Asian stock markets are trading mostly higher on Thursday, buoyed by the positive sentiment from Wall Street’s performance overnight, as markets remain optimistic about the interest rate outlook following the release of the latest US inflation data. Based on the recent economic data, CME Group’s FedWatch tool is indicating a 94.2% chance the US Fed will lower interest rates by a quarter point next month. On the earnings front, TSMC’s net income for the third quarter surpassed the average analyst forecast. The report alleviated concerns over the semiconductor industry after ASML’s underwhelming order figures and reduced revenue projection for 2025 earlier this week, leading to support for the flagship chip sector.The Japanese market is experiencing further losses on Thursday, despite the positive signals from Wall Street. The Nikkei 225 is dropping below the 39,000 handle with declines in exporters and technology stocks partially offset by gains in automakers and financial stocks. Traders have also responded to domestic data showing Japan recording a trade deficit in September, as exports unexpectedly declined while import growth slowed.China’s CSI300 real estate index declined by 5%, erasing two days of gains. China’s housing minister pledged to improve builders’ access to funding to complete thousands of projects, and the central bank’s deputy governor stated that cuts to down payments had already boosted confidence and sales. However, there was no new initiative to excite markets about a meaningful revival in a sector where a crackdown on developers’ borrowing has triggered a wave of defaults, while declining prices have shaken households’ faith in the asset class. Property developer Sunac China, taking the recent rally as a cue to raise capital, contributed to dampening the mood. Hong Kong-listed mainland developers fell by 3%. Some investors took the opportunity to cash in on the good news, leading to a pullback.Even though President Lagarde has taken a balanced stance, market pricing now assigns a likelihood of over 90% for Thursday’s policy rate decrease of another quarter point. Data on Eurozone business has been dismal, especially in manufacturing, with indications that the slowdown is affecting services as well. This increases the dangers associated with the employment market’s tightness. Inflation statistics have also improved, with HICP in Germany, France, Italy, and Spain falling below 2%. Although disinflation in services is still obstinate, weak demand, softening wage pressures, and the headline rate’s ongoing slowdown will all continue to push down underlying prices. In the’medium-term’ timeframe, inflation should return to goal in a sustainable manner, according to the Council. Risks of negative growth should be more worrisome than any lingering consequences of the earlier inflation shock since the policy operates with a lag. Since the policy is excessively restricted, it is difficult to argue for more “wait and see.” Overnight Newswire Updates of Note

(Sourced from reliable financial news outlets)As the US elections draw near, the financial markets are bracing for potential volatility, presenting both opportunities and challenges for traders. To help navigate this crucial period, we have launched the a comprehensive resource tailored to meet the needs of traders at every level.

FX Options Expiries For 10am New York Cut (1BLN+ represents larger expiries, more magnetic when trading within daily ATR)

CFTC Data As Of 11/10/24

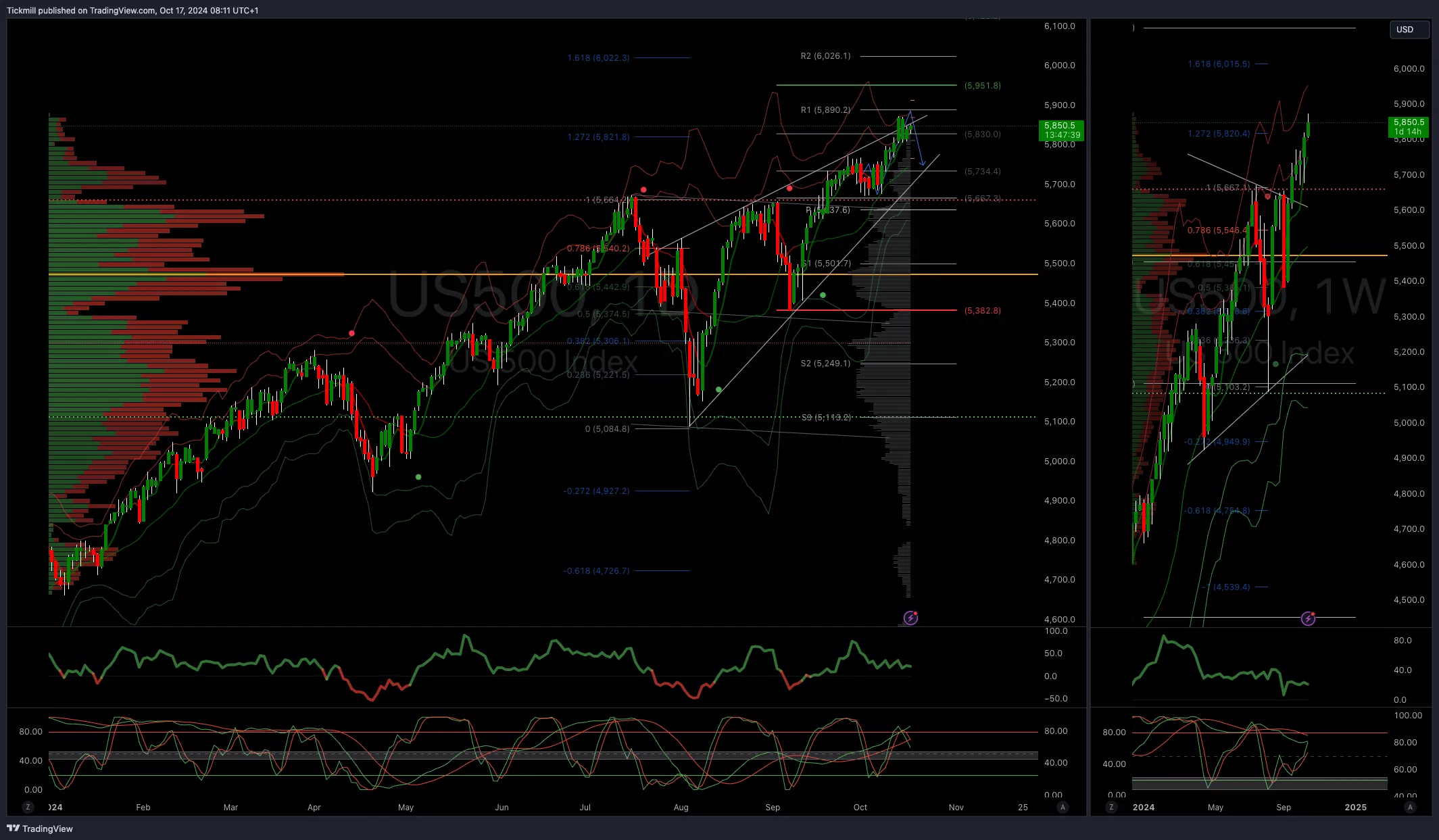

Technical & Trade ViewsSP500 Bullish Above Bearish Below 5750

(Click on image to enlarge) EURUSD Bullish Above Bearish Below 1.11

EURUSD Bullish Above Bearish Below 1.11

(Click on image to enlarge) GBPUSD Bullish Above Bearish Below 1.3230

GBPUSD Bullish Above Bearish Below 1.3230

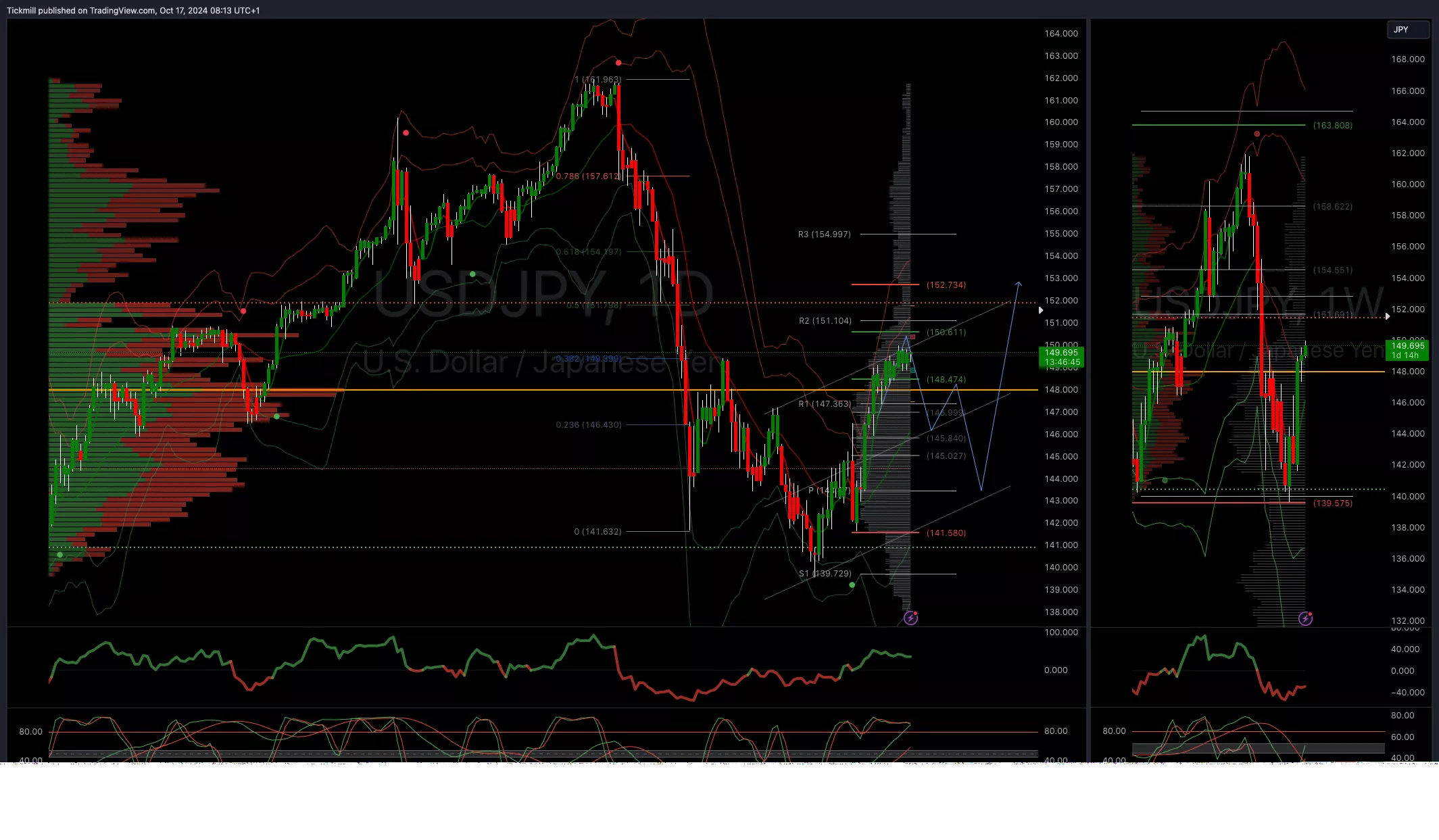

(Click on image to enlarge) USDJPY Bullish Above Bearish Below 144

USDJPY Bullish Above Bearish Below 144

(Click on image to enlarge) XAUUSD Bullish Above Bearish Below 2645

XAUUSD Bullish Above Bearish Below 2645

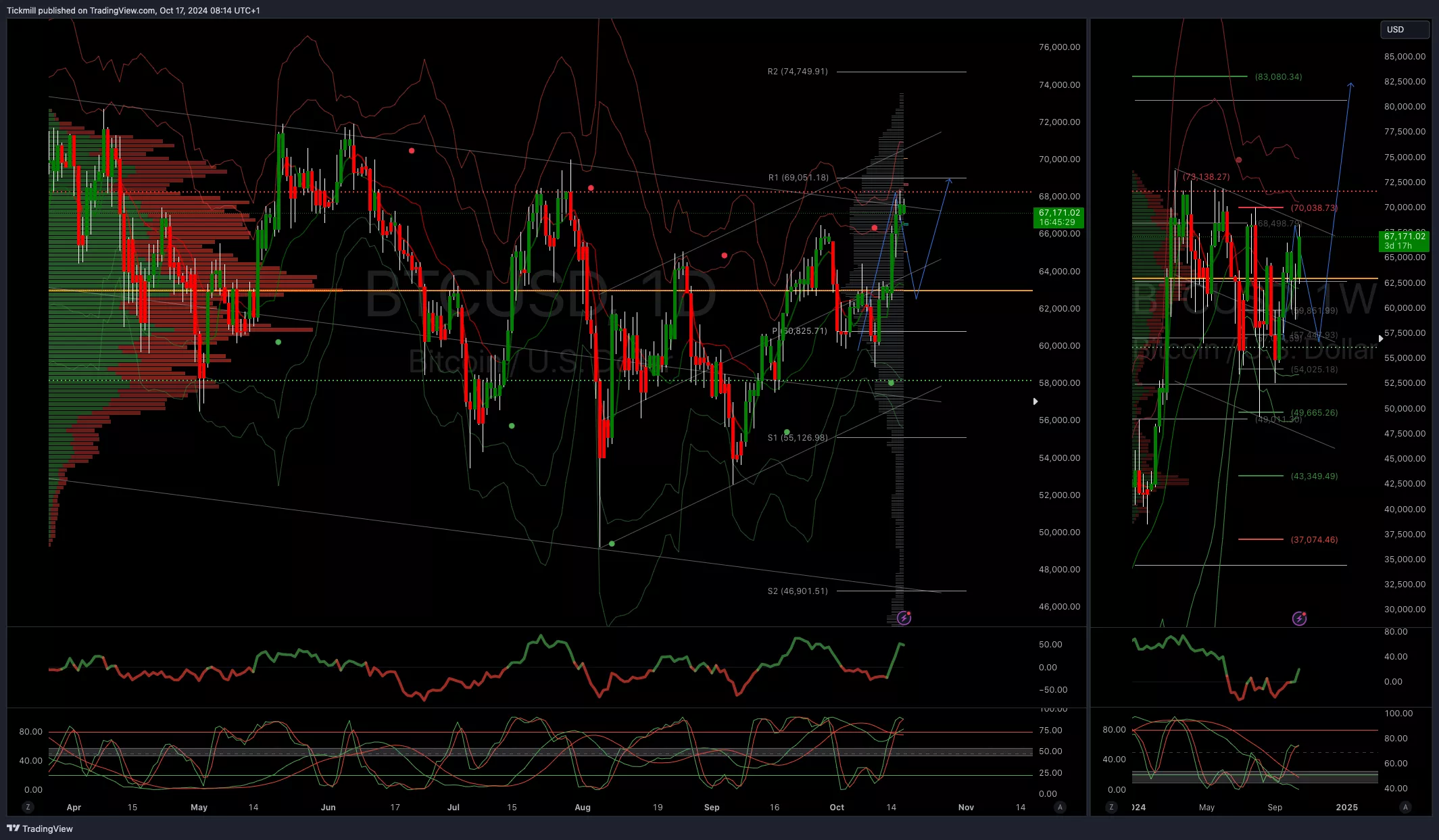

(Click on image to enlarge) BTCUSD Bullish Above Bearish Below 57000

BTCUSD Bullish Above Bearish Below 57000

(Click on image to enlarge) More By This Author:

More By This Author: