Image source:

Image source:

A fourth consecutive Bank of Canada rate cut is expected, but the market senses it will accelerate the move towards neutral policy rates with a 50bp step change. Inflation is finally below target and unemployment is trending higher, but the economy is still growing. We narrowly favour the BoC sticking with 25bp increments, but would not be shocked by 50bp.

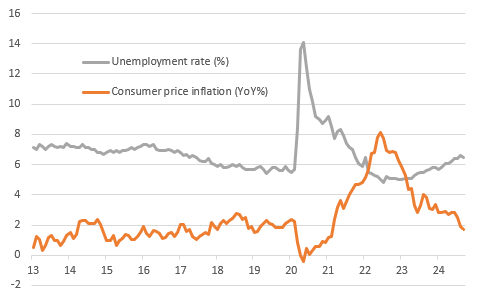

Close call between 25bp and 50bpThe Bank of Canada has lowered the target for the overnight rate at its past three policy meetings and is expected to follow up with a fourth consecutive cut next week. The question is, will it be another 25bp move or will the bank follow the Federal Reserve’s lead and cut by 50bp?Consumer price inflation slowed to just 1.6% year-on-year in September, undershooting the 2% target for the first time since February 2021. The bulk of the residual strength is due to housing costs, which if excluded would prompt inflation to fall below 1%. Nonetheless, we can’t pick and choose which things to exclude and include, and BoC officials remain wary about easing too far, too fast and running the risk of a return of price pressures.At the September policy meeting, the committee argued that “excess supply in the economy continues to put downward pressure on inflation, while price increases in shelter and some other services are holding inflation up. The Governing Council is carefully assessing these opposing forces on inflation”.Canada unemployment rate (%) versus consumer price inflation (YoY%) Source: Macrobond, ING

Source: Macrobond, ING

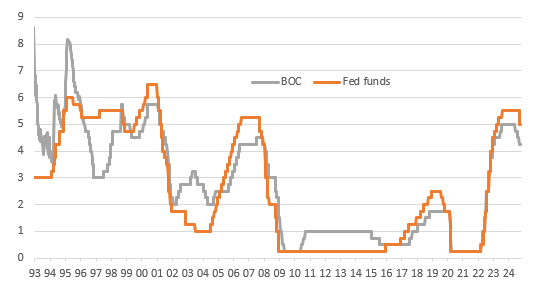

Inflation is cooling, the labour market is loosening, but the growth outlook is improvingIn terms of the job market situation, unemployment has climbed from a low of 4.8% in July 2022 to 6.5% today, but this is not because of job losses. Total employment is actually at all-time highs and stands more than a million higher than pre-pandemic levels. Instead, it is down to excess supply resulting from rapid population increase generated by a large wave of immigration in recent years. Nonetheless, this slack in the labour market should keep a lid on wage pressures and help contain inflation pressures over the medium term.General activity levels are subdued, but the economy is growing with recent monthly GDP and retail sales numbers beating expectations and the third-quarter Business Outlook survey pointing to a more optimistic outlook for the Canadian economy. As such, we continue to see a strong case for ongoing gradual rate cuts to bring monetary policy to a more neutral setting. Whether the committee sees enough to justify an acceleration in the process with a 50bp move is a close call.US versus Canada policy rates (%) Source: Macrobond, ING

Source: Macrobond, ING

Widening US-Canada rate differentials could argue for cautionThe consensus is on a knife edge as to whether it will be a 25bp or a 50bp cut. Financial markets are more confident, pricing 45bp of a 50bp move with a cumulative 83bp of cuts priced over the November and December meetings versus a mere 60bp just over a week ago.A 50bp cut from the BoC would widen out the spread with the Fed funds target rate to 125bp once again and this may put additional downside pressures on the Canadian dollar. This would threaten to push up import costs and may also add to nervousness from some officials about pursuing such a move. Consequently, we very narrowly favour the BoC choosing to go with 25bp, but would not be shocked by a 50bp cut.

CAD: Lots of dovishness in the priceThe gap between the USD and CAD two-year swap rate has widened substantially of late, from 50bp to 80bp since the start of October. This is mirroring both aggressive dovish rate expectations in Canada and a hawkish repricing in the US. Such a widening gap has been the main driver for the USD/CAD rally to the 1.38 mark and has prevented the loonie from benefitting from its lower risk profile in the crosses, ahead of some pre-US election positioning.The balance of risks is clearly skewed to the upside for CAD next week. Markets are fully pricing in a 50bp move that is far from guaranteed, and a 25bp cut can trigger a sizeable correction higher in the loonie. Even in the event of a half-point cut, markets are pricing in more than 25bp in December, meaning the room for a further dovish repricing in the CAD OIS curve is low. Our view remains that CAD has room to appreciate, if not against USD that might get support into the US election, at least versus other commodity currencies (e.g. AUD, NZD) that are more exposed to Trump hedges.More By This Author:FX Daily: Trump’s Specter Hangs Over The FX Market Asia Morning Bites For Thursday, Oct 17Plunging UK Services Inflation Set To Accelerate Rate Cuts

Canada Debates Whether To Supersize Rate Cuts