By Rupert Hargreaves

At the end of last week, Credit Suisse published a research report on its 18 contrarian stock ideas. What’s special about this report is that it highlights the companies where Credit Suisse’s analysts hold a view that goes against the consensus.  What’s more, the companies have been selected as the bank’s analysis reveals opportunities that the market has not yet priced in.

In order to arrive at the list of 18 contrarian stock ideas, analysts screened the bank’s whole US coverage universe to identify companies where Credit Suisse’s analysts’ views diverged from that of the rest of Wall Street, focusing on both rating as well as earnings projections. To Whittle down the pack further, analysts only put forward picks and selected stories in which their conviction level was high.

The result is a list of 12 Outperform-rated contrarian stock ideas and 6 Underperform-rated contrarian stock ideas. Here are five of the top picks. The summary is intended to be a starting point for further analysis by investors themselves.

Contrarian stock ideas

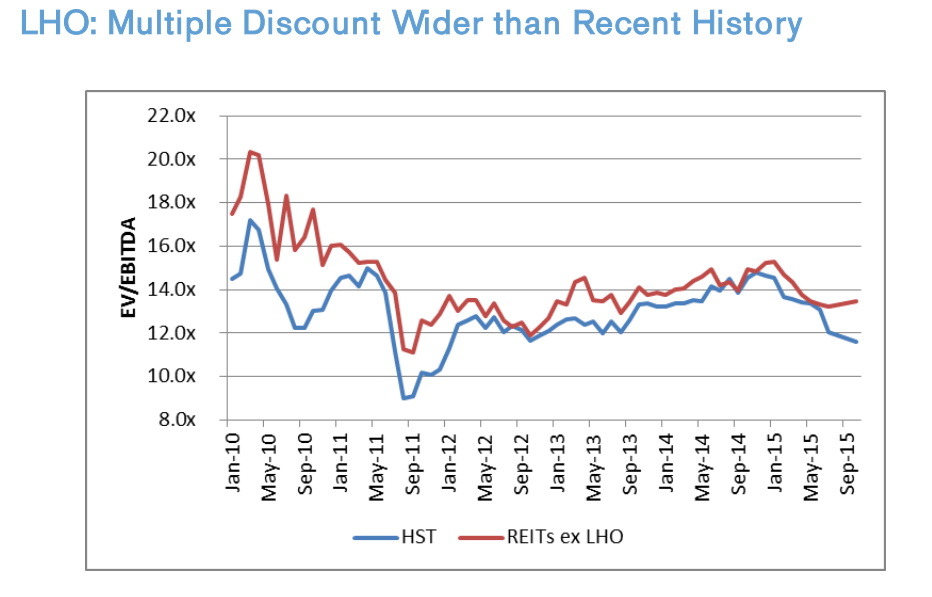

First up is LaSalle Hotel (LHO). Credit Suisse like LaSalle as the stock is currently trading 40% below the bank’s $39 price target. This target is based on a 50% weighting of its $42/share forward NAV, a 30% weighting of a $38/share EV/EBITDA valuation, and a 20% weighting of a $37/share DCF estimate. LaSalle has become a victim of the indiscriminate lodging selloff, giving investors a rare opportunity to buy blue chip lodging REITs at a significant discount to intrinsic value. LaSalle has significant exposure to west coast markets (37.3% of total exposure) where RevPAR growth is most robust. 15% of LaSalle’s portfolio is located in DC, a market that is expected to stage a recovery during 2016 and 2017.

Contrarian Stock Ideas: LaSalle’s discount to the wider sector

Next up is Weatherford International (WFT). Weatherford shocked investors last month when it attempted, and failed, to raise $1 billion in equity with the goal of making a once-in-a-lifetime strategic acquisition. The stock was punished, losing approximately $1.3 billion in market cap in one day. However, aside from this bad judgment call by management, the underlying business continues to show progress. The new management team continues to implement and push metrics on support ratios. Additionally, the financial statements are finally cleaned up: asset impairments and reductions in manufacturing and facility locations have been made. Weatherford expects to generate $150 million to $200 million in free cash flow for 2015 — a rare occurrence for the company. Weatherford has not generated a positive full-year free cash flow for ten years. Credit Suisse has a $13 price target on the stock based on an 11.5x (historical peak) multiple on 2016 EBITDA and a historical 25th percentile P/CF multiple of 8.7x.