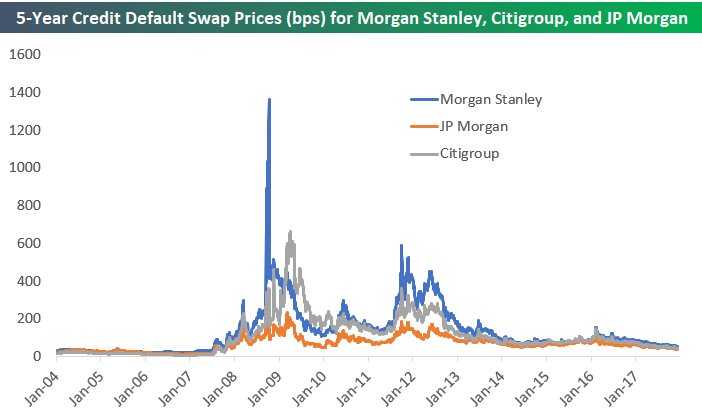

Below is a historical chart showing the annual cost of insuring against default for 5 years (5-year CDS) for three major US banks and brokers — Morgan Stanley, JP Morgan, and Citigroup. The price is in basis points, and basically the price shown is the cost in dollars per year to insure $10,000 of debt against default for five years. Large bondholders use credit default swaps (CDS) to hedge risk, but CDS also attract speculators as well. During the Financial Crisis, hedge funds betting against the banks made billions buying and selling CDS as prices to insure against default spiked.

We’re highlighting this chart today because of how low CDS prices have gotten again in the Financial sector. At this point, CDS prices for most of the major US financials are at the same levels they were trading at in July 2007. Back then, CDS prices had begun to rise a bit for the sector as some of the sub-prime mortgage companies were starting to go under, but prices didn’t really start to spike until late 2007.

Â

You can see the moves a little better in the chart if we cap the price on the Y-axis at 300 basis points.

Even though the Financial sector appears to be on better footing now than it was prior to the Financial Crisis, the cost to insure against default remains more elevated than it was in the early to mid-2000s. In hindsight, the levels that CDS prices traded at prior to the crisis were way too low, and the negative result of those low prices that “the market†experienced during the collapse appears to have lifted the price level that is now considered “normal.â€

Â