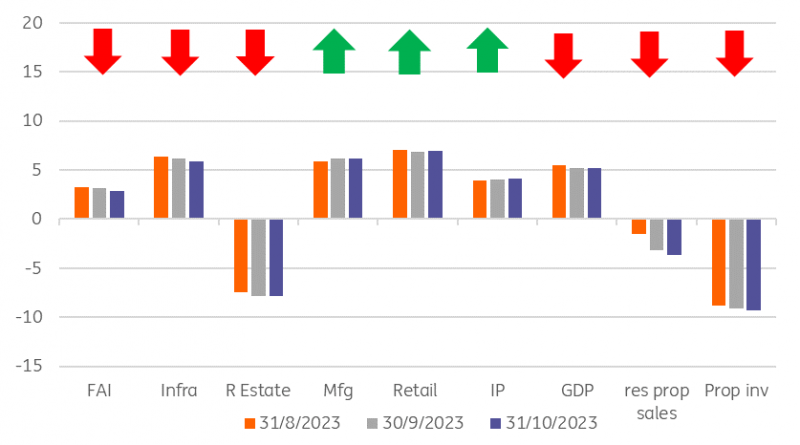

Despite leaving the one-year medium-term lending facility (1Y MLF) at 2.5%, the PBoC injected a net CNY600bn (over and above amounts falling due) to help support stimulus spending, raising thoughts that perhaps they may also tap other policy tools such as required reserves in due course. More funding will help activity to recoverAhead of the monthly deluge of activity data, the PBOC already provided markets with a positive surprise. Despite leaving the 1-year medium-term lending facility (1Y MLF) rate at 2.5%, the PBoC provided CNY1.45tr in funding, a net CNY600bn more than that which was falling due for rollover. The MLF is the conduit through which the PBoC lends funds to big commercial banks, who in turn, finance the rest of the economy. Short-term market interest rates have risen since September, as the CNY has weakened in the face of a stronger USD, and the PBOC has kept short-term funding costs high to deter CNY selling. However, this has also resulted in a bit of a liquidity squeeze, and it now looks as if the PBoC is looking to sidestep the unhelpful rate environment and alleviate liquidity issues by turning to volume lending instead.In so doing, it raises thoughts that similar liquidity-enhancing policies, such as the rate of required reserves (RRR), might also be tapped in the coming weeks and months, as the government looks to support economic activity, without resorting to large direct fiscal stimulus measures, or to rate cuts, which could send the CNY weaker. The last cut in the RRR was back in September when the rate for banks was cut by 0.25%. Activity data – mostly stronger except for anything property relatedThe run of activity data again suggested further modest progress in China’s recovery, though once again, there was a divergence between general activity, which moved forward, and anything property-related, which continued to flounder.The year-on-year growth rate for retail sales moved from 5.5% to 7.6% YoY, and well above the 7.0% rate expected. But year-to-date year-on-year measures, which may be less whipped around by last-year’s pandemic-related distortions, showed a smaller improvement from 6.8% to 6.9%.Industrial production also showed gains, rising to 4.6%YoY (from 4.5%) and 4.1% YoY ytd (from 4.0%).There was less good news for fixed asset investments, which slowed to 2.9% YoY ytd, from 3.1%. And property investment declined at a faster pace of 9.3% (from -9.1%) while residential property sales also fell slightly faster (-3.7% down from -3.2%).The surveyed unemployment rate remained 5.0%, though we don’t know what is happening to youth unemployment since the figures stopped being published. It most likely remains extremely high. Summary of China activity data (YoY% ytd)

More funding will help activity to recoverAhead of the monthly deluge of activity data, the PBOC already provided markets with a positive surprise. Despite leaving the 1-year medium-term lending facility (1Y MLF) rate at 2.5%, the PBoC provided CNY1.45tr in funding, a net CNY600bn more than that which was falling due for rollover. The MLF is the conduit through which the PBoC lends funds to big commercial banks, who in turn, finance the rest of the economy. Short-term market interest rates have risen since September, as the CNY has weakened in the face of a stronger USD, and the PBOC has kept short-term funding costs high to deter CNY selling. However, this has also resulted in a bit of a liquidity squeeze, and it now looks as if the PBoC is looking to sidestep the unhelpful rate environment and alleviate liquidity issues by turning to volume lending instead.In so doing, it raises thoughts that similar liquidity-enhancing policies, such as the rate of required reserves (RRR), might also be tapped in the coming weeks and months, as the government looks to support economic activity, without resorting to large direct fiscal stimulus measures, or to rate cuts, which could send the CNY weaker. The last cut in the RRR was back in September when the rate for banks was cut by 0.25%. Activity data – mostly stronger except for anything property relatedThe run of activity data again suggested further modest progress in China’s recovery, though once again, there was a divergence between general activity, which moved forward, and anything property-related, which continued to flounder.The year-on-year growth rate for retail sales moved from 5.5% to 7.6% YoY, and well above the 7.0% rate expected. But year-to-date year-on-year measures, which may be less whipped around by last-year’s pandemic-related distortions, showed a smaller improvement from 6.8% to 6.9%.Industrial production also showed gains, rising to 4.6%YoY (from 4.5%) and 4.1% YoY ytd (from 4.0%).There was less good news for fixed asset investments, which slowed to 2.9% YoY ytd, from 3.1%. And property investment declined at a faster pace of 9.3% (from -9.1%) while residential property sales also fell slightly faster (-3.7% down from -3.2%).The surveyed unemployment rate remained 5.0%, though we don’t know what is happening to youth unemployment since the figures stopped being published. It most likely remains extremely high. Summary of China activity data (YoY% ytd) CEIC, ING The economy is still strugglingTaking all of the data together, the general sense is that things are moving slowly in a more positive direction, but that the economy still needs the liquidity support that the PBoC seems to be starting to provide, and the slightly more helpful fiscal stance that the central government is taking. We don’t expect the external environment to improve meaningfully. The US may be weathering high interest rates for now, but we suspect that won’t last. And Europe is skirting recession, with little prospect of an upturn.Moreover, while the property sector continues to struggle, which we expect will be the case for some considerable time, the spillover effects to the rest of the economy are likely to keep overall growth rates tepid. The government’s 5.0% GDP growth target is not under threat any more. But it was always a very unambitious target.More By This Author:Asia Morning Bites For Wednesday, November 15The Fed Is Done And Market Rates Have Peaked – So What Now? Rates Spark: Shifting The Rate Cycle Discount

CEIC, ING The economy is still strugglingTaking all of the data together, the general sense is that things are moving slowly in a more positive direction, but that the economy still needs the liquidity support that the PBoC seems to be starting to provide, and the slightly more helpful fiscal stance that the central government is taking. We don’t expect the external environment to improve meaningfully. The US may be weathering high interest rates for now, but we suspect that won’t last. And Europe is skirting recession, with little prospect of an upturn.Moreover, while the property sector continues to struggle, which we expect will be the case for some considerable time, the spillover effects to the rest of the economy are likely to keep overall growth rates tepid. The government’s 5.0% GDP growth target is not under threat any more. But it was always a very unambitious target.More By This Author:Asia Morning Bites For Wednesday, November 15The Fed Is Done And Market Rates Have Peaked – So What Now? Rates Spark: Shifting The Rate Cycle Discount

China: People’s Bank Of China Injects More Cash To Support The Weak Economy