21%.

That’s the expected earnings gains for S&P 500 companies this quarter compared to the same quarter last year. Most of that is due to the tax cuts and the rest is due to buybacks as there are now no longer $2 TRILLION worth of shares to divide the earnings among due to buybacks and M&A (which earases the shares completely while putting the earnings into another company). Â

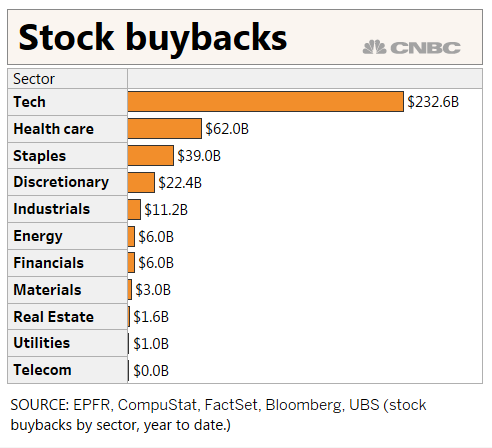

As you can see from the chart on the right (only through June), buybacks have been heavily oriented to the tech sector, as has M&A activity so it’s no surprise the Nasdaq is plowing higher despite the actual companies not actually making more revenues or even more profits – it’s just the same profits divided by a lot less shares. Â

Still, it’s real. As an investor, if I buy a stock that makes $1Bn on 1Bn shares then I’m making $1 per share and I’ll pay $20 ($20Bn) at 20x earnings but, if the company takes $4Bn and buys back 200M shares (20%) then the same $1Bn in profits becomes $1.25/share and 20x becomes $25/share – on the same revenues and the same profits. So, for a CEO who gets paid based on stock performance, it makes sense to do share buybacks whenever possible and the $2.5Tn of offshore funds that have been “repatriated” from overseas (from where they were hidden to avoid paying taxes and are now being rewarded for their behavior) have gone almost entirely to this practice. Â

As I was saying, as an investor, you are getting your $25 worth from an earnings perspective as it’s still 20x earnings but, consider that last year, this company had $4Bn in cash on the $20Bn valuation (or cash and no debt) and now it does not. Wasn’t the OPPORTUNITY to use that $4Bn to grow the business part of what made the company worth 20x earnings in the first place? Now that opportunity is lost and the company is what it is at $25/share with MUCH LESS possibility of growth down the road as it WASTED 25% of it’s market cap buying back it’s own stock!