It was just one short month ago when, on the back of the soaring dollar (which has since soared even more), as well as “diminished global GDP growth and lower crude prices“, Goldman’s David Kostin cut his EPS for 2015 and 2016 from $125 and $132 to $122 and $131.

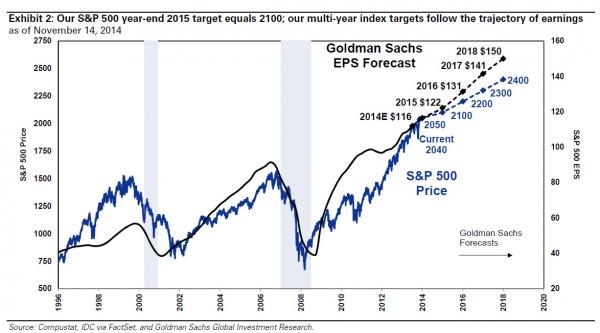

Then, it was just two short weeks ago, the same David Kostin said “we expect the P/E will contract and the index will slip during the second-half of 2015 as the Fed takes its first step in the long-awaited tightening cycle. Our S&P 500 year-end 2015 target of 2100 implies a modest 5-10% P/E multiple compression to 16.0x our top-down 2016 EPS estimate or 14.6x bottom-up consensus earnings estimates.”

Â

Â

Â

And then, with the S&P now about 20 points away from Goldman’s 2015 year end target (and just 120 points from the government-backed hedge fund’s 2016 year end target!), the very same David Kostin admits that he was only kidding and that the S&P may in fact rise to a whopping 2300, using the oldest excuse in the book to admit that strategists always and forever trail price – rigged as it may be – using the Fed Model as justification for what is now effectively a 19x P/E Multiple, using Goldman’s 2015 EPS target of $122 and its hint-hint revised S&P target of 2300.

To wit:

A lower interest rate scenario vs. our forecast would support a higher 2015 S&P 500 target

Â

The drop in 10-year Treasury yields from 3% to 2.3% has been one of the biggest market surprises of 2014. We expect rates to rise next year in conjunction with an initial Fed hike and accelerating GDP growth. The persistence of low rates has led many investors to question our economists’ year-end 2015 forecast of fed funds at 0.6% and 10-year Treasuries at 3%. As the yield curve normalizes, if interest rates remain lower than we anticipate, equity returns could be greater than we forecast. Within the confines of a Fed model, an end-2015 S&P 500 level of 2300 would be consistent with 2.5% 10-year Treasuries while our forecast of 2100 assumes a 3% yield.