Asian equities markets saw mixed results Thursday as investors weighed the potential effects of a second Donald Trump presidency. They also eye the U.S. Federal Reserve and other major central banks’ monetary policy decisions due today. All three major U.S. share indexes surged to record highs, but Asia did not experience significant increases, despite the possibility of a Republican sweep that would swiftly bring in significant fiscal expenditure. On the fear of larger deficits, U.S. Treasury rates surged, which helped push the dollar to its largest one-day gain in almost two years against key peers on Wednesday. German Chancellor Olaf Scholz’s dismissal of Finance Minister Christian Lindner, which led to the dissolution of the government three-party coalition, further put pressure on the euro. The Japanese stock market has retreated from its recent gains, closing lower on Thursday despite the positive signals from Wall Street overnight. The Nikkei 225 saw declines in major index constituents and technology stocks only partially offset by advances in exporting and financial firms. Chinese markets rebounded in the overnight session after losing ground on Wednesday due to the likelihood of higher tariffs under another Trump presidency. Hong Kong’s Hang Seng rose 2% and mainland blue chips added 4%. China’s week-long National People’s Congress Standing Committee meeting concludes on Friday, and market participants anticipate fresh details on stimulus measures. Chinese trade data released Thursday showed outbound shipments grew at the fastest pace in over two years in October as manufacturers rushed inventory to major export markets in anticipation of further tariffs from the U.S. and the European Union.BoE Governor Bailey and the MPC will have to take a tough line to out-hawk the market. A 25bp cut in Bank Rate to 4.75% today by the BoE is widely expected but there is probably less consensus on the vote split and especially on the outlook that will be signalled from here. A CPI forecast of around 2% at the 2-year horizon seems likely. The MPC minutes and Bailey’s press conference may signal a more hawkish message, but surely the market has got its retaliation in first on this occasion. With services CPI and private sector average earnings tracking beneath August MPR projections, the risk is that the market has more than factored in the Budget’s fiscal stimulus.The 2024 US election resulted in a convincing victory for Trump, who returned to power with a radical manifesto. Republicans retained control of the House and regained the Senate, giving Trump an overwhelming mandate to deliver on his campaign promises and removing many checks that Democrat control could have imposed. Trump’s protectionist ideology and transactional approach will be problematic for surplus economies, generating uncertainties around inflation and disrupting supply chains. Geopolitically, a more isolationist US leadership coincides with conflict and pariah-state expansionism, raising risks but also reinforcing the positive US dollar trend. The Federal Reserve is likely to cut interest rates by 25 basis points, with Powell emphasising the economy’s soft-landing credentials. The Fed will continue easing policy as inflationary pressures subside and the labour market remains balanced, with growth around 2.5%. The Fed will maintain its current tone, reacting to data and events rather than presumptions about the incoming administration.

Overnight Newswire Updates of Note

(Sourced from reliable financial news outlets)

FX Options Expiries For 10am New York Cut (1BLN+ represents larger expiries, more magnetic when trading within daily ATR)

CFTC Data As Of 1/11/24

Technical & Trade ViewsSP500 Bullish Above Bearish Below 5850

(Click on image to enlarge) EURUSD Bullish Above Bearish Below 1.09

EURUSD Bullish Above Bearish Below 1.09

(Click on image to enlarge) GBPUSD Bullish Above Bearish Below 1.3050

GBPUSD Bullish Above Bearish Below 1.3050

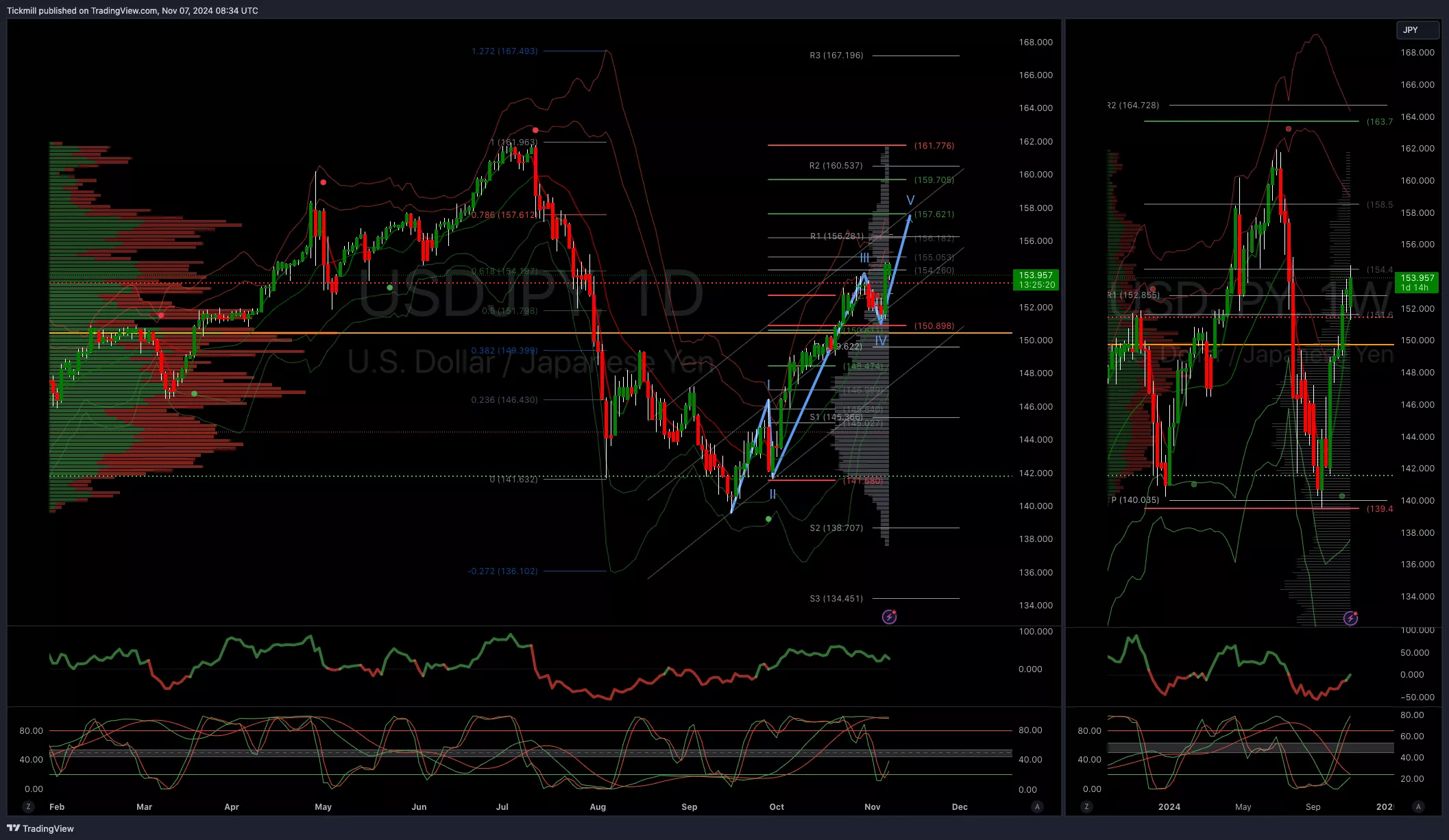

(Click on image to enlarge) USDJPY Bullish Above Bearish Below 151

USDJPY Bullish Above Bearish Below 151

(Click on image to enlarge) XAUUSD Bullish Above Bearish Below 2680

XAUUSD Bullish Above Bearish Below 2680

(Click on image to enlarge) BTCUSD Bullish Above Bearish Below 71500

BTCUSD Bullish Above Bearish Below 71500

(Click on image to enlarge) More By This Author:

More By This Author: