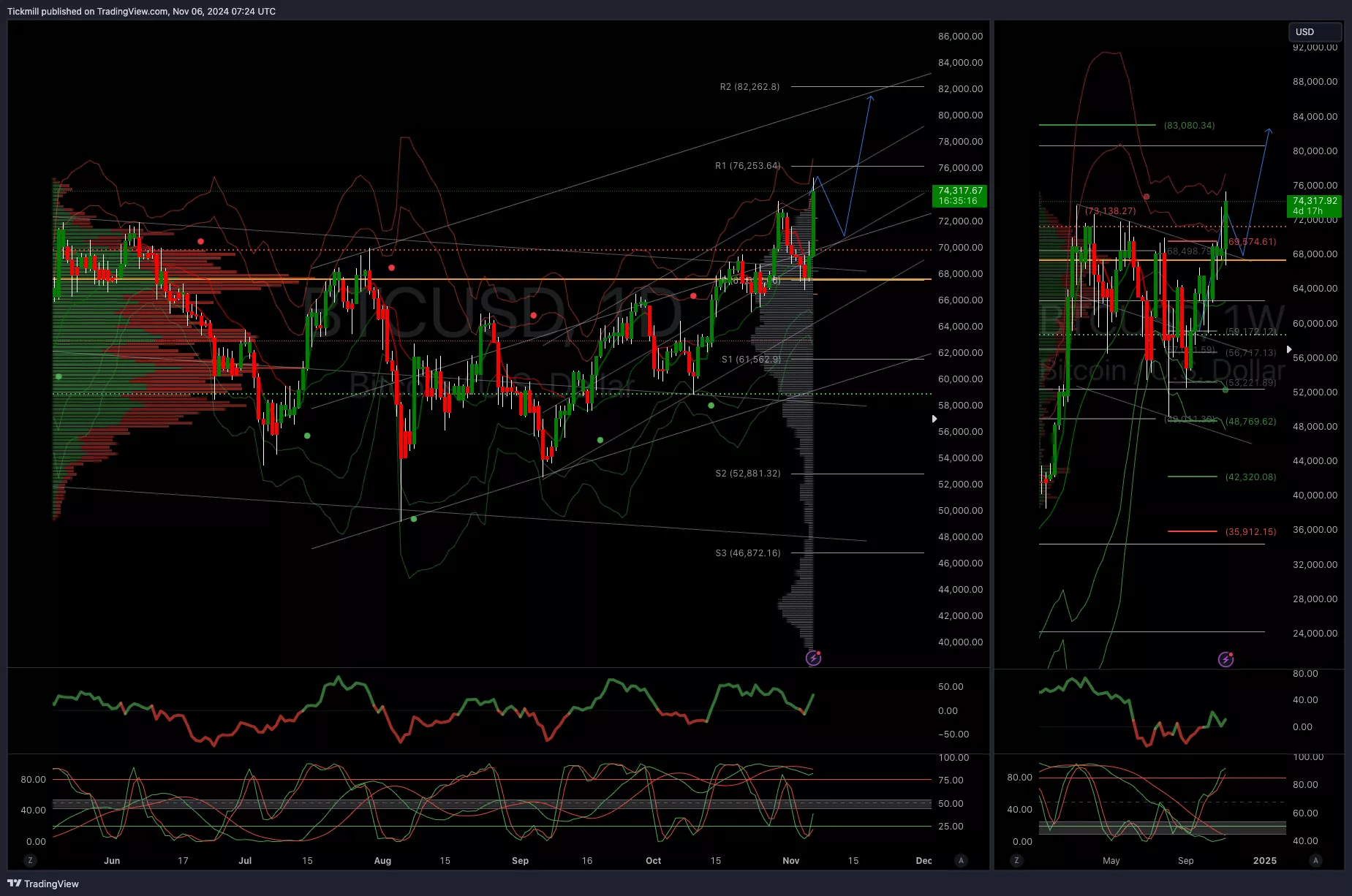

(Click on image to enlarge) BTCUSD Bullish Above Bearish Below 69500

BTCUSD Bullish Above Bearish Below 69500

Daily VWAP bullish

Weekly VWAP bullish

Below 69000 opens 64000

Primary support is 58000

Primary objective is 80000

(Click on image to enlarge) More By This Author:

More By This Author: