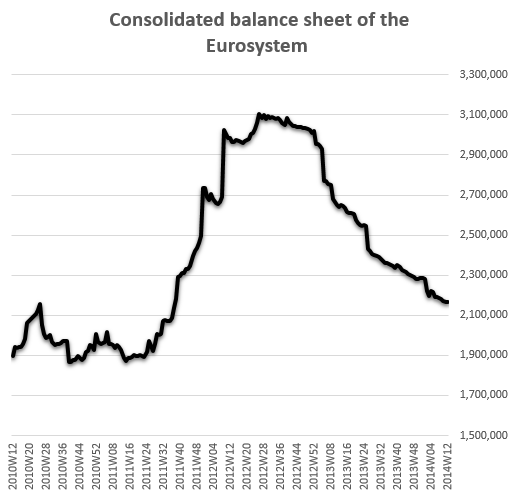

The Eurozone’s unemployment rate is at 12% and holding while the area’s youth unemployment is at staggering 24%. Private lending is still contracting (see post) and disinflationary pressures persist even within the “core” states (see chart). The price stability situation in the “periphery” is starting to look outright deflationary -Â see chart. Â The euro is still at mulit-year highs, putting pressure on the area’s export businesses. At the same time monetary conditions continue to tighten as the area’s central banking system balance sheet approaches pre-LTRO levels.

unit = mm € (source: ECB)

Given the situation, most central bankers would take action. A simple policy change for example could be to suspend the sterilization of securities already held by Eurosystem -Â see post. But the ECB is hesitating. Why? Here are some reasons:

1. This may upset some folks but the reality is that the ECB is notoriously indecisive as it is pulled into various directions by the member states. Many forget that the institution is relatively new (just over 15 years in existence) and the shock of the recent crisis had left the organization a bit paralyzed. It rarely takes a decisive action unless it’s forced by the markets to do so. The decision to “save the euro” only arose as Spain approached the point of “no return”.

2. The ECB is also somewhat distracted as it prepares to take on the massive task of regulating the area’s banking system – a responsibility that was not initially part of the central bank’s charter.

3. The ECB does not have the dual mandate of the Fed and is only focused on price stability. The central bank views the area’s horrible unemployment problem as being outside of its “jurisdiction”. While technically correct, many central bankers would regard this narrow interpretation of the rules as shortsighted.

4. The hawks at the ECB continue to view the disinflationary pressures in the euro area as transient.