When we first said three weeks ago that the spectacular, sudden implosion of Canada’s largest alt-lender Home Capital Group or HCG – whose fate we had followed closely since 2015 – was Canada’s own “New Century Moment“, the parallels were more than just the obvious: like in the US, it took the market nearly a year to realize the full implications of the subprime collapse which first manifested in the failure of New Century and its subprime lender peers. When all was said and done, the world’s central banks had to pump (and still do) trillions into the financial system to stop it from disintegrating.

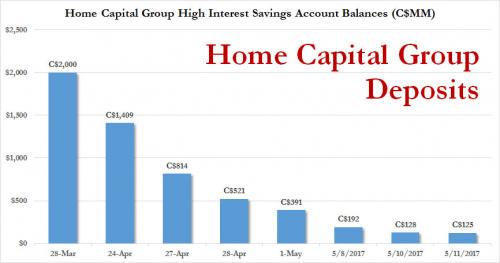

Slowly but surely, Canada is starting to appreciate just how serious the Home Capital failure is, and how the unprecedented bank run that has led to 94% of retail deposits fleeing the troubled lender.

It is just the first step of what will likely be a very painful process, which will likely culminate with either a government bailout, or a financial system on the verge of panic.

Today, the Globe and Mail has published an in-depth report putting the HCG pieces together, or as the G&M itself puts it, the “dramatic story of a financial institution’s near-collapse.”

How quickly can a financial institution go from seemingly healthy and solvent to being on the verge of liquidation? The answer: hours. Here is the background:

It was late in the evening on Sunday, April 30, when lawyers working for Home Capital Group Inc. dialled into a call with lawyers representing the company’s new lending syndicate. The troubled mortgage lender had negotiated a $2-billion credit line just days earlier, emergency money the board felt was needed to survive after a high-profile run on deposits at subsidiary Home Trust. The company planned to draw down the first $1-billion from it the next morning, May 1.

But the deal was getting bogged down in a last-minute dispute over details of the funding, according to two sources familiar with the talks. As the conversation proceeded late on Sunday, it became increasingly evident that the fate of the financing was hanging in the balance. Another call at 2 a.m. on Monday ended badly with no agreement, a source said.

There was no room for error. Home Capital was hours from the start of its business day, and it was critically low on capital. The board had determined the company could not open its doors for business Monday morning without the financing in place, the sources said.

As the dispute continued, officials from Canada’s banking regulator, the Office of the Superintendent of Financial Institutions (OSFI), were on standby to launch a process to take control of the company Monday, a move that would have almost certainly forced some form of wind-up of Home Capital’s business, the sources said.

In the end, some time prior to 7 a.m., the lawyers hammered out a deal on final terms of the loan, allowing the first $1-billion to be transferred Monday. When business started a couple of hours later, only a small circle of exhausted insiders knew how close the company had come to collapse.

The collapse started on April 19.

… much of the unrelenting focus on the company is also due to the rarity of a financial institution failing in this country. Canada Deposit Insurance Corp. (CDIC), which insures deposits in the event of a bank failure, hasn’t paid a claim since 1996.

Many commentators have pinpointed April 19 as a pivotal date when the Ontario Securities Commission unveiled an explosive enforcement case against the company and three of its executives, accusing them of making misleading disclosure to investors about mortgage underwriting problems in 2014 and 2015.But if the OSC announcement sparked a conflagration at Home Capital, it was only because there was so much dry tinder already in place to ignite. The case landed amid a broader backdrop of concern about the company’s financial condition, a loss of faith in senior management and the board, and extreme nervousness about the vulnerability of a non-prime mortgage lender deeply exposed to Toronto’s overheated housing market.

But the seeds of failure had been planted years ago, roughly around the time since 2015 HCG and accused it of issuing “liar loans.” It took regulators two years to catch up.

The first alert about the OSC case, for example, emerged late on a Friday afternoon on Feb. 10, when many had already left for the weekend. Home Capital Group issued a two-paragraph release revealing it had received an enforcement notice from the OSC, relating to disclosures in 2014 and 2015 about an internal investigation that found information on some loan applications had been falsified, leading to suspensions of 45 mortgage brokers. The enforcement notice said OSC staff had reached a preliminary conclusion about problems at the company, but Home Capital still had an opportunity to respond before the commission decided whether to launch disciplinary proceedings.