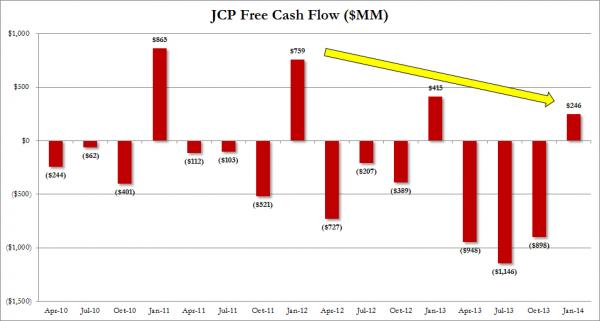

Moments ago JCP did what it does best: released results that missed expectations, with Revenues in the traditionally strongest, holiday (Q4) quarter of $3.78 billion below the $3.86 billion expected, and comp sales up 2.0% below the 2.1% expected. Additionally, the company’s profit margin was 28.4%, the second lowest in recent history, and only better than the 23.8% posted a year ago when the company was openly imploding. But the red flag was Free Cash Flow, driven entirely by inventory liquidation, was $246 million: the lowest such amount for the holiday quarter also in history. Whether or not this miss was not quite as bad as a worst case miss could be, whatever that means, is unclear but for now the traditional post-earning squeeze has pushed the stock higher. How long this particular squeeze persists is unclear, but likely depends on the longer-term viability of the company, and recent trends. To determine what these are, here are some charts showing how the company has performed in recent years.

First, here is JCP’s all important Free Cash Flow. While in Q4 JCP generated a little over $200 million in cash, it is the next three quarters that matter, as this is when the company burned the bulk of its cash. As a reference point: last year, in the Q1-Q3 period, JCP burned $3 billion.

JCP better not intend on burning $3 billion this year too. Why? Because as it reported, it expects its liquidity “to be in excess of $2 billion at year-end.” Really? How? Because that inventory build and $2-3 billion cash need will hardly grow on trees.

Next, we look at revenue: while this missed as we noted above, it was the only bright spot in the earnings report – the good news: it wasn’t an all out crash, even if like FCF, it was the lowest revenue for the holiday quarter in recent history.

Next, and perhaps most troubling, was the reason for the company’s subar free cash flow creation: in a nutshell, the company did not sell nearly enough inventory in the quarter. As the following chart shows, JCP liquidated, and thus generated “only” $812 million in inventory cash in the quarter: in prior years this number was always greater than $1 billion. This likely means even greater mark downs in coming quarters as JCP scrambles to dump even staler products.