When Seritage Growth Properties (SRG) was spun out of Sears Holdings in 2015, it had two forces working against it – a large portion of their leases were with Sears and KMart and alarms have sounded about the future of the shopping mall and brick and mortar retail as e-commerce sales take an increasingly bigger portion of the retail pie. Seritage may overcome these obstacles, but if it does so it will need to flawlessly execute a transformation of its real estate portfolio to modern uses and amongst a diversified client base.

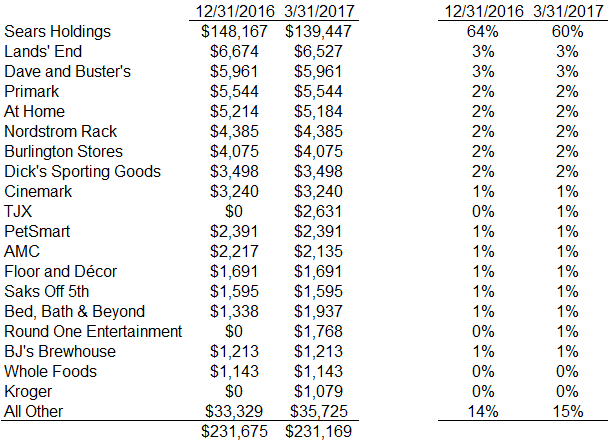

Seritage has already made good progress in finding new tenants. At the time of separation from Sears, 86% of its rent came from its former company. Today the figure is down to 60%.

Seritage’s diversification matters not just for reducing a single-tenant risk, but because once Sears closes a store and Seritage develops the property, it can charge meaningfully higher rents. Last year, Sears paid Seritage rent of $4.40 for every square foot that it leased. Seritage’s other tenants paid an average of $13.18.

Presently, investors are giving Seritage a valuation that is close to its peers when traditional metrics like funds from operations are considered but is woefully undervalued against its assets. It is obvious that the disconnect stems from Seritage being able to charge a lower rent for the real estate it owns than its peers do.

At 23x funds from operations, Seritage is right in line with Simon Property Group (SPG) and General Growth Properties (GGP) and at a discount to the highly regarded Realty Income. But, on the basis of its real estate, it’s valuation is quite low. Were it to trade in the future at the lower end of its peers of $250 square foot, the share price would be about $264 – six times what it trades for today.