Image source:

Image source:

The University of Michigan Consumer Survey for November found a fresh low in spending intentions. Consumers citing interest rates as preventing them from buying an automobile (36%) and a home (67%) were the highest since the 1981 and 1982 recessions when the Fed funds rate was 12 and 10 percent, respectively, versus 5.5 percent today. Meanwhile, it is more too-high prices than interest rates that are the biggest impediment to affordability today. The good news is that anemic demand is pressuring prices lower.For retail sales, the all-important holiday shopping season will likely disappoint elevated earnings expectations. See :

Early signs—from the number of boxes loaded on railway cars to rising consumer debt—signal a weaker holiday season than the past three, when pent-up demand coming out of the worst of the pandemic sparked shoppers’ spending.

A dud of a holiday season would be disastrous for retailers. For economists, it would be an ominous signal about the direction of the economy. And for shoppers, forecasting offers a clue to when and how deeply stores will start slashing prices. (Hint: There could be some steep discounting this year)…

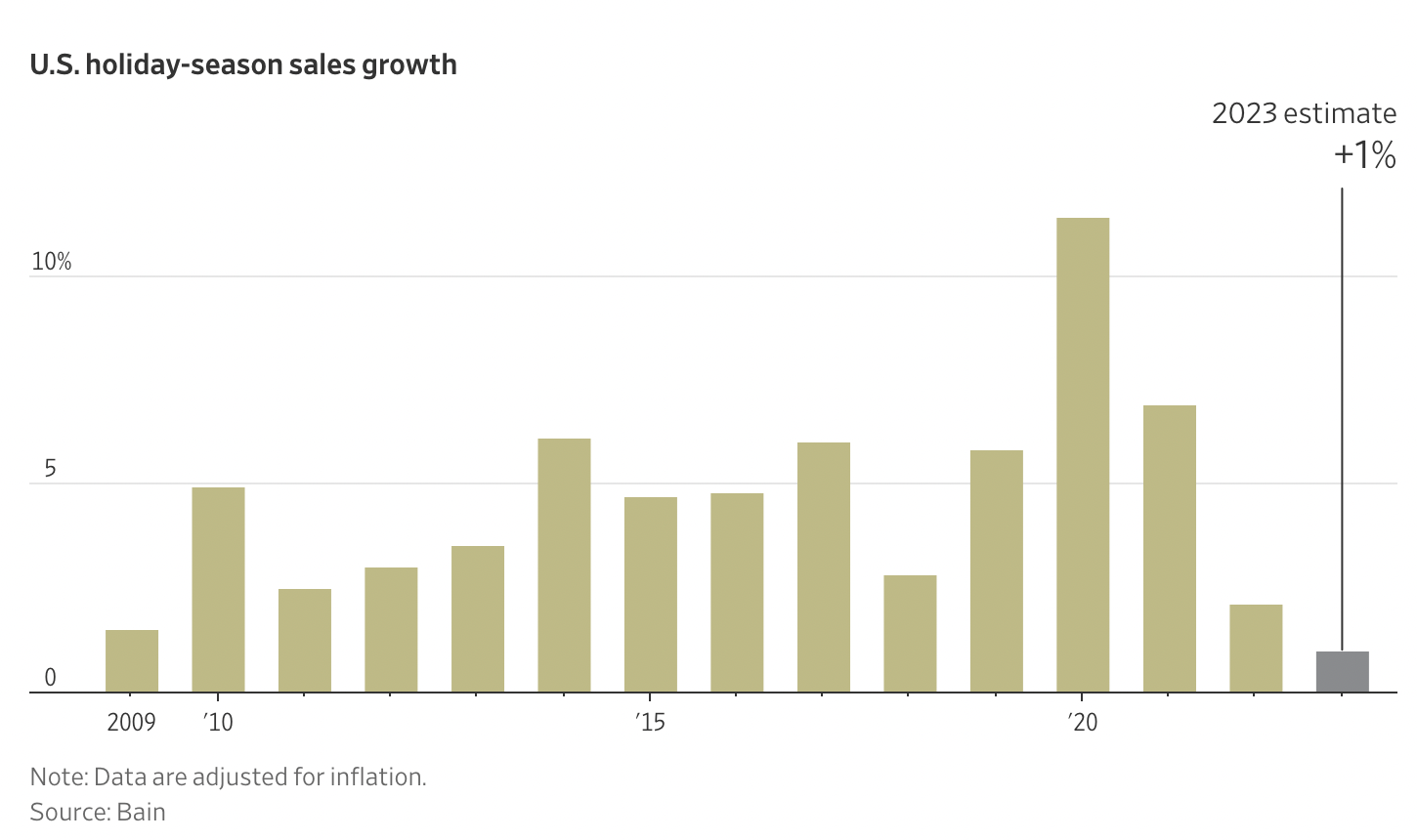

The National Retail Federation expects overall sales increases could be in line with the slower pace we saw in the decade leading up to the pandemic, from 2010 to 2019, when the average annual increase over that period was 3.6%. It expects November-December spending, not including inflation, to rise 3% to 4%. By contrast, sales rose 5.4% in 2022, 12.7% in 2021 and 9.1% in 2020.

Others are even gloomier. Some economic and company forecasts call for almost no growth in holiday spending this year, particularly when inflation is stripped out. The consulting firm Bain expects inflation-adjusted retail sales in November and December for stores and e-commerce to rise 1%, the slowest pace since the financial-crisis holidays of 2008.

Also, see :

Canadian companies are painting a stark picture of a consumer who’s pulling back on spending, as rising debt payments and inflation force households to change their behavior.

From big-box retailers to toy marketers to coat manufacturers, recent corporate earnings results and executives’ comments underscore how quickly the economic temperature is changing after two years of robust growth.

Again, the good news is that weak demand and mounting supply will continue to lower prices until clearing points are found. A deluge of exports from places like China is exerting a deflationary impact globally–typical during recessions. See :

Prices of goods shipped from China have fallen around 20% this year, according to ABN AMRO. While some of that drop reflects easing supply-chain bottlenecks, it is also a sign that Chinese sellers are discounting to preserve or expand market share during a period of weaker global demand, according to economists.

More By This Author:For Sale Inventory On The Rise Dash For Cash Intensifying What Interest Rates Say About Home Prices