Data/Event Risks

Data/Event Risks

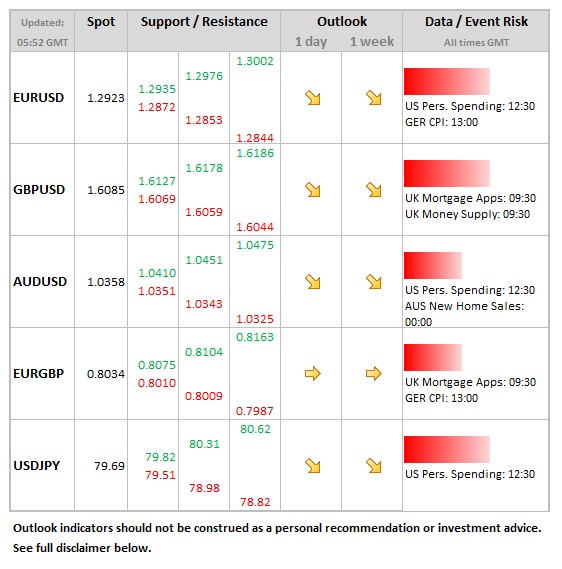

- USD: Personal spending and income the only economic release of note today. The former has been robust in recent months, but be alert because it could slow near term. Later this week, ISM and non-farm payrolls are the big releases.

- EUR: Just German inflation and Spanish retail sales out today. The latter could add to the recent sombre tone in the euro if it comes out on the weak side. PMIs due out later this week.

- JPY: Jobless rate and industrial production out late tonight. Any softness will add to pressure on the BOJ to ease further when they meet later this week.

Idea of the Day

The dollar was unaffected by GDP showing economy grew 2.0% in Q3. Dollar index desperately attempting to climb above the 50d MA at 80.15. Month-end flows might propel USD to higher levels near term.

Latest FX News

- EUR: Would not be surprising to see a serious test of the 50d MA and 200d MA at 1.2841 and 1.2836 (respectively) in the next couple of days. That said, the 1.28-1.32 range has held very tight since the Fed’s QE3 announcement in mid-September.

- GBP: Notwithstanding last week’s robust performance, cable’s 6 week downtrend was not penetrated, and so the downside is still favoured. Month-end flows may well weigh on sterling.

- AUD: Right now, the Aussie is the Teflon currency. The 1.02-1.06 range which has been in play for the past two months remains. Even so, short term it may pay to fade any strength.

- JPY: A huge reversal in the yen’s fortunes on Friday, as shorts scrambled for cover. In USD/JPY, 80.30 was always going to be tough to break first time around. BOJ likely to announce more asset purchases later this week.